Trump Leads a Red Wave, S&P 500 Crosses 6000, Bank of Canada and Federal Reserve Rate Cut

Christopher Bowlby - Nov 13, 2024

President Trump’s re-election as the 47th President of the United States, accompanied by a Republican majority in Congress, signals significant shifts for the U.S. economy, financial markets, and Canada’s cross-border relationship.

Trump Leads a Red Wave, S&P 500 Crosses 6000, Bank of Canada and Federal Reserve Rate Cut

The last week saw President Donald Trump re-elected as the 47th President of the United States, leading a red wave with Republicans taking majorities in both the House of Representatives and the Senate. Trump’s win marks only the second time a president has been elected to a non-consecutive second term, the first being Grover Cleveland as the 22nd and 24th president. This political shift south of the border will have significant implications for both the Canadian and U.S. economies, as well as for financial markets. Since Election Day, we have seen a dramatic rise in risk assets, as markets anticipate corporate tax cuts and a more supportive environment for mergers and acquisitions, as well as relaxed antitrust regulations from the FTC.

With Republicans now in control of all three branches of government, we anticipate a more favorable operating environment for U.S. companies. This will benefit U.S. stocks but may also bring increased protectionism and tariffs, leading to a stronger U.S. dollar and higher bond yields. As the Trump campaign continues to fill key positions in his administration, we will gain further insight into how much of his campaign rhetoric will translate into policy.

Source: BMO Economics

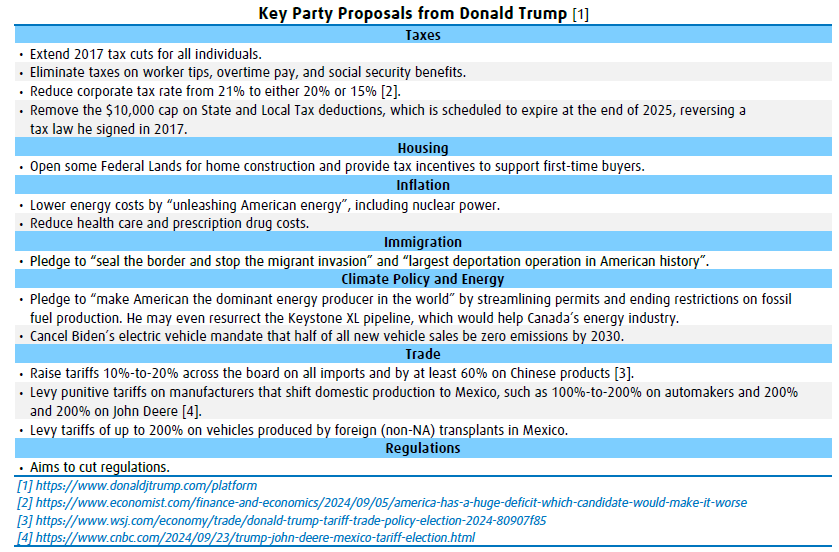

Trump 2.0

Economic Outlook

With a Republican sweep, we anticipate the swift adoption of most of Trump’s economic policy proposals, which are heavily weighted toward tax cuts and tariff increases.

Firstly, we anticipate an extension of all provisions of the Tax Cuts and Jobs Act beyond 2025. Additionally, Trump has proposed exempting overtime and tip income from taxes, ending taxation of Social Security benefits, repealing the $10,000 cap on state and local tax deductions, and lowering the corporate tax rate from the current 21% to 15%.

Trump’s tax cuts and proposed spending increases could add over $10 trillion to the federal deficit over ten years. To help offset some of these costs, Trump has proposed a 10%-20% universal baseline tariff on all imports, with a 60%-100% tariff on imports from China, potentially raising an additional $2.7 trillion in tax revenue. It is estimated that federal debt held by the public could rise to 142% of GDP by 2035, compared to 125% under current law.

For the U.S. economy, we believe we will see a boost from more accommodative fiscal policy, lighter regulation, and easier financial conditions. For example, a reduction of corporate taxes from 21% to 15% could result in a 5% increase in S&P 500 earnings per share for companies that produce goods in the United States. Furthermore, the prospect of less regulation and potentially more lax antitrust enforcement for mergers will benefit corporate America. We anticipate that any fiscal policy changes will not impact the economy until 2026.

However, these gains could be offset by protectionist measures, as higher tariffs, potential trade retaliation, and possibly higher inflation and interest rates could have adverse effects. The U.S. National Retail Federation warned that double-digit price increases could result from these tariff policies for several imported consumer goods. In the end, tariffs function as an indirect tax on consumers, potentially lowering economic growth. This impact could be exacerbated if they lead to a tit-for-tat trade war, which the European Union has already cautioned against.

Market Outlook

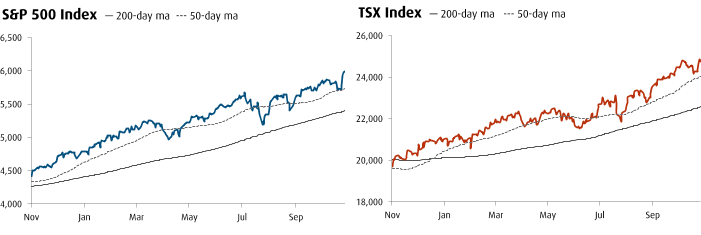

Following the election results, we saw the largest move in equity markets in the history of the S&P 500. Looking forward to 2025 and beyond, we believe that benefits from lower corporate taxes will support the robust earnings growth seen over the past year. We expect that the combination of an easier operating environment for corporations, decreasing interest rates, and strong earnings momentum will lead to continued market appreciation.

Additionally, the regulatory posture of the Federal Trade Commission and the Department of Justice’s Antitrust Division, which in the past four years challenged many proposed business combinations, will likely become more relaxed under the incoming administration. Combined with continued economic expansion and improved CEO confidence, M&A activity will likely increase. Furthermore, we anticipate a rebound in IPOs in 2025, given the coming positive macro environment.

While many U.S. companies may benefit from the projected changes under a second Trump presidency, there will also be losers negatively affected by these policies. We anticipate a continued rise of the BRICS nations, especially following the influential 16th summit in Kazan, where four new members joined (Egypt, Ethiopia, Iran, and the UAE), and thirteen nations were added as partner countries. With the planned imposition of tariffs, particularly on China, we expect to see further detachment between the G10 and BRICS economies.

Implications for Canada

Due to the Canadian economy’s reliance on its cross-border relationship with the U.S., we believe that any short-term boost to U.S. GDP will have some spillover effects into Canada. The U.S. is Canada’s largest trading partner, purchasing 75% of Canada’s merchandise exports.

Trump’s promise to “rip up” the United States-Mexico-Canada Agreement (USMCA) when it expires in 2026 adds risk to Canada’s trade-dependent economy by potentially depressing capital flows to Canada and weakening domestic investment. During his first term, changes to the USMCA were mostly cosmetic, so we hope the outcome will be similar this time around. In the meantime, we expect any changes to the USMCA to put further pressure on the Canadian dollar and Canada’s export-dependent industries.

Finally, the federal government might need to lower corporate taxes to prevent a further loss of competitiveness, as Canadian businesses and investments may shift southward.

On the TSX, we expect companies with U.S. revenue exposure to continue outperforming the rest of the index. Additionally, many large Canadian public companies have demonstrated resilience through different political and economic regimes, and we anticipate this trend will continue throughout the second Trump presidency.

Conclusion

Overall, with President Trump’s return to office, we anticipate both positive and negative impacts on the economy and markets. Robust earnings growth should drive continued equity market appreciation into next year, although these estimates may change as the new administration’s policy agenda comes into focus. The prospect of trade conflict poses downside risks to these estimates, while potential regulatory and corporate tax changes present upside potential.

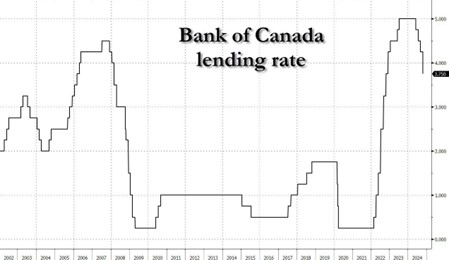

Bank of Canada October Meeting

At their October meeting, the Bank of Canada cut the overnight interest rate by 50 bps to 3.75%, a decrease of 125 bps from the peak of 5% in 2022. This larger rate cut was driven by significant forecast misses for both Q3 GDP and CPI. While the 50 bps rate cut was widely expected and fully priced in by the market, it marked an increase in aggressiveness for this easing cycle. So far in this cycle, the Bank of Canada has been the most aggressive major central bank; no other G10 bank has cut more than 100 bps, with the Federal Reserve cutting 75 bps and the Royal Bank of Australia having not yet begun to cut.

Source: Bloomberg

Surprisingly, even with the large GDP growth miss for Q3 (1.5% vs 2.8%), the Bank of Canada did not adjust its full-year forecasts for 2024 or 2025.

While the October cut was outsized, the Bank of Canada’s messaging showed little urgency to follow up with another large move; it will depend entirely on forthcoming economic data. The October cut resulted from deteriorating inflation and growth indicators over recent months. Going forward, we anticipate the Bank of Canada will return to a 25 bps rate-cut schedule, though the bank’s unchanged growth expectations leave the door open for another 50 bps cut if conditions worsen. BMO Economics forecasts that the Bank of Canada will implement five more 25 bps rate cuts over the next five meetings, bringing the Overnight Rate to 2.5% by June 2025.

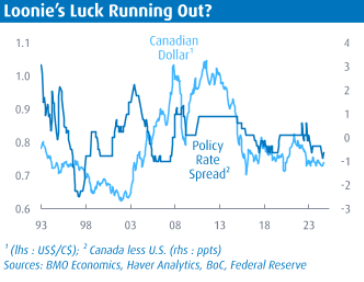

Canadian Dollar

The growing divergence in rate cuts between the Bank of Canada and the Federal Reserve has been reflected in the Canadian dollar’s weakness in 2024. With the Bank of Canada aggressively cutting interest rates amid a sluggish economy and the U.S. economy remaining resilient, the divergence in monetary policy could exert additional pressure on the Canadian dollar.

With the Federal Reserve likely to continue its 25 bps rate-cut trend, and with tariffs potentially adding inflationary pressures, policy easing in the U.S. may not be as pronounced as initially anticipated. Meanwhile, Canada’s economic momentum remains weak, and we foresee five more rate cuts over the next seven months. Furthermore, recent immigration target changes by the Canadian government point to reduced inflationary pressures in 2025, particularly in the housing sector, and slower growth. These factors continue to drive policy divergence.

So far, the Canadian dollar has held near the lower end of the range observed over the last two years, despite this divergence in rates. However, the Canadian dollar could depreciate further if the divergence continues. The last time Canada’s overnight rates were significantly lower than U.S. rates, in the mid-to-late 1990s, spreads widened from -50 bps to -250 bps within ten months, causing a 15% depreciation of the Canadian dollar over the following two years. The Bank of Canada eventually stepped in with a 100 bp rate hike in August 1998. While such depreciation is not an imminent risk, it cannot be disregarded. With President Trump indicating his intent to invoke the USMCA renegotiation clause, any broad tariff action or increased trade friction could add further pressure on the Canadian economy and dollar.

Overall, the Bank of Canada must tread carefully with its rate-cut plans, mindful of the knock-on effects a weaker Canadian dollar could have on the economy.

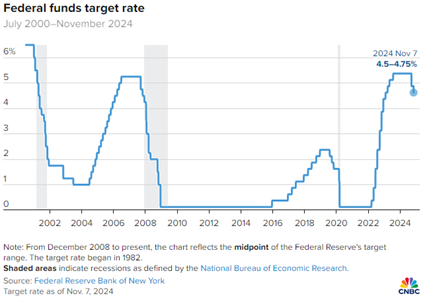

Federal Reserve November Meeting

On Thursday afternoon, in a widely anticipated move, the Federal Reserve cut the Fed Funds rate by 25 bps to a range of 4.5%-4.75% in a unanimous decision. The Fed reiterated that the pace of further reductions will depend on continued progress in lowering inflation. Additionally, the FOMC stated that the risks to the economic and inflation outlooks were “roughly balanced.” The economy continues to grow “at a solid pace,” labor markets have “generally eased,” and inflation has “made progress toward” the target, though it “remains somewhat elevated.”

This decision was in line with market expectations, resulting in minimal market reaction. During his press conference, Chairman Powell reiterated that the labor market is not contributing to inflationary pressure and that recent upward revisions to personal income have reduced some downside risks to the economic outlook.

Looking ahead, we anticipate another 25 bps rate cut at the December meeting. Chairman Powell has indicated the Fed intends to move neither too quickly nor too slowly toward a more neutral Fed Funds rate. The Fed plans to continue cutting rates cautiously, adjusting the pace as economic data evolve.

US CPI

Source: Bloomberg

On November 13th, the October CPI report revealed a monthly increase in Core CPI, with year-over-year Core CPI re-accelerating to 3.33%. While inflationary pressures remain, they are unlikely to prevent one more quarter-point rate cut before year-end. Disinflationary momentum appears to be slowing, with inflation still above the Fed’s 2.0% target. Persistent inflation in the housing and service sectors continues to offset easing pressures from goods and energy prices. The Fed’s battle against inflation is ongoing as core inflation progress has stalled. While we expect another 25 bps rate cut in December, the updated Summary of Economic Projections will be pivotal, as the number of projected rate cuts in 2025 remains uncertain.

Appendix 1