June Market Newsletter: Navigating Regime Change: Trade, Tariffs, and What Comes Next

Christopher Bowlby - Jun 23, 2025

The first half of 2025 has been characterized by a dramatic regime shift in economic policy following President Trump’s inauguration for his second term.

The first half of 2025 has been characterized by a dramatic regime shift in economic policy following President Trump’s inauguration for his second term. Running under the banner of MAGA 2.0, he pledged a more isolationist posture and explicitly protectionist trade agenda to accelerate the reshoring of manufacturing to the United States.

It did not take long for the post-election euphoria—fuelled by promises of pro-growth tax cuts and deregulation—to give way to the reality of policy inconsistency and abrupt reversals. President Trump inherited an enviable macro backdrop: robust economic fundamentals, historically low unemployment, solid productivity gains, and corporate earnings and equity indices near record highs. Yet market confidence quickly evaporated in the face of aggressive, at times incoherent tariff actions levied indiscriminately against allies and rivals alike. Rapid-fire policy announcements—often issued directly via social media—reminded investors that policy unpredictability remains a core feature of the new administration’s approach.

This culminated in the rollout of the “Liberation Day” tariffs, which upended the decades-old trade regime and triggered levels of market volatility not seen since the early days of COVID-19 or the depths of the Global Financial Crisis. Yet, in classic fashion, each escalation has been followed by a partial retreat: President Trump has repeatedly stepped back from the brink to adopt a more moderate tone once financial markets recoil. The outcome, for now, appears to be a codified 10% baseline tariff across nearly all imports—a structural shift with long-term implications for supply chains, price dynamics, and corporate capital spending.

In Canada, the surprise re-election of the Liberal government under Prime Minister Mark Carney—something that seemed improbable at the start of the year—has added a layer of domestic policy continuity, even as global trade frictions deepen. Carney’s reputation as a credible financial steward, forged during his leadership at the Bank of Canada through the GFC and the Bank of England during Brexit, has given markets cautious confidence that Canada can remain a stable counterweight to policy noise south of the border.

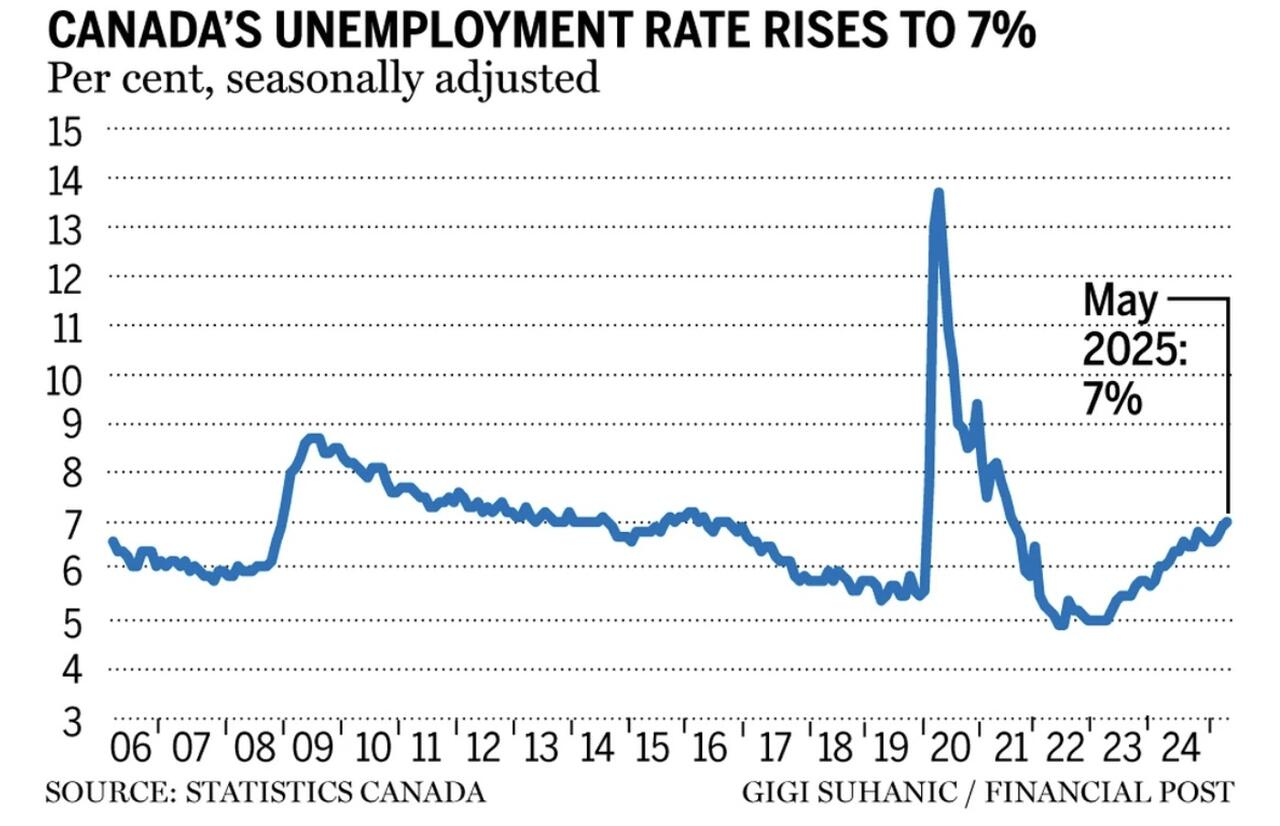

First-quarter GDP growth in Canada surprised to the upside at 2.2% annualized, buoyed by front-loaded exports and inventory stockpiling ahead of tariff deadlines. However, beneath the headline, signs of strain are emerging: consumer spending has softened, residential construction has lagged, and trade-sensitive industries are recalibrating. With the Bank of Canada holding its policy rate steady at 2.75% in June and unemployment drifting up to 7%, economic momentum is expected to moderate as businesses and households adjust to the new cost landscape.

Looking ahead, while tariff headlines and political soundbites may continue to swing sentiment in the short term, our focus remains anchored on owning high-quality businesses with pricing power, resilient balance sheets, and the discipline to navigate an environment where uncertainty is not an aberration but the new norm.

U.S. Trade, Fiscal and Political Landscape: OBBB, Baseline Tariffs, and the New Playbook for American Protectionism

Source: Bloomberg

With the MAGA 2.0 agenda now firmly in place, the United States has embarked on a deliberate reconfiguration of its global economic footprint. Nowhere is this clearer than in the overlapping layers of fiscal expansion, broad-based tariffs, and aggressive rhetorical signaling that define President Trump’s second-term approach.

Along with more aggressive tariffs and protectionist measures, President Trump has promised fiscal reform with the One Big Beautiful Bill (OBBB)—an ambitious budget package passed by the House and inching through the Senate with a high probability of approval in modified form. At first glance, the OBBB extends the 2017 Tax Cuts and Jobs Act, providing households and corporations with near-term relief: bigger standard deductions, renewed child tax credits, and cuts to taxes on tips, overtime, and specific middle-income wage brackets. This front-loaded tax relief has temporarily supported consumption and helped offset some consumer anxiety around tariffs.

However, the fiscal boost is front-loaded but shallow: the real budget math shows spending cuts, particularly to Medicaid and other social supports, ramping up only after 2027. If current Senate amendments moderate those cuts, the cumulative deficit impact could swell well past the headline $2.8 trillion estimate, raising red flags in the bond market. For now, this balancing act has left the U.S. running a deficit of roughly 7% of GDP—unusually large outside a recession—and paying higher yields as a result.

Tariffs and Trade Strategy: Structural, Not Temporary

What started with the “Liberation Day” shock has solidified into a 10% universal baseline tariff on nearly all imports—an explicit statement that the post-WTO low-tariff era is over for the world’s largest economy. While initially rattling markets, repeated climbdowns after brinkmanship (most visibly with China) have left investors expecting a pattern: big threats, partial backtracks, but a permanently more expensive trade channel.

The Geneva consensus framework, struck in recent talks between U.S. and Chinese negotiators, and President Trump’s latest conversation with President Xi, suggest tactical adjustments may still occur. For instance, both sides hinted at easing restrictions on rare earths and selected industrial inputs, helping to prevent complete supply chain freezes in sensitive sectors like semiconductors and battery technology. However, the structural signal is unchanged: the U.S. intends to maintain pricing leverage over inbound goods to encourage domestic production and rebalance trade relationships on its own terms.

Simultaneously, the Commerce Department under Secretary Lutnick continues to call for stricter export controls, particularly targeting dual-use technologies and AI-related hardware—reinforcing that the trade war is not purely about tariffs, but also about securing technological primacy.

Notably at the G7 in Kananaskis in Alberta, President Trump’s suggested that a new bilateral trade agreement with Canada could be finalized within 'days or weeks,' opening the door for targeted sectoral relief even as the 10% universal tariff baseline remains the structural floor for U.S. trade policy going forward."

Source: Getty Images

Canada: A Tale of Two Economies

If the U.S. narrative is one of self-imposed friction and policy pivot, Canada’s story is one of unavoidable exposure and cautious adaptation. Few economies are more entangled with American trade than Canada’s, and this year has reinforced how that structural reality shapes everything from regional growth rates to fiscal choices in Ottawa.

Headline data still paints a misleadingly solid picture. Canada’s economy expanded at a 2.2% annualized pace in Q1—its fifth straight quarter of above-trend growth. But beneath that number lies the same front-running behavior visible in U.S. trade figures: exporters and manufacturers rushing shipments south of the border to beat tariff deadlines, and retailers stockpiling key inputs to avoid cost spikes. That momentum is already unwinding. April’s trade report showed the goods deficit tripling to a record high, while exports fell nearly 11% month-over-month, including a 15% plunge in shipments to the U.S.

The labour market is showing cracks. Unemployment edged up to 7.0% in May, its highest non-pandemic reading since 2016. Manufacturing payrolls have fallen for four consecutive months, with auto and steel-related layoffs leading the decline. Meanwhile, consumer spending growth has softened, and the housing market remains stuck in a shallow downturn despite lower mortgage rates. Preliminary May data suggests a fragile bottoming in home sales, but affordability challenges and cautious buyer sentiment remain major headwinds—especially in Ontario and British Columbia.

Regional divergence is widening. Ontario and Quebec, heavily reliant on auto parts, steel, and aluminum production, face outsized risks from the doubling of U.S. tariffs. The non-U.S. portion of finished vehicles still attracts a 25% duty, weighing on both assembly lines and feeder industries. By contrast, Alberta continues to outperform: oil exports, which remain duty-free under the USMCA, have surged, and interprovincial migration has provided a demographic boost to local demand.

Policy response: fiscal backstop, not a silver bullet. Prime Minister Mark Carney’s minority Liberal government has moved quickly to deploy a mix of infrastructure spending, housing initiatives, and targeted support for industries squeezed by tariffs. The new fiscal framework implies a widening federal deficit—estimated to exceed 2% of GDP this year and to remain elevated into FY28/29—yet markets have largely endorsed the approach, trusting Carney’s credibility as a seasoned crisis manager. Moreover, backchannel diplomacy with Washington continues, with Carney and President Trump meeting personally during the G7 to try and lay the groundwork for further negotiations aimed at tempering the worst tariff excesses. At the G7 President Trump hinting that a focused Canada–U.S. trade deal could be reached within days or weeks — a potential catalyst to unwind some of the most punitive tariffs on key Canadian exports like steel, aluminum, and autos

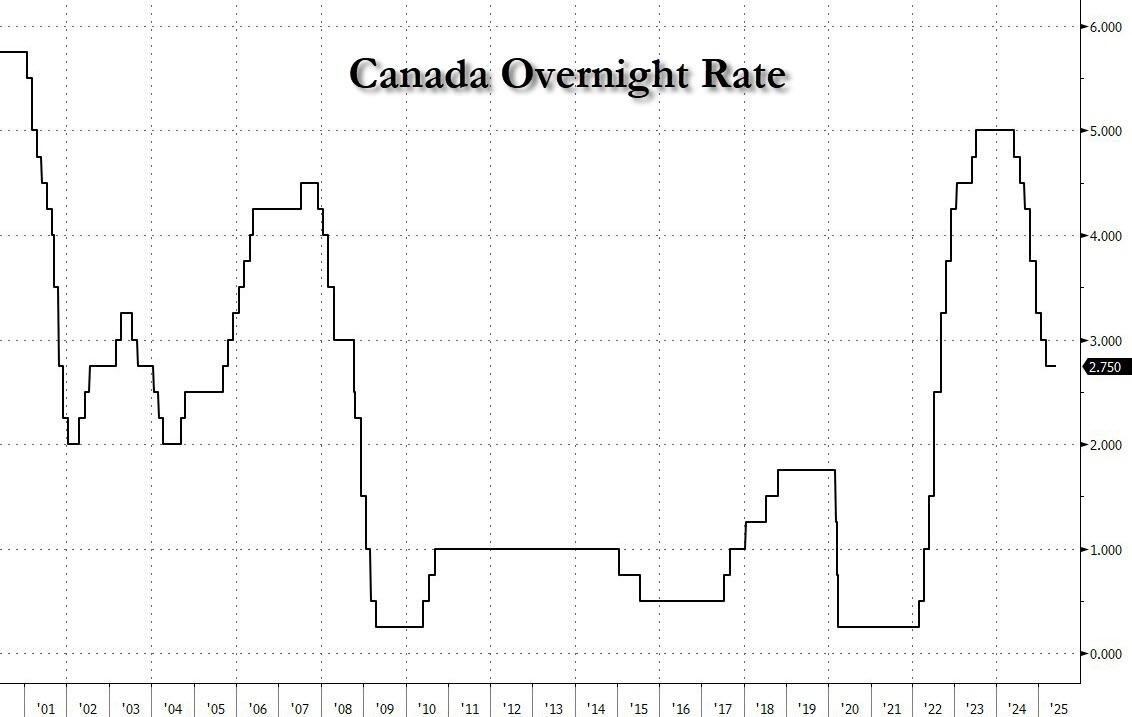

Monetary policy remains delicately poised. The Bank of Canada’s hold at 2.75% in June marked the second consecutive pause after a rapid series of rate cuts from last year’s 5% peak. Governor Macklem’s statement made clear the Governing Council is divided: some members worry that sticky core inflation (running near 3%) still warrants caution, while others see mounting evidence that trade-driven uncertainty and rising unemployment justify renewed easing. BMO Economics and other forecasters expect that a clearer trend in core CPI and a few more soft labour prints could tip the balance toward another cut by July or September.

US Inflation: Contained for Now, But the Tariff Shadow and Fiscal Fuel Linger

One of the more surprising storylines halfway through 2025 is how little the aggressive tariff regime has translated into headline inflation so far. Beneath the noisy policy environment, both the U.S. and Canadian consumer price trends remain more subdued than many feared—though the path ahead is anything but certain.

In the United States, the May CPI report delivered another pleasant surprise for markets. Headline inflation rose just 0.1% month-over-month, softer than the expected 0.2%, while core inflation—excluding food and energy—came in at an equally mild 0.1%, defying calls for a tariff-induced spike. On a year-over-year basis, headline CPI ticked up slightly to 2.4% (from 2.3% in April) and core CPI held steady at 2.8%.

One emerging wild card is the OBBB’s front-loaded tax cuts. While tariffs push on the supply side, renewed tax relief temporarily props up disposable income for middle-income households—sustaining consumption at a time when the Federal Reserve would prefer more visible demand softening to finish the disinflation job.

Financial conditions, meanwhile, remain relatively accommodative. Credit spreads have widened only modestly, equity markets have recouped losses, and the weaker U.S. dollar has taken some pressure off export-oriented sectors. This backdrop buys the Fed time: Chair Powell’s repeated refrain is that they would rather risk being a little late to ease than underestimate sticky price pressures. Current market pricing suggests September is the earliest realistic window for a rate cut, with the path beyond still highly data dependent.

Source: Bloomberg

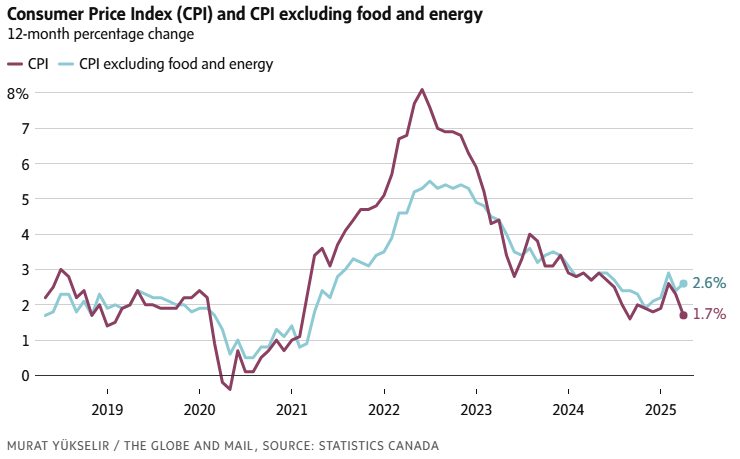

Canada Inflation: Softening Inflation as Growth Stalls

In Canada, the inflation picture is more nuanced but echoes the same underlying tug-of-war. Headline CPI eased to 1.7% in April, driven by lower fuel costs and the removal of the federal carbon tax. Yet the Bank of Canada’s preferred core measures have hovered stubbornly near 3% for most of the spring, reflecting the residual impact of supply chain rerouting and higher input costs as businesses scramble to adapt to the new trade environment.

The softer labor market is providing an offset. Unemployment hit 7.0% in May and is expected to drift higher by year-end as manufacturing, transportation, and wholesale trade adjust to weaker U.S. demand and double tariffs on steel and aluminum. This should, in time, feed through to wage moderation. The BoC has repeatedly flagged that sticky wage growth remains one risk to a smooth glide path for core inflation—especially if businesses struggling with higher costs feel compelled to defend margins through pricing.

On balance, financial conditions in Canada are supportive. Household debt servicing costs remain manageable despite higher interest rates, and the recent strength in the Canadian dollar—back to mid-2024 levels—has dampened some imported cost pressures. If core inflation shows a decisive downward drift, BMO Economics expects the Bank of Canada to resume easing with another 25–50 basis points of cuts before year-end, providing a buffer for households and firms adjusting to tariff-induced shocks.

Markets & Q1 Earnings Season Update

Resilient Earnings, a Relief Rally, and the Road Back from Liberation Day

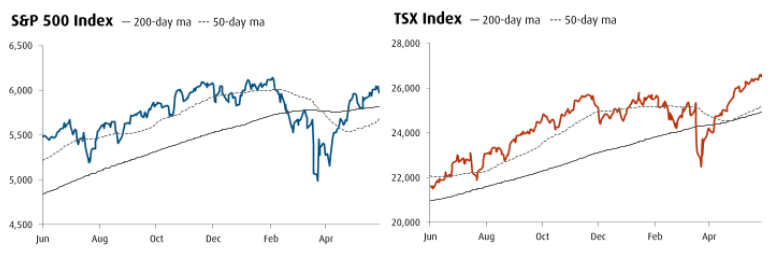

The first half of 2025 has offered investors a vivid reminder that markets tend to recalibrate more quickly than the economic headlines imply. After enduring one of the sharpest volatility spikes since the early pandemic days, driven by the surprise rollout of the “Liberation Day” tariffs, major equity benchmarks have staged an impressive rebound as policy uncertainty shifted from escalation to grudging negotiation.

Equity markets plunged in early April, briefly erasing all post-election gains and retesting levels last seen in mid-2024. Markets found their footing once it became clear that President Trump’s tariff stance, while aggressive in rhetoric, would likely settle into a structural baseline rather than an ever-rising ladder of levies. News of backchannel negotiations with China, a fragile Geneva consensus framework, and signs of flexibility in sectoral carve-outs all helped lift sentiment. Since the April lows, the S&P 500 has climbed back over 1.5% in the latest week alone and now sits just shy of its pre-Liberation Day level. The TSX has recouped most of its losses as well, helped by firmer oil prices and defensive buying in materials and financials.

Source: BMO Economics

Q1 Earnings Season: A Backward Look, A Forward Warning

Against this volatile backdrop, the Q1 earnings season delivered broadly stronger-than-feared results—though it is important to remember that these numbers mostly reflect the pre-tariff regime. Profit growth was healthy across sectors, with particular strength in large-cap technology, communications services, and selected financials. Cost controls, resilient consumer demand, and robust pricing power in services and software helped offset early signs of margin pressure in industrials and consumer goods.

However, the forward guidance painted a more sobering picture. Many industrial and consumer-facing companies used Q1 calls to withdraw or trim full-year guidance, citing persistent uncertainty around input costs, supply chain reconfigurations, and end-customer confidence. One telling metric: mentions of “recession” or “tariffs” in S&P 500 earnings transcripts jumped nearly 40% versus the prior quarter—a clear sign that management teams expect operational headwinds to persist into the second half.

On the flip side, the big technology and AI infrastructure leaders—Alphabet, Microsoft, Meta, and their peers—stood out for both reaffirming revenue growth targets and raising capital expenditure plans for data centers and AI deployment. Investors have rewarded this consistency: the Nasdaq has outpaced broader indices in the rebound, and tech remains the primary contributor to the market’s regained footing.

Central Banks & Policy Signals: Patience, Pragmatism, and the Path Ahead

If there is one thing both the Federal Reserve and the Bank of Canada have signaled consistently this year, it is that neither is in a hurry to front-run the data. With growth softening at the edges but inflation behaving better than feared, policymakers remain firmly in watchful mode—balancing two competing risks: easing too soon and reigniting price pressures, or waiting too long and risking a deeper slowdown.

Federal Reserve: Data Over Doctrine

Source: Federal Reserve Bank of New York & CNBC

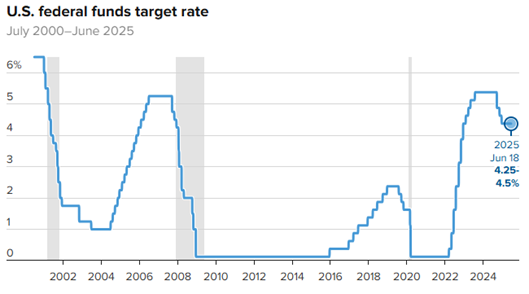

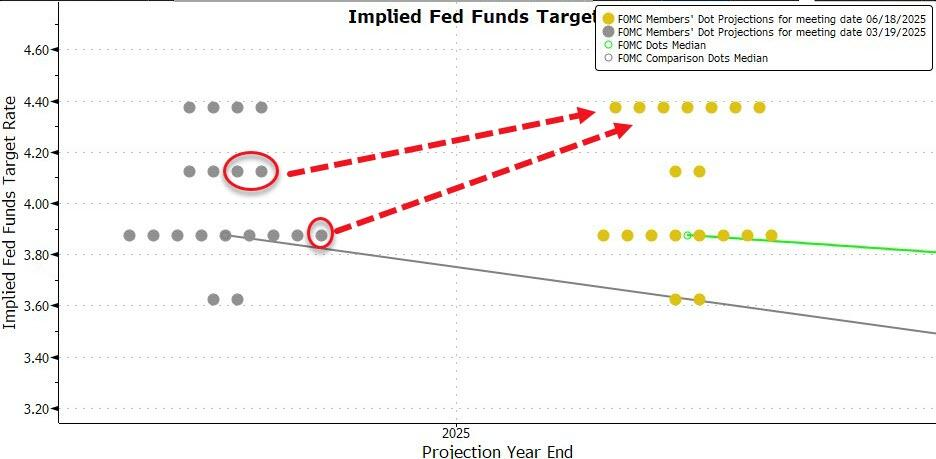

At its June 18 meeting, the Federal Open Market Committee held the fed funds target range steady at 4.25% to 4.50% for a fourth consecutive meeting, signaling that policy is likely to remain on hold a while longer as officials weigh persistent inflation risks against signs of moderating growth.

The post-meeting statement acknowledged that “uncertainty about the economic outlook has diminished but remains elevated,” underscoring the Committee’s deliberate stance. While last quarter’s stagflation alarm — where the Fed flagged simultaneous risks of higher unemployment and higher inflation — has been toned down, it has not disappeared altogether.

Fresh forecasts in the Summary of Economic Projections (SEP) skewed more stagflationary than markets had expected: for 2025, real GDP growth was revised down by 0.3 percentage points to 1.4% (Q4/Q4), while both total and core PCE inflation were lifted by 0.3 percentage points to 3.0% and 3.1%, respectively. The same directional adjustments extended into 2026, with growth trimmed slightly and inflation nudged higher, suggesting that progress toward the 2% target may be bumpier than hoped.

Source: Bloomberg

The dot plot maintained a median expectation for two 25-basis-point cuts this year, but a growing bloc within the Committee now leans toward just one — or none at all — if price pressures prove stickier as new tariffs work their way through supply chains this summer.

In his press conference, Chair Powell struck a balanced note: he described labour market trends as not yet “troubling” and characterized overall economic momentum as “decent,” affording the Fed more time to monitor how tariff-driven input costs evolve in coming months. Powell emphasized that the Committee remains highly data-dependent: if slower growth becomes the dominant story by late summer, a rate cut or two is likely; if inflation remains stubbornly above target, the hold could extend deeper into year-end.

Markets have adjusted to this more cautious tone. Short-term rate expectations have drifted to imply a September or November cut as more probable, but the path beyond remains contingent on whether core inflation and wage growth finally settle back toward the Fed’s comfort zone.

The Federal Reserve continues to weigh whether the drag from slower growth will ultimately outweigh the upward push from supply-side tariff pressures. For investors, the message is clear: policy remains restrictive for now, and any pivot to easier conditions will hinge squarely on how the next few inflation and labour reports unfold.

Bank of Canada: Between a Soft Labour Market and Sticky Core Prices

The Bank of Canada’s June hold at 2.75% was the second consecutive pause after a rapid series of cuts that brought the policy rate down from last year’s 5% peak. Governor Macklem’s accompanying statement struck a cautiously neutral tone: acknowledging the economy is softening beneath the surface while warning that rerouted supply chains and still-firm core inflation warrant patience.

Labour market cracks are widening—unemployment has risen to 7.0%, and BMO forecasts expect it could drift toward 7.5% by year-end if trade-exposed sectors continue to shed jobs. Consumer spending has turned cautious and residential construction has yet to meaningfully rebound, despite lower mortgage rates.

The Bank has made clear that it will be guided by data, not forecasts alone. With the next two CPI prints and employment reports due before the July decision, the bar for further easing is gradually lowering. If core inflation finally begins to follow headline measures down, we expect the Governing Council to resume rate cuts by late summer, with 25–50 basis points of additional easing likely before year-end.

Source: Bloomberg

Outlook: Staying Grounded as Markets and Policy Find Their Balance

As we look to the second half of 2025, one reality stands above the noise: this is not the kind of crisis that rewrites the macro playbook overnight. It is, instead, a drawn-out adjustment—a deliberate reshaping of global supply chains and trade relationships under a protectionist framework that is here to stay.

Markets have proven remarkably resilient so far. The sharp volatility spike following Liberation Day reminded us how quickly policy uncertainty can shake confidence, but the swift rebound since then reinforces a lesson that has held true across cycles: capital markets adapt long before policymakers finalize their new path.

Earnings season validated this resilience: Q1 results came in healthier than many feared, with large-cap technology and services businesses providing ballast, while more exposed industries flagged margin compression and pulled back guidance in the face of whipsawing input costs and supply chain friction.

Meanwhile, both the Federal Reserve and the Bank of Canada have made it clear that they will not overreact to political headlines or short-term data blips. Instead, they remain guided by the interplay of slowing growth, still-sticky core inflation, and the unusual fiscal cushion created by front-loaded tax relief under the OBBB.

For investors, this environment calls for discipline, not complacency:

Prioritize quality and resilience — we continue to favour companies with strong balance sheets, clear pricing power, and durable demand, especially those less reliant on complex global sourcing.

Stay balanced and diversified — a prudent mix of Canadian value and commodities, North American technology and AI leaders, and well-managed fixed income remains the bedrock of a durable portfolio.

Remain flexible — the policy backdrop will remain fluid, particularly around trade negotiations and possible tariff adjustments heading into late summer. Sharp swings in sentiment should be used to rebalance, not to chase short-term narratives.

Lean on the data, not the noise — just as the Fed and the BoC are letting the data lead, we encourage clients to do the same. Fundamental earnings power, cash flow strength, and prudent capital allocation will outlast even the loudest policy headlines.

In the months ahead, we expect the policy and trade environment to remain a source of headline noise and tactical volatility. Yet underneath that surface, resilient businesses, adaptive consumers, and prudent central banks continue to anchor the global economy. Should a bilateral Canada–U.S. trade deal emerge as signaled, we expect this could ease some of the most immediate trade headwinds for key domestic sectors and provide further support to our cautiously optimistic positioning heading into the second half of 2025.