Increased Volatility and US China Trade War Escalation

Christopher Bowlby - Apr 11, 2025

This last week has been one of the more chaotic weeks in our investing careers, with markets reacting quickly to both changed economic assumptions, social media posts and an escalating trade war between the US and China.

This past week delivered a sequence of shocks that may come to define the end of the post-globalization era. What began with a press conference and a Truth Social post evolved into a series of cascading policy announcements, retaliatory moves, and market dislocations—each more consequential than the last. The result is not just volatility, but a new regime: one defined by transactional diplomacy, politicized trade, and the erosion of the norms that once underpinned the global economic system.

At the center of this realignment is President Trump’s “Liberation Day” tariff plan. Following his re-election, the administration has moved swiftly to implement a sweeping restructuring of trade relationships. The core framework is deceptively simple: a 10% universal tariff on all imports into the U.S., layered with country-specific “reciprocal” tariffs based solely on bilateral trade deficits. This approach ignores capital flows, services trade, and global production chains.

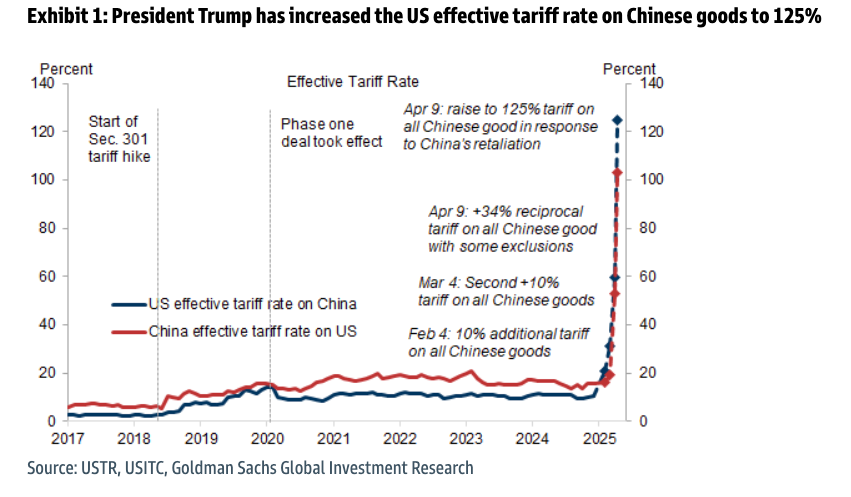

Among the hardest-hit are export-reliant economies like Vietnam, where U.S.-bound exports account for nearly 30% of GDP. Other countries scrambled to negotiate exemptions or signal goodwill. Yet the true target of this policy architecture is China, which now faces a 145% tariff rate on its goods, triggering direct retaliation. In return, China has imposed a 125% tariff on U.S. goods, curbed cultural imports, tightened regulatory scrutiny of U.S. firms, and delayed critical rare earth exports. What’s emerging is not simply a trade spat—it is a full-spectrum economic decoupling.

While many hoped that the White House’s April 9 announcement of a 90-day pause on reciprocal tariffs for non-retaliators might signal a pivot, markets saw it for what it was: a delay, not a detente. The universal 10% tariff remains in place, and the escalation with China continues unabated. BMO Capital Markets summarized it best: this isn’t emergency policy—it’s “elective surgery” for an economy that wasn’t sick. With U.S. GDP growth trending near 3%, inflation down from its post-pandemic highs, and unemployment at multi-decade lows, the move appears ideologically driven, not cyclical.

Financial markets reacted swiftly. U.S. equities tumbled early in the week, briefly rallied on rumors of the pause, and then reversed again as the broader implications became clear. The S&P 500 closed the week down 2.9%. Treasury markets experienced one of the sharpest bear steepenings in years, with the 10-year yield surging above 4.4% and 30-year bonds breaching 5%. The dollar, traditionally a safe haven in times of uncertainty, weakened broadly—down more than 3% since April 2—while gold hit a new all-time high. Liquidity drained rapidly as bid-ask spreads widened and risk tolerance evaporated.

Part of the strain stemmed from the collapse of the basis trade—a once-reliable arbitrage strategy employed by large macro hedge funds like Citadel, Millennium, and Point72. These funds exploit small pricing discrepancies between Treasury futures and the underlying cash bonds, typically using significant leverage. But with bond yields spiking and price volatility surging, margin calls forced abrupt deleveraging. This created a feedback loop, where rising yields drove liquidation, which in turn drove yields higher.

At the same time, algorithmic trading flows amplified the swings, often front-running human comprehension. On Tuesday, the S&P 500 surged 7.5% within minutes after a blue-check “Walter Bloomberg” account posted a false rumor of a full tariff rollback. The White House denied it within 10 minutes—but by then, the market had already spiked and retraced most of the move. The next day, a Truth Social post from President Trump announcing the 90-day pause triggered an even sharper rally. In both cases, by the time traditional media reported the headline, the trade was already over. This is what volatility looks like in an AI-amplified, automated trading market structure.

Another underappreciated factor this week has been the absence of corporate buybacks. With Q1 earnings season approaching, most U.S. companies are in blackout windows, removing an estimated $3 to $5 billion of daily natural buying support from equity markets. In periods of elevated volatility, this missing bid becomes glaringly obvious—and reinforces the fragility of a market increasingly dependent on liquidity over fundamentals.

Beyond the markets, real economic damage is already underway. According to Vizion Inc., global container bookings dropped sharply in early April, as firms paused shipments amid tariff confusion. There are confirmed reports of Chinese shipments being canceled mid-route, and U.S. LNG exports redirected from China to Europe. After the April 9 pause, logistics providers reported a brief surge in orders as firms front-loaded shipments to beat potential tariff hikes—further distorting inventory data and near-term GDP prints.

Geopolitically, the tariff structure is being used not merely as an economic tool, but as leverage to enforce alignment. Exemptions and concessions appear increasingly tied not just to market access, but to strategic behavior. Nations are being asked to demonstrate loyalty—not just by opening their markets, but by pivoting away from China. LNG deals, military contracts, and pledges of U.S. investment have all been used as bargaining chips. This creates profound tensions for allies whose economies are deeply intertwined with both superpowers.

The European Union, for now, has paused retaliation and offered modest concessions. Yet internal fractures are surfacing. Spain’s Prime Minister visited China for the third time in two years this week, advocating for deeper ties in EVs and agriculture. EU officials have made clear they will resist binary choices. But if tariffs extend to pharmaceuticals or agri-tech—a real possibility—the calculus may shift. The outcome is not likely to be a multilateral resolution, but a fragmented world of overlapping, contested trade blocs.

Against this backdrop, corporate America faces Q1 earnings with little clarity. We expect weak forward guidance, increasing CapEx directed at supply chain resilience, and rising input costs. Investors should watch carefully for commentary on reshoring, vendor diversification, and pricing power. This earnings season is not just a scorecard—it is a strategic status update.

In Canada, we are already seeing signs of strain. The March employment report showed the largest private-sector job loss in three years. With headline CPI expected to tick up to 2.7% in April, and the loonie surging to a five-month high, the Bank of Canada’s room to maneuver is narrowing.

This week didn’t just bring volatility—it redefined it. Markets are no longer reacting to the cycle. They are reacting to a systemic reordering of the global economy. We anticipate prolonged instability, sudden reversals, and a world where risk is driven not by fundamentals, but by political will and power dynamics.

Throughout this volatility, we have been selectively adding new positions in a few high-quality companies that remain relatively insulated from the global tariff drama that have defensive free cash flow and revenue generation as well as adding to core position that are trading at a discount from their January highs. Furthermore, we are looking for opportunities to lengthen our bond portfolio duration to benefit from a spike of Canadian bond yields and credit spreads. Throughout all of this confusion and volatility, we remind ourselves and our clients that trying to time the market is a fool’s errand and while it is quite jarring to see portfolio values go down, we must remember to ignore the noise, as hard as that may be, and stay the course because even with this most recent flare-up the stock market is a market of individual stocks and high quality corporate fundamentals drive long term appreciation.

If you would like to chat more or if you have any questions, please feel free to reach out.

Debbie, Chris Mark and Rosemary