Markets Don’t Move in Straight Lines

Christopher Bowlby - Mar 11, 2026

Excerpt Markets don’t move in straight lines. After three strong years, 2026 has started with a more demanding mix of realities: elevated valuations, a more selective AI trade, a weaker US labour market, and an oil shock tied to war with Iran

TL;DR

The first quarter of 2026 has felt harder, but not because the market or economy have fundamentally broken. After three very strong years, investors are being forced to price a more demanding mix of realities at the same time: high starting valuations, a more selective phase of the AI trade, a weaker-than-expected labour market, and a new oil shock tied to the war in Iran.

Our view is that this looks more like a recalibration than an unraveling. Earnings have held up better than sentiment, leadership is broadening beyond the same narrow winners, and Canada has been more resilient than many expected even if the domestic economy remains soft underneath. The key message for investors is not to react dramatically, but to stay diversified, stay selective, and remember that volatility is not the same thing as broken fundamentals.

Introduction

After three very strong years for investors, 2026 has started on a more uneven path. That is not surprising. In our view, it is also not necessarily unhealthy.

Strong markets do not move higher in a straight line forever. At some point, earnings need to catch up, leadership needs to broaden, and investors need to become more selective. That feels like part of what we are seeing now.

The early months of this year have been harder not because the economy has fallen apart, but because the market has had to absorb a more difficult set of questions all at once. Expectations were high coming into the year. Artificial intelligence remained a major source of enthusiasm, but also became a source of anxiety as investors started sorting through who really benefits from it and where too much optimism had already been priced in. On top of that, the war in Iran has created an energy shock that matters less because of direct exposure in North America and more because of what higher oil prices can do to inflation, interest-rate expectations, and sentiment.

That is a lot for markets to absorb in a short period of time. What has made this stretch more difficult is not any single issue on its own, but the fact that several pressure points — valuation, AI repricing, labour-market softness, and an oil shock tied to Iran — have hit markets at the same time. In that kind of environment, the old habit of assuming every setback is a simple buying opportunity becomes less reliable, especially when the market is starting from elevated valuations rather than washed-out ones.

Still, some perspective matters. We are not writing this after a lost decade. We are writing this after three very good years. A difficult stretch after a run like that is not a sign that the market is broken. In many ways, it is the price investors pay for the gains that came before it.

Our view is that this market is still investable. But it is less forgiving than it was a year ago. Fundamentals matter more. Earnings durability matters more. Balance sheets matter more. And broad narratives, whether too optimistic or too pessimistic, deserve a little more skepticism than usual.

Why This Year Feels Harder

This year has felt harder in part because the market has been leaning on a relatively small group of winners for a long time. That can work for a while, but not forever. Eventually, expectations get high enough that even very strong companies have a harder time pushing the entire market higher on their own.

The earnings picture itself has actually held up better than the market’s mood suggests. If current estimates hold, the S&P 500 will post a sixth straight quarter of double-digit earnings growth, with first-quarter growth currently expected at roughly 11.5%. Positive guidance has also been stronger than many expected. The issue is not that earnings have collapsed. The issue is that strong fundamentals were already priced in.

That matters even more with the S&P 500 still trading above its longer-term valuation averages. When valuations are already elevated, the market becomes less forgiving of even modest disappointments. As one strategist put it bluntly: when the stock market is as expensive as it is today, it takes a much smaller predicament to create problems.

Source: BMO Economics

Three lines showing U.S. underperformance versus international markets year-to-date. Annotate the TSX all-time high on February 23 and the point where international markets decisively broke away from the S&P 500.

Source: Bloomberg

There is one other detail worth noting. Despite all the noise around tariffs this year, mentions of tariffs on corporate earnings calls actually declined for the third consecutive quarter. Companies have largely stopped treating tariffs as a new surprise. They have adapted, adjusted supply chains, and moved on. That does not mean trade policy no longer matters. It means uncertainty is increasingly being absorbed as part of the operating backdrop.

AI: Real Opportunity, Real Repricing

The same dynamic playing out across the broader market is playing out with particular intensity inside the AI trade. We have moved past the easy phase, where almost anything connected to AI benefited simply from the story. The market is now asking harder questions: who will actually earn strong returns on all of this spending, which business models remain defensible, and where expectations ran too far ahead of reality.

One place that question landed hard was enterprise software. Some of those names sold off sharply, and in our view the market may have painted with too broad a brush. The best enterprise software businesses are deeply embedded inside large organizations and are not easily replaced overnight. Not every business will win, but the first market reaction is often broader than the reality that follows.

Part of what the market is repricing is not just near-term growth, but the durability of moats, pricing power, and earnings quality in software and other AI-exposed industries. That is why the move has felt so abrupt. The fear is no longer that AI will fail. It is that AI will succeed, and in doing so challenge business models investors once treated as safe — across software, professional services, media, and finance. Investors are no longer rewarding the entire theme indiscriminately.

It is also worth understanding where the largest technology companies now stand as a group, because the story has fractured in a way that is genuinely new. For most of the past two years, those names moved together. This quarter they have not. They are increasingly being evaluated company by company, on fundamentals and on credibility. That is a healthier dynamic, even if it feels messier in the moment.

The money that has left some of the more expensive software and AI-linked names has not simply gone to cash. A meaningful share has rotated into more defensive and asset-heavy parts of the market, including utilities, industrials, consumer staples, financials, and other businesses perceived to have steadier cash flows and less direct disruption risk.

That is one reason this period looks more like a handoff than a breakdown. Beneath the surface, participation has broadened beyond the same narrow set of winners that defined much of the last cycle. The market may feel less smooth, but it is arguably becoming healthier.

The takeaway is straightforward. This looks less like the end of the AI trade and more like the next phase of it. Investors are becoming more selective, both within technology and outside it. Leadership may broaden, winners and losers will become clearer, and the market may reward discipline more than excitement for a while.

The Iran War is Mostly an Energy Story for North America

For investors here at home, the military detail matters less than the transmission mechanism.

This is primarily an energy-price story. Higher energy prices do not just affect the cost of filling up a car. They lift inflation expectations, weigh on consumer confidence, and make the Federal Reserve’s job harder at exactly the moment that parts of the economy are already slowing. That is why an oil shock can raise stagflation risk so quickly: higher inflation at the same time as weaker growth is a difficult combination for both policymakers and markets.

History also suggests that markets do not respond to conflict in a uniform way. The economic impact depends on how long the event lasts, whether supply is actually disrupted, and how much risk had already been priced in beforehand. Conflict acts as an amplifier, not the whole story.

Source: WSJ

The key variable from here is not simply whether the conflict continues, but whether the disruption to energy flows proves brief or prolonged. That will determine whether this remains a headline shock or becomes a more meaningful macro problem. BlackRock’s framing is useful here: markets appear to be pricing a disruption measured in weeks rather than in months, with the heaviest pressure falling on energy-importing regions.

The relative good news is that Canada and the United States are better positioned than many regions to absorb this kind of shock. Even so, being a major energy producer does not fully shield an economy from higher global oil prices. Consumers and businesses still pay world prices for fuel and heating, while the benefits of higher prices are concentrated more narrowly. In Canada, that also means the impact is uneven across regions: oil-producing provinces are better insulated, while much of the rest of the country still feels the drag through higher inflation and weaker confidence.

It also connects more directly to the AI story than it may first appear. Building chips, data centres, and digital infrastructure is energy-intensive, which means a sustained energy shock can pressure both the supply chain behind AI and the broader market that has been depending on it.

The takeaway is simple. The Iran conflict deserves to be watched closely, and we are watching it. But for Canadian and American investors, it is best understood as an oil and inflation story first, not as a signal that the domestic economy is suddenly facing the same pressures bearing down on every part of the world.

The Labour Market and What it Means for Rates

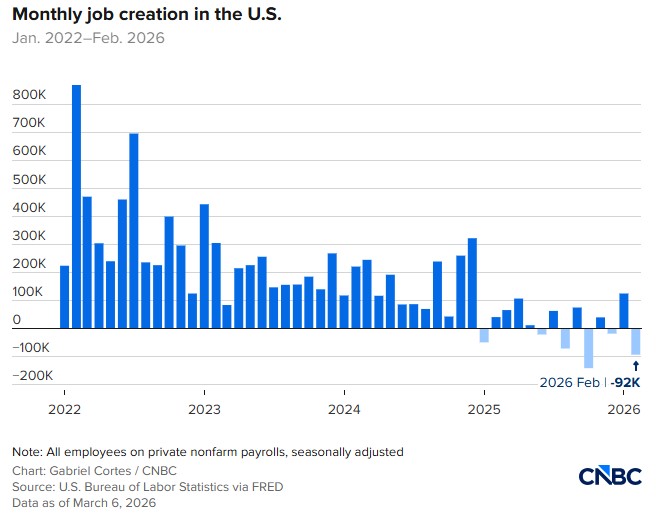

Central banks came into 2026 with less room to help than many investors were expecting, and a weaker labour market has made the picture more complicated.

Recent payroll data in the United States came in softer than expected, and revisions showed the labour market had already been weaker than many believed. That changes the context for everything else.

At the same time, growth has still felt more resilient than a weak payroll number alone might suggest. Consumer spending has become increasingly concentrated among higher-income households, which tend to be less sensitive to ordinary labour-market weakness but more exposed to falling asset prices. That helps explain why the economy can weaken without immediately rolling over.

That is the bind for central banks. A softening labour market argues for cutting rates. Energy-driven inflation argues for holding or even raising them. It is also worth remembering that, before the oil shock, inflation had actually been moving in the right direction. What changed was not that inflation had already become unmanageable on its own, but that a new commodity shock arrived at exactly the wrong moment.

The Bank of Canada held its policy rate at 2.25% in late January, while the Federal Reserve held its rate in a range of 3.50% to 3.75%. Even before the latest energy shock, both central banks were already signaling little urgency to move quickly. That already limited the odds of meaningful rate relief in Canada, and the oil shock only reinforces that point.

Our base case is that Canada is likely done cutting unless the economy weakens enough to force the Bank’s hand. In the United States, cuts still look possible, but probably on a slower timetable than markets were hoping for at the start of the year.

There is also a transition question in the United States. Jerome Powell’s term ends in May, and the question of who leads the Federal Reserve next has started to draw more attention. Leadership changes at central banks can create short-term noise even when the underlying policy direction stays intact.

The takeaway is simple. Markets may get less help from central banks this year than they were counting on. That does not mean the outlook is poor. It does mean company fundamentals may need to do more of the work, and investors may need to be a little less reliant on the assumption that policy will quickly smooth over every setback.

What This Means For Portfolios And Planning

The core point for clients is simple. A market like this does not call for dramatic changes. It calls for perspective.

After three strong years, some volatility is normal. In fact, it is healthy. Markets need time to digest gains, reset expectations, and allow more companies to take part in the next phase of the advance. That can feel frustrating in the moment. But frustration is not the same thing as lasting damage.

It also reinforces why diversification matters. When one narrow group of stocks is doing most of the work, portfolios can start to feel more dependent on a single story than they really should be. Strong long-term returns are rarely built that way.

That matters even more in an environment where central banks may be less able to provide support than they were a year ago. If rates stay higher for longer and leadership broadens beyond the same handful of winners, then the quality of the businesses you own starts to matter more. Balance sheets matter more. Cash flow matters more. Pricing power matters more.

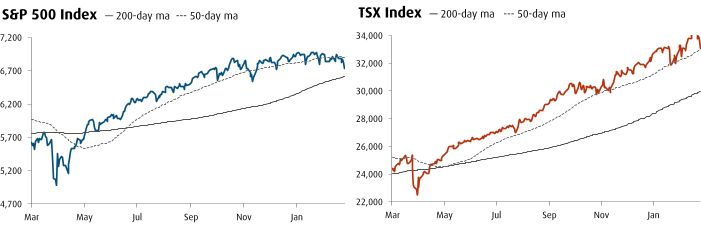

It is also worth noting something that may have surprised investors who ended last year focused on Canada’s risks rather than its strengths. The TSX hit an all-time high in February and has outperformed the S&P 500 by a meaningful margin so far this year. That is not an accident. It reflects stronger bank earnings, commodity exposure that benefits from higher energy prices, and a domestic economy that has held up better than the headlines suggested. The Canadian banks in particular delivered a standout quarter, with all six major institutions beating expectations and generating roughly $19 billion in combined profit. At the same time, the underlying Canadian growth picture has remained soft. Equity-market resilience is not the same thing as broad economic strength.

It is also becoming clearer that Canada’s policy posture is shifting, at least at the margin, from trade diversification as a slogan toward capital attraction as a strategy. Infrastructure investment, industrial partnerships, critical minerals, energy security, and supply-chain integration are all areas where capital flows can support Canadian earnings and asset values even before the full trade benefit shows up in the macro data.

The fixed-income side of the portfolio still plays an important role in moments like this. It is not there to win headlines. It is there to provide structure, income, and a counterweight while equity markets work through a noisier period. As the events of recent weeks have demonstrated, in an inflation-driven shock, bonds and equities can fall at the same time, and traditional safe havens may not behave as neatly as investors expect in the short run. That is a reminder to favour high-quality, shorter-duration fixed income rather than reaching for yield. The goal is stability, not excitement.

The takeaway is straightforward. We would view this environment less as a reason to retreat and more as a reminder to stay disciplined. The market is still investable. It just may reward patience, diversification, and quality more than momentum for a while.

Volatility is not the same thing as broken fundamentals. In our view, this remains a market that is recalibrating, not unraveling.

For long-term investors, the message is not to react dramatically to a harder stretch of market behaviour. It is to stay diversified, stay selective, and keep decisions anchored to a sound plan rather than to headlines. This remains a more demanding market, but not a broken one.