“Liberation Day”, Tariffs, and International Trade Regime Change

Christopher Bowlby - Apr 04, 2025

The U.S. administration’s “Liberation Day” tariff announcement—initially dismissed as posturing—materialized into the most sweeping shift in U.S. trade policy in a century, triggering a material repricing of global economic risk.

The first quarter of 2025 will likely be remembered not for what markets feared might happen, but for what did. The U.S. administration’s “Liberation Day” tariff announcement—initially dismissed as posturing—materialized into the most sweeping shift in U.S. trade policy in a century, triggering a material repricing of global economic risk.

Equity markets corrected, inflation expectations firmed, recession forecasts were revised upward, and the resilience of portfolios was put to the test. For investors, it was a quarter defined by dislocation—but also one where discipline, diversification, and decisiveness again proved their worth.

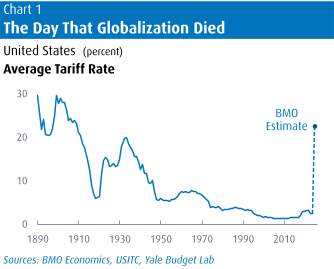

The Largest Tax Hike Since 1968

On April 5, the U.S. government enacted a 10% baseline tariff on all imports, excluding Canada and Mexico. Four days later, a second layer of tariffs came into force, targeting countries running large bilateral trade deficits with the U.S. with "reciprocal" surcharges—calculated using a formula never before deployed in U.S. trade history. The result: effective tariff rates of 34% on China, 24% on Japan, 25% on South Korea, 20% on the EU, 46% on Vietnam, and similarly elevated levels across Asia.

The total policy change represents a 22 percentage point increase in the U.S. effective tariff rate this year—the largest U.S. tax hike since the Revenue Act of 1968, and the highest tariff regime since the Smoot-Hawley era of the 1930s. Unlike that period, today’s globalized economy features an import share of GDP over 11%, magnifying the potential impact on supply chains, inflation, and sentiment.

According to Goldman Sachs, while one-third of imports are temporarily exempt (including energy, autos, and critical minerals), the net impact is an increase of 12.6 percentage points in the effective tariff rate—rising to 18.8pp when accounting for other measures already announced this year. Critically, these exemptions may prove temporary, with sector-specific tariffs on pharmaceuticals, semiconductors, and copper currently under review.

A Mercantilist Framework with Nonlinear Effects

What makes the Liberation Day framework unusual—and deeply concerning—is the policy logic underpinning it. Rather than basing tariffs on clearly defined violations of trade rules or regulatory misalignments, the administration has anchored its calculations on nominal bilateral trade deficits.

Each country’s “reciprocal” tariff was determined by a mechanical formula: take the U.S. goods trade deficit with that country, divide by the total value of U.S. imports from that country, then halve the result. The outcome was a schedule of tariffs that appear to penalize countries not based on their trade policies, but on the scale of their trade surplus with the U.S.

These are stacked on top of the 10% baseline, resulting in headline-effective rates exceeding 50% in some cases. By contrast, countries like the UK, Australia, and Brazil—which run small surpluses or balanced trade—received only the baseline 10% levy. Canada and Mexico, under USMCA, were granted partial exemptions, with only non-compliant goods subject to a 25% duty.

The problem with this approach is twofold. First, it is analytically unsound. Trade deficits are not inherently indicative of unfair trade practices. They are often the result of capital flows, consumer demand, or the global role of the U.S. dollar—not predatory policies. Second, the method treats trade as a zero-sum game. It presumes that balanced trade is fair trade and that imports are inherently harmful—an idea long discredited by mainstream economics.

The lesson is clear: this approach confuses economic interdependence with exploitation.

And that’s before mentioning the now-infamous example of a remote island with no real economy—save penguins—that was still slapped with a 10% tariff under the policy’s “minimum rule.”

What’s more, the tariffs do not account for services trade, non-tariff barriers, or value-chain complexity. Countries with surpluses in goods but deficits in services are treated as offenders, while those with opaque barriers but balanced books escape scrutiny. This is mercantilism masquerading as fairness, and risks misaligning global supply chains, distorting prices, and creating inefficiencies rather than addressing real trade frictions.

Macroeconomic Repercussions: Growth Downgrades, Recession Risk, and Policy Drift

The macroeconomic consequences are significant. Tariffs function as consumption taxes—broad-based, regressive, and inflationary. We estimate the annualized revenue impact could exceed $700 billion, or 2.4% of U.S. GDP, with costs falling disproportionately on U.S. households and businesses.

As a result:

- Core PCE inflation could rise by 1–1.5%, particularly in the middle quarters of the year.

- Real disposable income growth may turn negative, eroding consumer purchasing power and sentiment.

- The probability of a U.S. and global recession in 2025 has increased.

- U.S. real GDP forecasts are being revised downward to 1.0% Q4/Q4, with risks still tilted to the downside.

These risks are compounded by what appears to be a broader policy pivot away from pro-growth orthodoxy. Rather than supporting the expansion through tax reform, immigration, and regulatory stability, the administration has adopted a protectionist stance likely to depress business investment and cloud longer-term productivity trends.

The Federal Reserve is now in a difficult position—facing inflationary pressure from tariffs even as growth slows. While markets are still pricing in rate cuts, those expectations may need to be re-evaluated if headline and core inflation remain sticky through mid-year.

Emerging Markets and the Uneven Distribution of Pain

The global nature of the tariffs ensures that no region is spared, but emerging markets in Asia are disproportionately impacted. Countries like China, Vietnam, Thailand, and Indonesia face tariff rates exceeding 30%, threatening their export-led growth models and weakening investor sentiment across the region.

Policy space exists in many of these countries—fiscal buffers are available, and inflation is relatively tame—but stimulus measures may only partially offset the drag from reduced external demand. Complicating matters further, regional trade partners may consider imposing counter-tariffs on Chinese goods in a bid to remain competitive with U.S. markets, potentially fragmenting intra-Asian supply chains.

Canada: Relieved, But Not Unscathed

Amid the global dislocation, Canada finds itself in a rare position: not a direct target of this round of tariff escalation. Thanks to USMCA compliance and sectoral exemptions, most Canadian exports avoided new levies. The standout exception is autos, which now face an estimated 12.5% tariff, and ongoing 25% duties on steel and aluminum.

Still, the relative relief has mattered. The Canadian dollar rose modestly during a week of global equity and oil price weakness—an unusual occurrence that underscores the country’s favorable comparative position. While retaliatory measures were announced (including a 25% tariff on U.S.-built vehicles), these have thus far avoided escalation.

BMO Economics has held its already below-consensus 0.5% Canadian GDP growth forecast steady, citing the risk of spillovers from the broader downturn but also acknowledging that Canada’s resilience was stronger than expected. The housing market and employment data weakened into March, and sentiment remains fragile—but the lack of direct exposure to the harshest tariffs buys policymakers time and space.

Looking Ahead: Risks, Reversals, and the Return of Fundamentals

The next quarter will test investor discipline. Volatility will remain elevated. Economic data may deteriorate before it improves. Negotiations over tariffs will dominate headlines. Yet none of this invalidates the underlying drivers of long-term returns.

Productivity is rising. AI and digital infrastructure investment remains robust. Balance sheets are healthy. And policy responses—both monetary and fiscal—are more likely to accelerate than retreat.

While we cannot predict the precise path of geopolitics or trade negotiations, we remain confident in our disciplined process, well-diversified positioning, and long-term conviction.

As we’ve said many times: we do not make investment decisions based on headlines. We assess, rebalance, and navigate—never overreact.

Final Word: Endure the Noise, Trust the Process

Liberation Day is not just a trade policy—it is a turning point. Whether it marks the start of a sustained retreat from globalization or a temporary reset remains to be seen. What is clear is that uncertainty has risen, and capital markets have responded accordingly.

Our approach remains unchanged: assess risks rationally, respond deliberately, and focus on fundamentals. In markets as in life, response is everything.

We thank our clients for their continued trust and encourage all investors to stay the course, ask questions, and maintain perspective.

Debbie, Chris, Mark and Rosemary