Cash Gab with Noah - March 2026

Noah Ross - Mar 01, 2026

Quick Nugget of the Day

Inflation, The Silent Tax

Inflation quietly erodes your purchasing power over time. Even when it feels “low,” it compounds year after year, meaning a dollar today won’t buy the same goods and services in the future.

It doesn’t show up as a single painful moment. It shows up gradually, and that’s what makes it easy to underestimate.

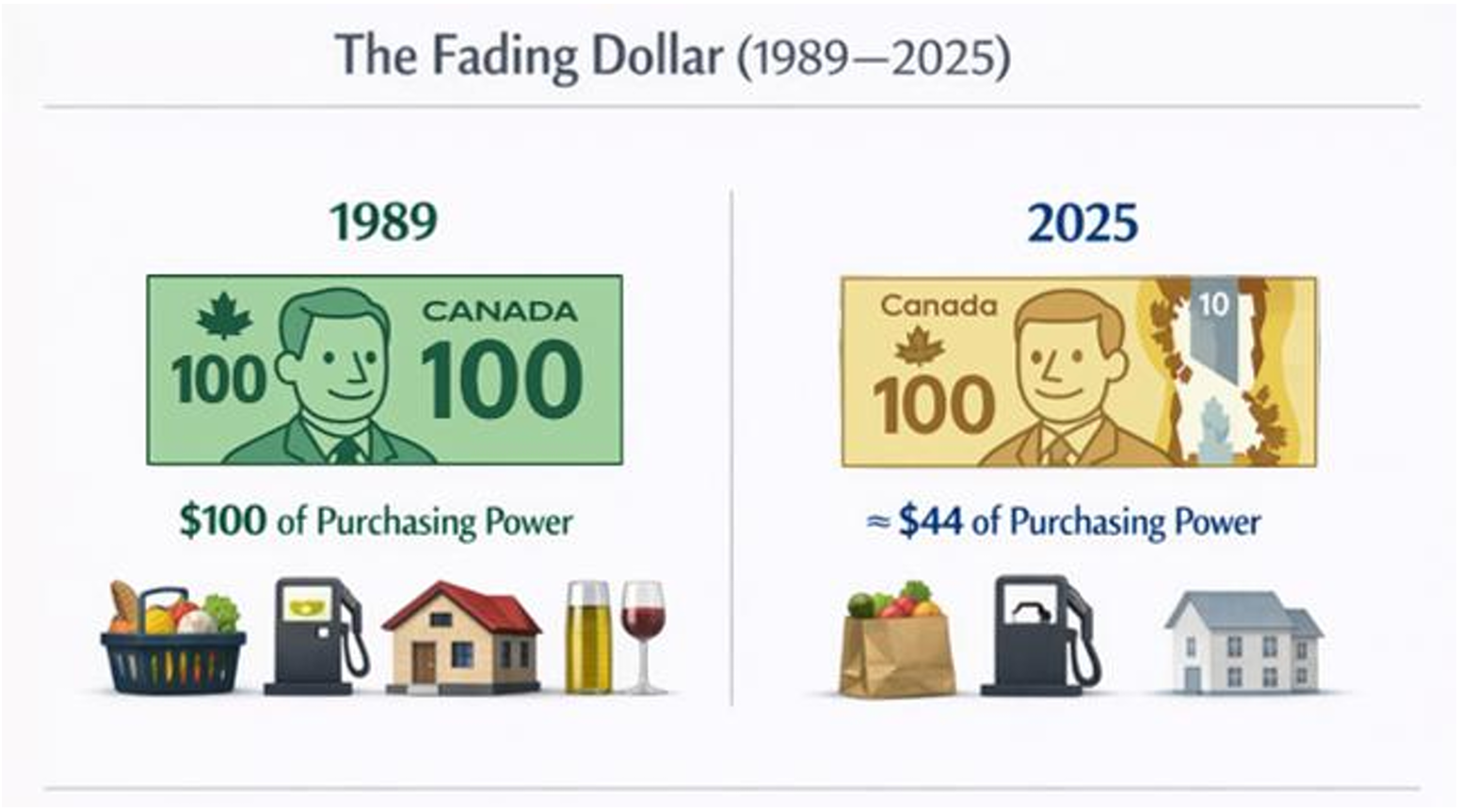

What Inflation Does to Your Dollar (1989 --> 2025)

Using Consumer Price Index (CPI) figures:

- 1989 CPI: 72.7

- 2025 CPI: 164.2

- Time Period: 36 years

This works out to an average annual inflation rate of approximately 2.3%.

So, what does that mean in real terms?

Something that cost $100 in 1989 would cost about $226 today.

Put differently:

$100 in 1989 = $44 of purchasing power today.

What’s powerful about this is it happened within a single working lifetime.

What this Means for Your Investments

Let's look at two simple examples:

Scenario A: Your money earsn 2% per year

(Think high-interest savings accounts or GICs)

- Inflation: 2.3%

- Real return: -0.3%

Your account increases, but your purchasing power slowly declines.

It’s common for people to keep a large portion of their wealth in low-interest options because they feel “safe”. For money you’ll need in the short-term, that can be a prudent choice. But for long-term money, safety isn’t just about avoiding volatility, it’s about preserving and growing purchasing power. That’s where equities play an important role.

Scenario B: Your money earns 7% per year

- Inflation: 2.3%

- Real return: 4.7%

In this case, your purchasing power meaningfully increases over time. Your returns outpace inflation by a healthy margin, which means the goal of long-term growth of your money is actually being achieved.

Takeaway

Inflation is the silent tax on cash and low-return investment strategies. For long-term goals, it must be part of the equation.

At an inflation rate of 2.3%, the value of your dollar is effectively cut in half every 31.3 years. As retirements become longer, this highlights the importance of balance, combining guaranteed, volatility-free investments with long-term equity exposure designed to grow purchasing power over time.

The goal isn’t to chase returns. It’s to make sure your money keeps up with the life you want it to support.

Critical Illness (CI) and Disability Insurance (DI)

A disability or a critical illness such as cancer, heart attack, or stroke can impact far more than someone’s health. It can disrupt daily life, jeopardize long-term financial plans, and force families to make difficult choices. Without proper 3 OF 7 protection, treatment costs, caregiving needs, or the loss of income can quickly erode savings that were earmarked for other goals.

Two types of insurance can help protect your earning ability and your financial stability: disability insurance and critical illness insurance. While both provide financial support during illness or injury, they do so in different ways, and for different situations.

Disability Insurance: Income Protection

Disability insurance replaces a portion of your income if you can’t work due to injury, serious illness, or mental health challenges. For many employees, this coverage comes through workplace group plans; for others, a private plan may be required. Benefits are paid monthly, typically until you return to work, reach age 65, or pass away.

However, disability insurance has limitations, especially for people whose income structure doesn’t align with traditional employment.

Business owners and incorporated professionals are a prime example. Many minimize T4 income and draw corporate dividends to maximize tax efficiency. But disability insurers base benefits on earned income, not dividends which reduces coverage available. As a result, many business owners are under‑insured relative to their lifestyle.

Self-employed individuals face similar challenges: fluctuating income, fewer group benefits, and a strong incentive to “push through” an illness because stepping away could jeopardize their client base or business operations.

High-income professionals often face benefit caps. For example, a maximum monthly benefit may only replace a small percentage of their $250,000 or $500,000 annual income. This creates a gap where private DI is required to close it.

Critical Illness Insurance: Flexible, Lump-Sum Support

Critical illness insurance pays a tax-free lump sum upon diagnosis of a major illness (after a short survival period). This payment is not tied to income, making it especially valuable for:

- Business owners, who may need funds to keep their business running while they recover.

- High income individuals whose lifestyles and financial obligations far exceed DI benefit caps.

- Stay-at-home parents or people out of the workforc ewho cannot qualify for disability insurance at all.

- Partners or spouses who may need to reduce work hours to take on caregiving responsibilities.

Critical illness insurance is flexible, and the benefit can be used for anything: medical treatment, paying down debt, replacing a spouse’s lost income, hiring caregiving help, or covering business expenses during recovery.

Some policies even provide return-of-premium options if no claim is ever made.

Why They Work Best Together

If someone must choose only one type of coverage, disability insurance often comes first because it replaces ongoing income. But for many families, especially those with complex income structures, critical illness insurance serves as a powerful complement or, in some cases, the only viable option.

The Bottom Line

Disability insurance protects the income you earn. Critical illness insurance protects the financial stability you need while you heal.

Together, they create a more complete safety net that helps safeguard your family, your business, and your long-term goals from the financial shock of a serious illness or injury.

In the News

Missed Mortgage Payments in Toronto have Quadrupled – Toronto Life

For years, rising interest rates were framed as a future risk. This data shows that stress is now showing up in real household cash flows, particularly for more recent buyers who stretched at peak prices and are now renewing at higher payments.

The Canadian Mortgage and Hosing Corporation (CMHC) emphasizes that income stability, not home prices, is the key determinant of mortgage health. Households with emergency savings, flexible spending, or longer planning horizons are far better positioned than those relying on rate cuts or price rebounds.

Fidelity 2025 Retirement Report – Fidelity

Fidelity Canada’s 2025 Retirement Report reveals how dramatically retirement expectations have shifted over the last twenty years. Today, Canadians approaching retirement believe they need over $1M to retire comfortably which is more than double what they believed in 2005 after adjusting for inflation.

Retirement is also becoming more complex. Nearly 9 in 10 Canadians say planning is harder than it was 20 years ago, driven by rising living costs, wanting to pass wealth to younger generations while still alive, and economic uncertainty. As a result, Canadians are retiring later with the average retirement age climbing from 61 to 65. Encouragingly, retirement isn’t viewed as “stopping work” but rather transitioning to flexible work or passion projects.

One finding stands out, planning matters. 90% of Canadians with a written financial plan feel prepared for retirement, compared to just 55% without one. Those who work with an advisor are more optimistic about their financial future.

Bottom line: Retirement may be more expensive and increasingly uncertain, but Canadians who plan, adapt, and get good advice feel significantly more confident about what’s ahead.

Cash Gab Book of the Month

Book: The Art of Spending Money

Author: Morgan Housel

Summary: This book reframes money not as a math problem, but as a deeply personal and psychological one. Housel argues that while many people learn how to make money, very few learn how to spend it well. True wealth comes from aligning spending with values, independence, and long-term satisfaction, rather than status, comparison, or fear.

- Spending is an art, not a science. Most people aren’t very good at knowing what they actually want from their money, so they default to using it as a benchmark for comparison (house, car, clothes, lifestyle).

- What makes one person happy can make another miserable. The goal is to identify what you genuinely enjoy spending money on and do more of that.

- Money doesn’t buy happiness, but it can buy independence, and independence meaningfully increases the odds of living a happier, more intentional life.

This was a great book and caused me to reflect on my own spending, what I enjoy spending money on, and just as importantly, what I don’t. One idea that really stuck with me was the danger of tying your identity too tightly to being a “good saver.” Housel points out that if your identity is built around not spending, then spending later (when it’s time to actually use your savings) can feel psychologically painful and disorienting.

I’d recommend this book to anyone who wants a healthier, more intentional relationship with money, especially those who are good at saving but unsure whether they’re actually using money to support the life they want.

The Ross Group: Who We Are

At Ross Group Wealth Advisors, we work with future-minded investors to keep them on track toward greater wealth. Through our unique approach to portfolio management and wealth planning, we deliver smart risk and tax strategies and guide sound decisions that secure their wealth and expand their lives.

What We Provide

We act as your financial quarterback, building comprehensive, long-term strategies, not quick fixes. Our wealth plans aim to minimize taxes and safeguard your financial health today and for the future.

We proactively review your portfolio and overall financial picture, update your wealth plan regularly, and ensure you stay aligned with your goals. We engage with your priorities, uncover opportunities, and challenge assumptions about what you can do and when.

Community Engagement

Subscribe!

Subscribe to the Cash Gab with Noah Newsletter to receive every issue by email as soon as it's released

In-person Cash Gab Session

What is a Cash Gab Session?

Cash Gab brings together peers in similar careers and life stages to share, listen, and learn about financial topics that matter to you. The goal is to build a community of like-minded, future-oriented people aiming to achieve financial freedom.