TL;DR

Markets are at or near record highs, even though the headlines remain uncomfortable.

If you only looked at the major indexes, you would not know there was a military conflict involving Iran, disruption around the Strait of Hormuz, or oil trading at levels that would normally make investors more cautious. That disconnect can feel strange, but it is not necessarily irrational.

Markets do not move on headlines alone. They move on how those headlines are expected to affect earnings, inflation, interest rates, liquidity, and future cash flows. Right now, investors are not saying the risks have disappeared. They are saying those risks have not yet overwhelmed the earnings story.

The first quarter earnings season was strong. AI-related capital spending continues to drive a meaningful share of market leadership. Semiconductor and infrastructure companies remain central to that story. Oil is a risk, but so far markets are treating the Iran and Hormuz disruption as an energy and inflation shock rather than a broad economic break. Inflation remains the main macro constraint in both Canada and the United States. And the IPO market, especially around large private technology and AI-linked companies, may become one of the most important tests of public-market risk appetite in years.

Our view is that this remains an investable market, but not an easy one. Record highs are not a reason to abandon discipline. They are a reason to be more selective about what you own and why you own it.

Introduction

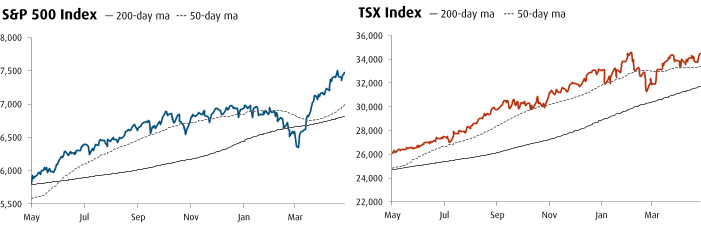

After a strong run for global equity markets, investors are facing an uncomfortable contradiction.

On one hand, major indexes are at or near all-time highs. Technology shares have regained momentum. Semiconductor stocks have pushed higher. AI-related enthusiasm has returned. Earnings have generally held up better than many expected.

On the other hand, the macro backdrop does not feel calm. The conflict involving Iran has raised serious energy-market concerns. The Strait of Hormuz remains one of the most important chokepoints in the global energy system. Oil has moved sharply. Inflation has become harder to dismiss. Central banks have less room to provide quick relief. Valuations are not cheap.

That is a lot for markets to absorb.

What makes this moment unusual is not that risks exist. Risks always exist. What makes this moment unusual is that the market has continued to climb while those risks are visible in plain sight.

That does not mean investors are ignoring the risks. It means markets are trying to sort out which risks are temporary, which risks will transmit into the economy, and which risks could permanently impair earnings.

That distinction matters.

A market at record highs is not necessarily a complacent market. Sometimes it is a market that has looked at the risks, assigned a probability to them, and decided that earnings, liquidity, and visible growth still deserve a higher price.

The job for investors is not to pretend the risks are gone. It is to separate risks that create volatility from risks that change the long-term value of the businesses they own.

Source: BMO Economics

Markets Are Not a Newspaper

One of the hardest parts of investing is accepting that markets do not always respond to the world the way people emotionally expect them to.

Bad headlines do not automatically create bad markets. Good headlines do not automatically create strong markets. Markets are forward-looking, imperfect, and often frustratingly unemotional.

They are not trying to measure how serious a headline feels. They are trying to measure whether that headline changes the path of earnings, inflation, interest rates, credit conditions, or liquidity.

That is why two things can be true at the same time.

The conflict involving Iran can be serious.

The Strait of Hormuz can matter.

Oil can be a genuine inflation risk.

And markets can still move higher if investors believe the shock is contained, earnings are resilient, and the companies leading the market can continue to grow.

That is the environment we are in now.

Markets appear to be treating the Iran and Hormuz risk as a meaningful transmission risk, but not yet as a broad earnings impairment risk. In plain English, investors are not saying the conflict does not matter. They are saying it has not yet broken the earnings picture.

That may sound subtle, but it is the difference between volatility and a change in trend.

Volatility is uncomfortable. It can be sharp. It can dominate headlines for days or weeks. But volatility does not necessarily change the long-term value of a portfolio.

A change in earnings power is different. If higher oil prices persist long enough to pressure margins, weaken consumers, force central banks to stay restrictive, and reduce corporate profits, then markets would need to reprice more seriously.

So far, that is not what the market is saying.

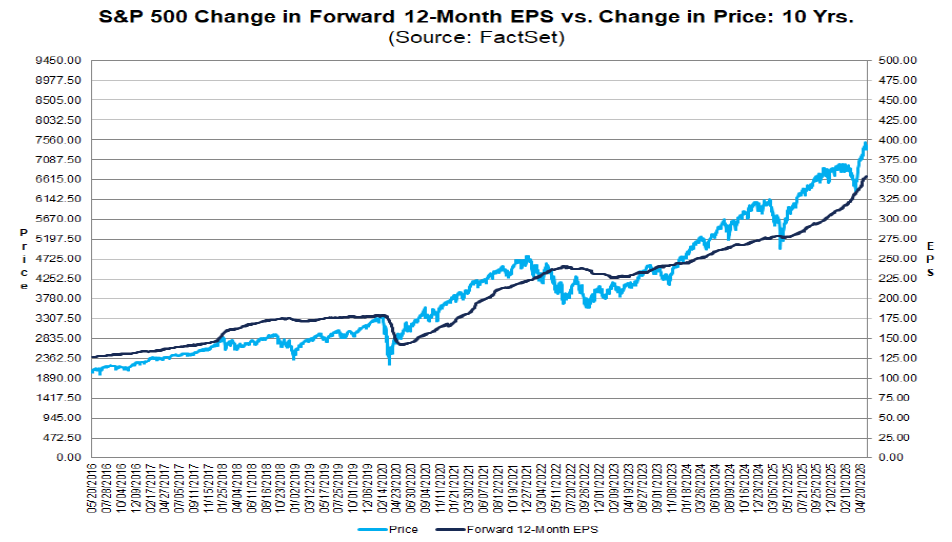

Earnings Are Still Doing the Heavy Lifting

The most important support for markets right now is earnings.

The first quarter earnings season was stronger than many investors expected. Companies beat estimates at an above-average rate, profit growth was better than feared, and guidance was generally resilient enough to keep investors focused on fundamentals rather than headlines.

That matters.

Markets can tolerate noise when earnings are improving. They have a much harder time tolerating noise when earnings are falling.

But the strength has not been evenly distributed. A large share of the positive momentum is still coming from technology, semiconductors, AI infrastructure, and companies tied to capital spending. That is why the market can look healthy at the index level while still feeling narrow underneath.

The lesson is not that the market is fragile. The lesson is that the market is selective.

Investors are rewarding companies that can turn demand into real earnings. They are rewarding pricing power, margin resilience, balance-sheet strength, and visible growth. They are being less generous toward businesses that need lower rates, cheaper fuel, stronger housing, or a broad consumer rebound to make the numbers work.

That is exactly what we should expect in a higher-rate, higher-uncertainty world.

AI Is Still the Main Equity-Leadership Story

AI remains the main equity-leadership story, but it is not the only thing that matters for diversified portfolios.

That distinction is important.

The first phase of the AI trade was mostly about excitement. Investors rewarded almost anything connected to the theme. That phase was never going to last forever. Eventually, markets had to become more selective. They had to ask which companies would actually earn strong returns on the spending, which business models had durable advantages, and where expectations had already moved too far.

That more selective phase is healthier.

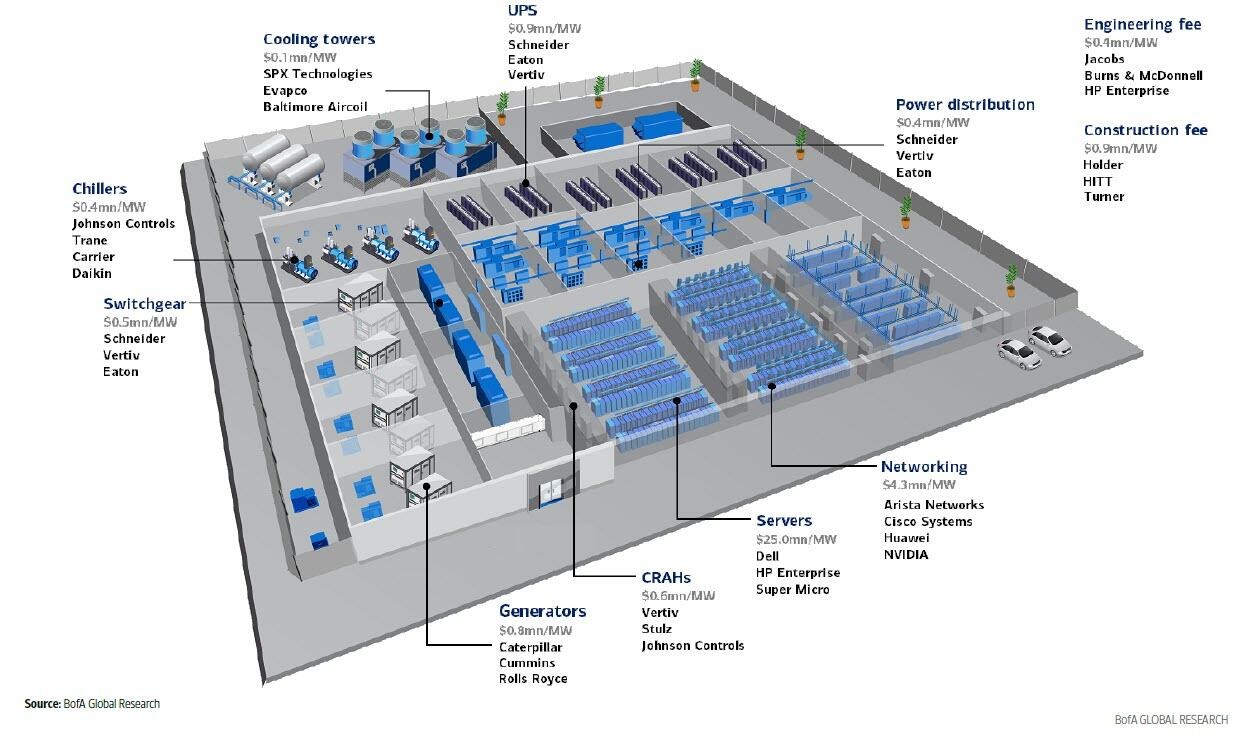

What has changed in recent months is that the market has started to treat AI less as a software story and more as a full infrastructure cycle.

The buildout is physical. It requires semiconductors, memory, networking equipment, data centers, cooling systems, power infrastructure, grid capacity, land, water, and electrical equipment. It also requires enormous amounts of capital.

That is why semiconductor stocks remain so central. It is why memory, networking, power equipment, and data-center infrastructure have become more important parts of the discussion. The constraint is not just computing power. The constraint is the entire supply chain required to deploy computing power at scale.

That is not a minor shift. It shows how deeply the AI infrastructure theme is now tied to index-level market leadership.

There is also an important portfolio lesson here.

A real theme can still become crowded. A great company can still become expensive. A powerful secular trend can still produce disappointing returns if investors pay too much for it.

The question is no longer whether AI is real. It is. The question is where the durable earnings will accrue, which companies can defend margins, and what return is left after the market has already recognized the opportunity.

For portfolios that already have meaningful exposure to technology, semiconductors, and AI infrastructure, the next step is not simply to add more of what has worked. It is to make sure the exposure is intentional. The best businesses in a theme are not always the best incremental buys after a strong run. We continue to separate the validity of the AI buildout from the price being paid for each company inside it.

The IPO Market May Be the Next Big Test

The IPO market may become one of the more important tests of risk appetite over the next year.

This is not because clients should chase IPOs. They should not.

It matters because IPO windows tell us something about liquidity, investor confidence, and the market’s willingness to fund long-duration growth.

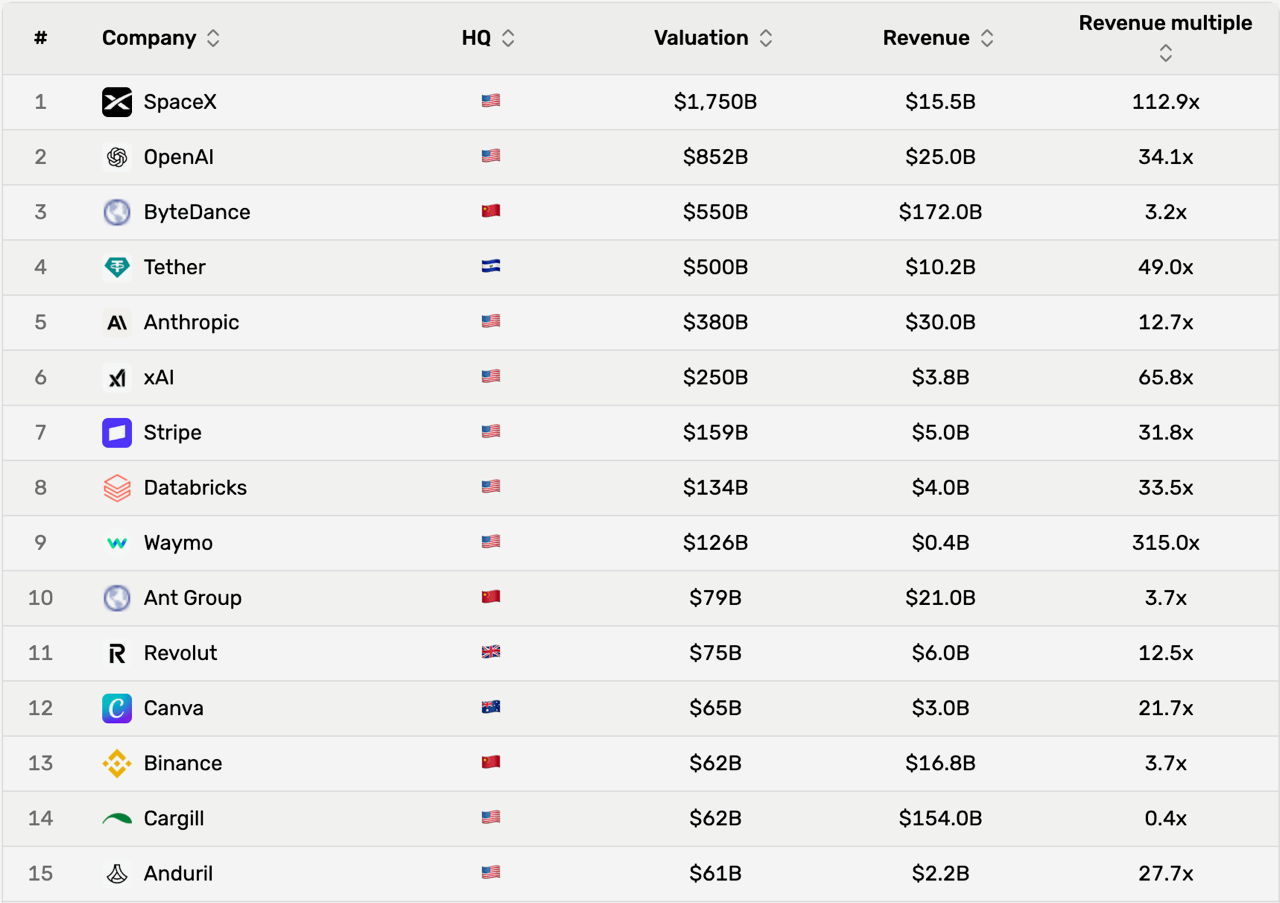

The potential scale is unusual. We are now talking about private companies that could come public at valuation levels that would have seemed almost impossible a decade ago. SpaceX, OpenAI, Anthropic, and other large private technology companies are not small speculative listings. They are potential public-market events measured in the hundreds of billions, and in some cases potentially north of a trillion dollars if they come to market near recent private-market valuation markers.

Those figures are not final offering terms. Timing can change. Valuation can change. Float can change. Investor demand can change. But the direction of travel matters.

The largest private companies preparing for public markets are not traditional industrials, retailers, banks, or energy producers. They are companies tied to artificial intelligence, space infrastructure, data, compute, and frontier technology.

That reinforces the same point: AI is not a side theme in this market. It is the main equity-leadership story.

But the IPO section deserves discipline, not excitement.

A healthy IPO market can support sentiment. It can improve liquidity. It can signal that public markets are willing to finance growth again. It can also test how much risk investors are willing to absorb at elevated valuations.

There is a difference between a company being important and a stock being attractive. There is a difference between a technology being transformational and an IPO being priced with a margin of safety.

This is especially important when private-market valuations are this large. At a certain point, the question is not simply whether the company is exciting. The question is whether public-market investors are being asked to pay today for earnings power that may still be years away.

That is why the IPO window is so important. It will tell us whether the market’s appetite for AI is disciplined or indiscriminate.

A healthy market can absorb large new listings if the fundamentals are credible, the float is manageable, and investors believe the path to profitability is real. A more speculative market will treat size itself as a reason to buy.

We would rather see the first version.

The IPO market is a sentiment test, not a portfolio instruction.

Source: Multiples VC

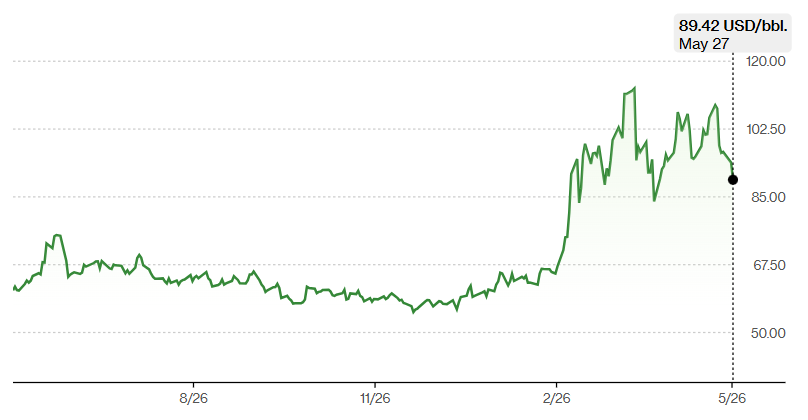

Oil and Hormuz Matter, But the Path Matters More Than the Level

The conflict involving Iran and the disruption around the Strait of Hormuz created a real energy shock.

Oil moved sharply higher. Markets had to price the risk that higher fuel costs could feed inflation, pressure consumers, and make central banks less willing to cut rates. That risk is real.

The Strait of Hormuz is not a minor shipping route. It is one of the world’s most important energy chokepoints. Any disruption there can quickly affect oil markets, transportation costs, inflation expectations, and corporate margins.

But markets are often more frightened by the speed of a price move than by the level itself.

A sudden oil spike forces investors to reprice inflation, interest rates, transportation costs, consumer spending, and profit margins all at once. A high but more orderly oil range is still a problem, but it is easier for companies and investors to digest.

That is the distinction we are watching.

Oil near the high-$90s or low-$100s is not harmless. It acts like a tax on consumers. It pressures fuel-sensitive industries. It complicates the inflation outlook. It can narrow margins for companies that cannot pass through higher costs.

But a market can absorb higher oil better than it can absorb an uncontrolled energy shock.

For Canadian and American investors, the Iran and Hormuz conflict is best understood first as an oil and inflation story, not as a signal that the domestic economy is suddenly facing a broad breakdown.

That does not make it unimportant. It makes the transmission mechanism clearer.

The key question from here is whether the disruption remains temporary and manageable, or whether it persists long enough to change inflation expectations, consumer behaviour, and central bank policy.

Source: Bloomberg

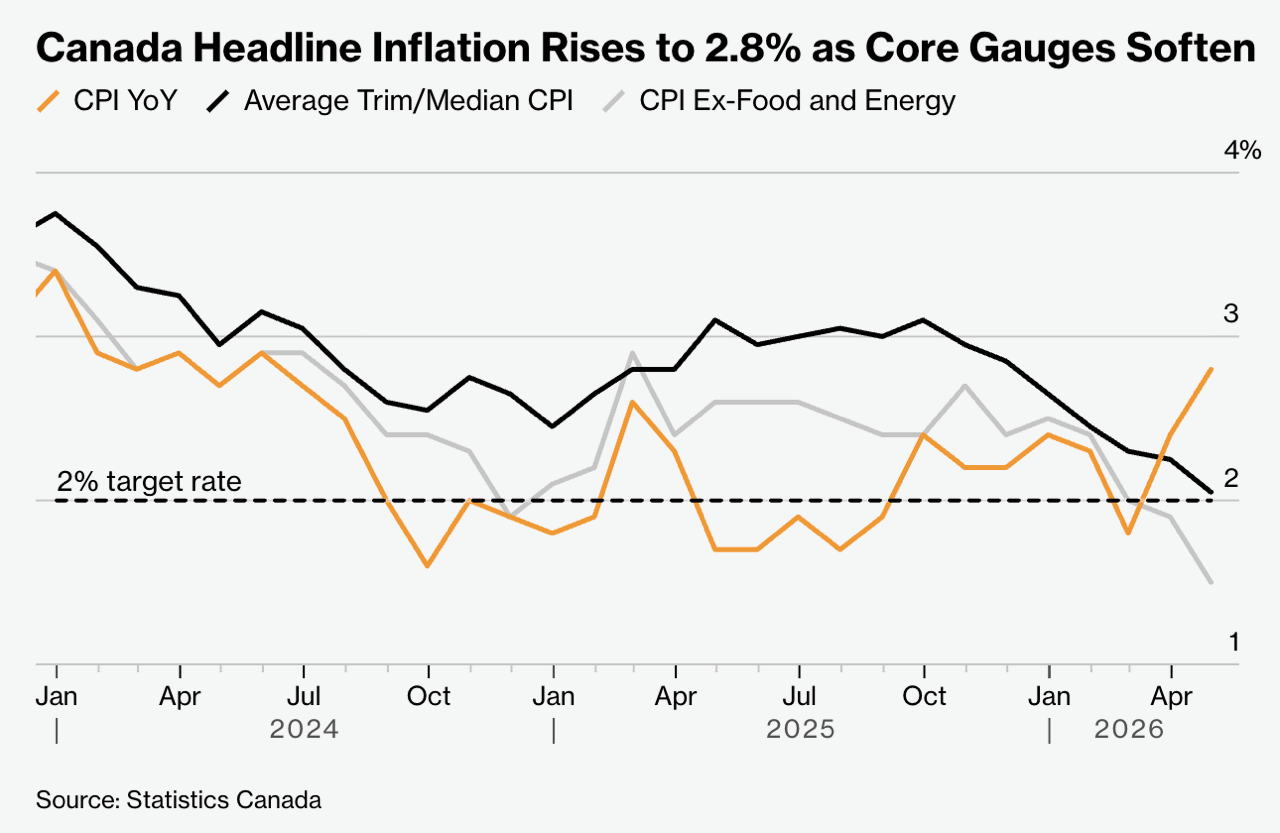

Inflation Is Still the Macro Governor

The harder issue remains inflation.

In Canada, the April inflation data were complicated by energy. Headline inflation moved higher, but the underlying picture looked less alarming once gasoline was stripped out. That gives the Bank of Canada a reason to remain cautious, but not necessarily a reason to panic.

The headline number looks hotter. The underlying picture is less alarming once gasoline is removed.

In the United States, the inflation issue is broader. Services prices, energy pressure, input costs, and tariff pass-through risk all make the Federal Reserve’s job more difficult.

Growth has held up. Earnings are still improving. But inflation has not cooled enough to make policy easy. If oil remains elevated, tariffs feed into input costs, and services inflation remains sticky, central banks have less room to provide the kind of quick support investors often expect.

That matters for portfolios.

Investors should not build around the assumption that rate cuts will quickly rescue every weak business model. If rates stay higher for longer, the companies that matter most are the ones that can fund themselves, protect margins, and grow without depending on cheap money.

This is why balance sheets matter again. It is why free cash flow matters. It is why pricing power matters. It is why selectivity matters.

Source: Bloomberg

Why Record Highs Can Feel Uncomfortable

Record highs often make investors uncomfortable.

That is understandable. When markets are falling, investors worry about what they have lost. When markets are rising, they worry about what could go wrong next.

That is the emotional paradox of investing. There is rarely a moment when the market feels perfectly safe.

At record highs, the concerns become more specific. Are valuations too high? Is the market too dependent on AI? Are investors ignoring geopolitical risk? Are earnings as strong as they look? Is the IPO window a sign of healthy liquidity or late-cycle enthusiasm?

Those are the right questions.

But the existence of those questions does not mean the market is broken. It means discipline matters more.

A market at record highs can still move higher if earnings continue to grow. It can also become more vulnerable to disappointment if expectations become too high. Both are true.

The answer is not to retreat simply because the market is high. The answer is to be more demanding.

Own businesses that can justify their valuations. Favour companies with durable demand, strong cash flow, pricing power, and balance sheets that can handle a higher-rate world. Be careful with crowded themes. Avoid companies that need everything to go right.

This is not a market that rewards broad enthusiasm. It is a market that rewards disciplined participation.

What This Means for Portfolios and Planning

The core point for clients is simple.

A market like this does not call for dramatic changes. It calls for perspective.

The market is not saying there are no risks. It is saying the risks have not yet changed the earnings picture enough to overwhelm the companies leading the market.

That could change. Oil could move higher. Inflation could become stickier. Central banks could stay restrictive longer than investors expect. AI-related valuations could get stretched. The IPO market could become too enthusiastic. These are real risks, and they deserve attention.

But the right response is not to retreat from equities every time the headlines get worse. The right response is to stay invested with discipline.

New capital still needs company-level proof. In this environment, we want to see pricing power, backlog strength, margin resilience, balance-sheet quality, and a valuation that leaves room for future returns. A powerful theme may explain why a business matters, but it does not automatically tell us what the stock is worth.

In equities, that means favouring quality businesses with durable earnings, strong margins, good balance sheets, and the ability to convert demand into cash flow.

In technology, it means recognizing that AI remains a powerful theme, while also accepting that not every AI-related company will be a winner and not every winner will be attractive at any price.

In fixed income, it means remembering that bonds still play an important role, but the quality and duration of that exposure matter. In an inflation-driven shock, bonds and equities can come under pressure at the same time. That is why we continue to favour high-quality fixed income rather than reaching for yield.

In portfolio construction, it means diversification still matters. A market driven by a narrow set of companies can produce strong returns for a while, but long-term portfolios should not depend entirely on one story, one sector, or one macro outcome.

The goal is not to predict every headline. The goal is to build portfolios that can withstand a range of outcomes.

The Bottom Line

Markets are not ignoring the risks. They are weighing them.

They are weighing Iran and Hormuz against earnings. They are weighing oil against AI infrastructure. They are weighing inflation against liquidity. They are weighing record highs against the possibility that profits can continue to grow.

That balance may change. It always can.

But for now, the message from markets is not that everything is fine. The message is that the risks have not yet broken the fundamental story.

That is why our view remains steady.

This is still an investable market. It is just not a market that rewards complacency. The opportunity is not in chasing the index because it is going up. It is in owning companies with durable earnings, pricing power, strong balance sheets, and exposure to real demand.

Record highs do not mean risk has disappeared. They mean discipline matters more.