Cash Gab with Noah - February 2026

Noah Ross - Feb 01, 2026

Charitable giving is an expression of our values and commitment to community. But here’s the surprising truth: many donors aren’t making use of strategies that can significantly increase the impact of their gifts and making their donations go furth

Quick Nugget of the Day

Maximize your RRSP

The RRSP deadline is March 2, 2026. Contributions made before then can reduce your 2025 taxable income.

Why contribute now?

1. Compounding Works in Your Favour

Early contributions grow longer, and employer matching if available, is free money.

2. Strong Tax Advantages

- Growth inside an RRSP is tax defered.

- Withdrawals in retirement are usually taxed at a lower rate.

- You can carry forward unused deductions to claim in higher income years.

3. More Flexible Than People Think

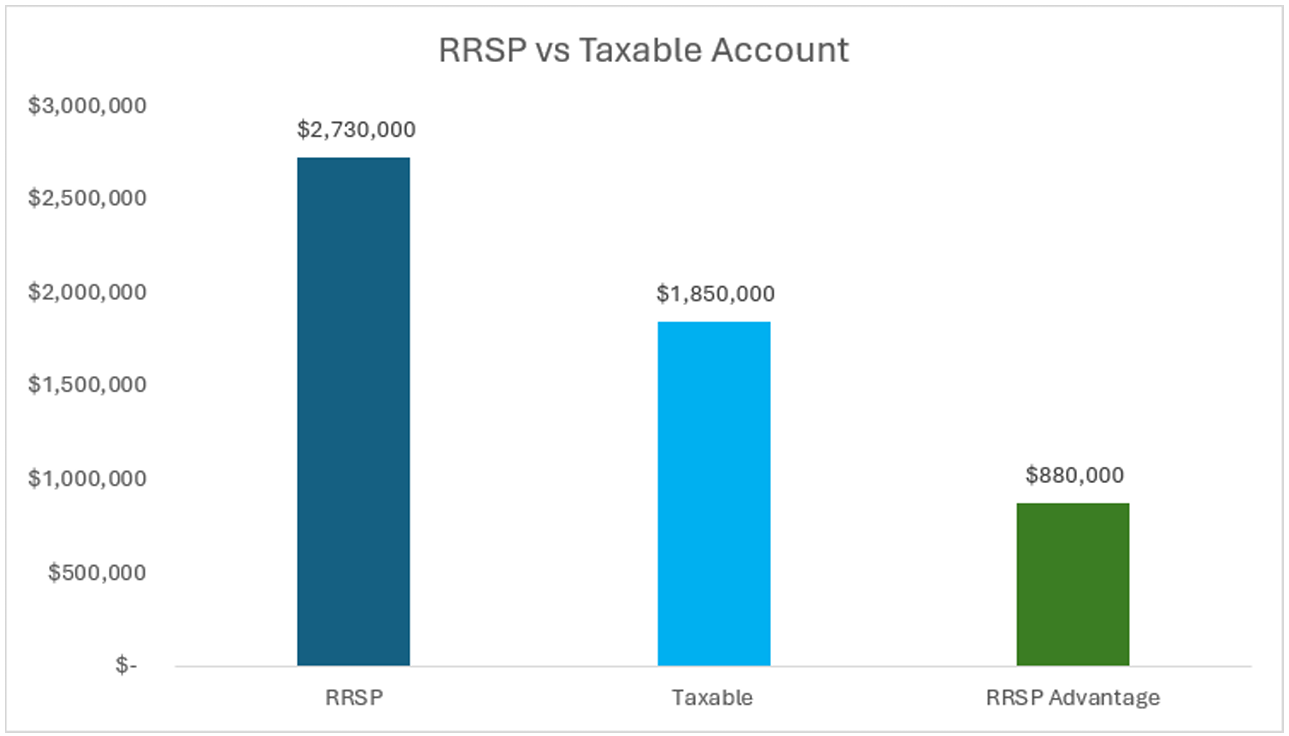

If you earn $150,000 and max your RRSP for 30 years at 7% returns, you save about $11,700 in tax each year and over $351,000 total. Choosing RRSPs over a taxable account becomes roughly a $1.23 million decision.

How to Give More for Less

Charitable giving is an expression of our values and commitment to community. But here’s the surprising truth: many donors aren’t making use of strategies that can significantly increase the impact of their gifts and making their donations go further.

By planning your donations strategically, you can make a bigger difference while being tax efficient. Here are two powerful approaches:

1. Donate Appreciated Securities Instead of Cash

If you own stocks, mutual funds, or ETFs that have grown in value, donating them directly to a registered charity can be a win-win:

- You receive a charitable tax receipt for the full market value of the investment.

- You pay no capital gains tax on the appreciation.

- The charity receives the full value of the shares.

This works best for investments held in non-registered accounts (not TFSA, RRSP, or FHSAs).

Example

You bought $10,000 of shares years ago, now worth $25,000. If you sold them:

- $15,000 capital gain x 50% inclusion = $7,500 taxable.

- At a 53.53% tax rate, you’d owe $4,015 in tax.

By donating the shares directly:

- You get a $25,000 tax receipt (worth up to $10,000 in tax savings in Ontario).

- You pay $0 in capital gains tax.

- The charity receives the full $25,000.

2. Give Tax-Efficiently Through RRSP/RRIF Withdrawals

If you’re over 71 or withdrawing from a RRIF, part of your required income can be offset with charitable giving. A donation receipt reduces the tax owed on your withdrawals.

Example

You withdraw $40,000 from your RRIF and are in the highest tax bracket (53.53%):

- Without giving: $40,000 x 53.53% = $21,412 in taxes.

- Donate $10,000 to charity:

- You receive a $10,000 tax receipt, saving over $4,000 in taxes.

- Your effective tax bill drops to $17,412.

- Net lifestyle impact is minimal, but you’ve contributed $10,000 to charity instead of paying it in taxes.

The Bottom Line

With a little planning, you can turn the same gift into a much greater contribution. These strategies can work for any registered charity in Canada and can help maximize your impact.

In the News

Chairman's Letter - 1990 - Appendix B – Warren Buffett Chairman's Letter

As Warren Buffett steps back after a lifetime of exceptional investing, his legacy is defined less by returns and more by the wisdom, humility, and humanity he shared. One of the best examples is a letter he wrote to a prospective seller, explaining why Berkshire Hathaway would be the right steward for their business.

That lens matters because selling a business isn’t just a transaction; it’s a transition.

As Buffett notes, some owners simply want liquidity and a new chapter. Others see their business as the work of a lifetime, something that still matters deeply, even if they’re ready for a different role in its future.

Many owners look back on their exit with regret because they never defined what kind of seller they wanted to be. They didn’t plan for their wealth, their time, or the identity shift that comes after stepping away. The result is avoidable stress, uncertainty, and missed opportunities to find the right buyer.

Whether you own a business or not, Buffett’s original letter is worth reading. It’s a timeless reminder of what thoughtful, long-term investment and stewardship looks like.

How Food Inflation is Making Canadians Miserable – The Globe and Mail

Food inflation remains the biggest drag on household finances, with grocery costs rising far faster than wages and forecast to jump another 4% to 6% this year. So what? To maintain or grow your savings rate, you need clarity on which costs are rising and by how much—because you can only adjust the things you can see.

How to brace for the stock market crash everyone's talking about – The Globe and Mail

The piece reminds us that even severe market drops reward investors who stay invested, keep contributing, and treat volatility as opportunity. So what? No one can predict the next correction (despite the headlines), but human nature tempts us to try. The real differentiator isn’t forecasting; it’s sticking to disciplined actions when markets get noisy.

Cash Gab Book of the Month

Book: The Gap and the Gain

Author: Dan Sullivan (with Dr. Benjamin Hardy)

Summary: This book argues that lasting happiness, motivation, and progress come from measuring yourself against your past gains, not the idealized future “gap”. A few takeaways:

- The Gap is comparing yourself to an unreachable ideal; it guarantees feelings of inadequacy and stagnation.

- The Gain is the practice of measuring backward, recognizing how far you’ve already come.

- Progress and motivation increase dramatically when you define success based on internal benchmarks.

- Gratitude/positive psychology are performance multipliers, reshaping how you experience success and growth.

Although not a personal finance book, I recommend it for anyone looking to develop a more positive relationship with money and to stay committed to their financial plan without being derailed by comparison.

The Ross Group: Who We Are

At Ross Group Wealth Advisors, we work with future-minded investors to keep them on track toward greater wealth. Through our unique approach to portfolio management and wealth planning, we deliver smart risk and tax strategies and guide sound decisions that secure their wealth and expand their lives.

What We Provide

We act as your financial quarterback, building comprehensive, long-term strategies, not quick fixes. Our wealth plans aim to minimize taxes and safeguard your financial health today and for the future.

We proactively review your portfolio and overall financial picture, update your wealth plan regularly, and ensure you stay aligned with your goals. We engage with your priorities, uncover opportunities, and challenge assumptions about what you can do and when.

Community Engagement

Subscribe!

Subscribe to the Cash Gab with Noah Newsletter to receive every issue by email as soon as it's released

In-person Cash Gab Session

What is a Cash Gab Session?

Cash Gab brings together peers in similar careers and life stages to share, listen, and learn about financial topics that matter to you. The goal is to build a community of like-minded, future-oriented people aiming to achieve financial freedom.