March Market Newsletter: Market Conditions, Tariffs, and Political Uncertainty

Christopher Bowlby - Mar 31, 2025

The first quarter of 2025 has ushered in a period of heightened volatility across asset classes, driven by an increasingly complex global trade environment, shifting political landscapes, and signs of economic deceleration.

The first quarter of 2025 has ushered in a period of heightened volatility across asset classes, driven by an increasingly complex global trade environment, shifting political landscapes, and signs of economic deceleration. With the U.S. administration pressing forward with aggressive tariff policies, financial markets have responded by repricing risk, sending equity indices into correction territory, pushing bond yields lower, and forcing central banks into a more accommodative stance. At the same time, evolving market leadership is becoming apparent, requiring a nimble investment approach to navigate shifting sector dynamics.

Source: BMO Economics

Trade policy remains the dominant driver of economic sentiment. On March 3, President Trump imposed a 25% tariff on Canadian and Mexican goods, marking the official start of a North American trade war. Canada responded immediately with reciprocal tariffs on U.S. goods, while Mexico has opted to delay retaliation in hopes of keeping negotiations alive. On March 4, hints emerged that a compromise might still be possible, but markets remain on edge, reflecting the broader uncertainty that has defined recent months. While some degree of tariff escalation had been anticipated, the magnitude and scope of these measures have forced investors to reassess both short- and long-term economic expectations.

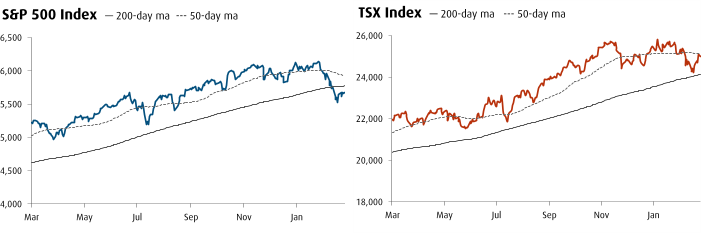

From an economic perspective, tariffs function as a regressive tax, disproportionately impacting consumers and businesses that rely on international supply chains. While targeted tariffs can sometimes be useful, broad-based protectionist policies tend to increase inflation, reduce economic growth, and weigh on business investment. The immediate response in capital markets reflects this reality. The S&P 500 and TSX Composite are down 8% and 4%, respectively, from their February peaks. Bond markets have moved sharply in response, with yields declining as investors shift from pricing in inflation risks to focusing on weaker growth prospects. The Canadian dollar remains under pressure, with expectations that it will weaken to C$1.49 (67 cents USD) by September, offering a cushion to exporters but compounding inflationary pressures for consumers.

Before these developments, the Canadian economy was gaining momentum on the back of lower interest rates, posting a 2.6% annualized GDP growth rate in Q4. However, with tariffs now a reality, GDP growth projections have been revised downward, with expectations that growth will slow from previous estimates above 1% to just 0.5% this year. The expected downturn could lead to more than 100,000 job losses and push the unemployment rate to 8.0% by year-end, a stark contrast from the labor market strength seen in the previous twelve months. In the United States, GDP growth expectations have been lowered to 1.8% from 2.8% last year, marking the weakest performance in five years. While the U.S. economy is less exposed to trade disruptions than Canada or Mexico, the combination of tariffs, government spending cuts, and a potential equity market correction poses risks to consumer spending and corporate earnings.

Recent data on U.S. retail sales underscores these risks. The headline number rose just 0.2% in February, below expectations, with discretionary categories showing particular weakness. However, the control group—a better indicator of core consumer demand—rebounded 1.0%, offsetting January’s decline. Personal savings also rose in January, offering households a temporary buffer. Nonetheless, weakening consumer confidence, particularly among lower-income groups, suggests this resilience may prove short-lived. Foot traffic is falling, and retailers like Dollar General have warned that shoppers are increasingly focused on essentials.

Industrial production has surprised to the upside, growing at a 5.9% annualized pace in Q1. Yet this strength may prove transitory, fueled by weather-related distortions and stockpiling ahead of tariff changes. More broadly, regional PMI indicators continue to fall, suggesting that manufacturers are bracing for rising input costs, supply-chain frictions, and waning demand. Investor and business sentiment has similarly deteriorated, with surveys showing multi-decade highs in pessimism and cash allocations rising rapidly—echoes of the early pandemic period.

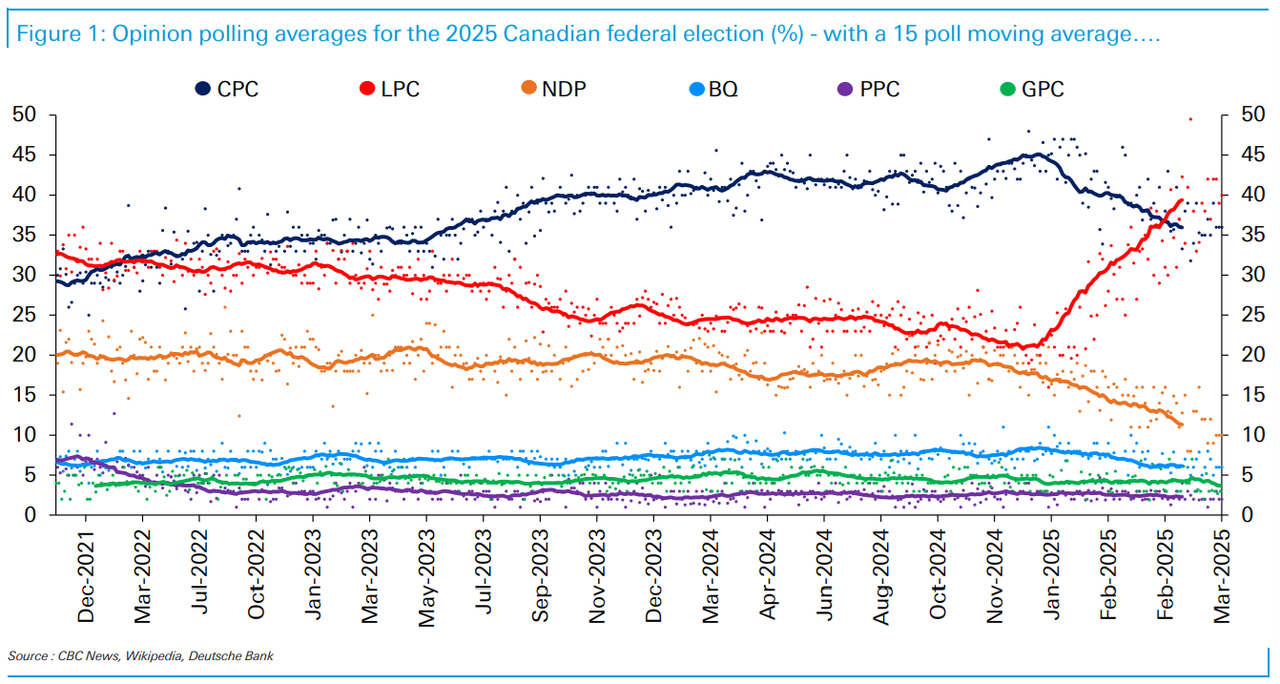

The tariff war is unfolding against a backdrop of shifting political dynamics. In Canada, newly elected Prime Minister Mark Carney—just nine days into his term—has called a federal election for April 28. The decision comes amid heightened national anxiety over U.S. trade aggression and controversial remarks by former President Trump suggesting Canada should become the “51st state.” These provocations, combined with punishing tariffs, have reshaped the political landscape. Nationalist sentiment has surged, breathing new life into Carney’s governing Liberal Party and narrowing what had been a significant Conservative lead.

Carney, a former governor of both the Bank of Canada and Bank of England, has positioned himself as a steady economic steward during a period of extraordinary external threats. He has quickly pivoted away from several Trudeau-era policies, including shelving the proposed capital gains tax increase and the consumer carbon tax, while simultaneously deepening economic ties with European allies. Meanwhile, Conservative leader Pierre Poilievre has sought to frame the election around affordability and governance, arguing that Canada’s vulnerability to U.S. pressure stems from Liberal mismanagement. Yet the rapidly shifting tone of the campaign has complicated his pitch, particularly in Quebec, where support for separatist movements is being replaced by a unifying nationalist response.

Should the election consolidate support behind Carney’s Liberals, markets may interpret this as a signal of continuity in fiscal policy but with a greater emphasis on global diversification and economic sovereignty. However, political uncertainty in the run-up to April 28 will remain a near-term overhang for Canadian equities and the loonie.

In the United States, trade policy is becoming increasingly unpredictable as the presidential election cycle intensifies. The March FOMC meeting saw the Fed hold its policy rate steady, but members lowered their growth forecasts and revised inflation projections higher. While the dot plot continues to show two cuts this year, the range of views has widened, and Chair Powell emphasized the unusually high degree of uncertainty. The risk of policy error is increasing—particularly if stagflationary pressures build, making it harder to separate transitory tariff effects from embedded inflation dynamics.

Outside of North America, retaliatory measures are escalating. The European Union has already imposed reciprocal tariffs, and China has signaled that it may begin targeting key U.S. exports if tensions persist. Meanwhile, European defense spending is ramping up in response to geopolitical tensions and concerns about U.S. reliability. Germany, Switzerland, and Canada are exploring deeper cooperation, with Prime Minister Carney advocating for a “coalition of the willing” to navigate the post-American order in trade and security policy.

The near-term market outlook hinges on several key factors. Tariff negotiations will be closely watched, particularly as the April 2 deadline for additional measures approaches. Central bank policy will also be critical, as both the Federal Reserve and Bank of Canada weigh the risks of further economic weakness against the persistence of inflationary pressures. Fiscal policy developments in the United States will determine whether economic stimulus or contraction defines the second half of the year. Corporate earnings, despite market weakness, have continued to surprise to the upside, particularly in the United States and Canada. Finally, technical indicators suggest that equities may be approaching a short-term rebound after recent declines, though the path forward remains volatile.

While the risks from tariffs and political uncertainty remain high, capital markets have historically adapted to periods of disruption. The coming months will test investor resilience, but they will also present opportunities for those prepared to pivot with changing market dynamics. We maintain a cautiously optimistic stance, balancing near-term risks with selective opportunities in defensive assets, quality cyclicals, and global equities. The evolving trade war, political landscape, and economic fundamentals will dictate market movements in the months ahead.

As always, we will continue to monitor developments closely and adjust our outlook accordingly.

Debbie, Chris, Mark and Rosemary

The Bank of Canada’s March Rate Decision: Balancing Easing with Inflationary Risks

Source: Bloomberg

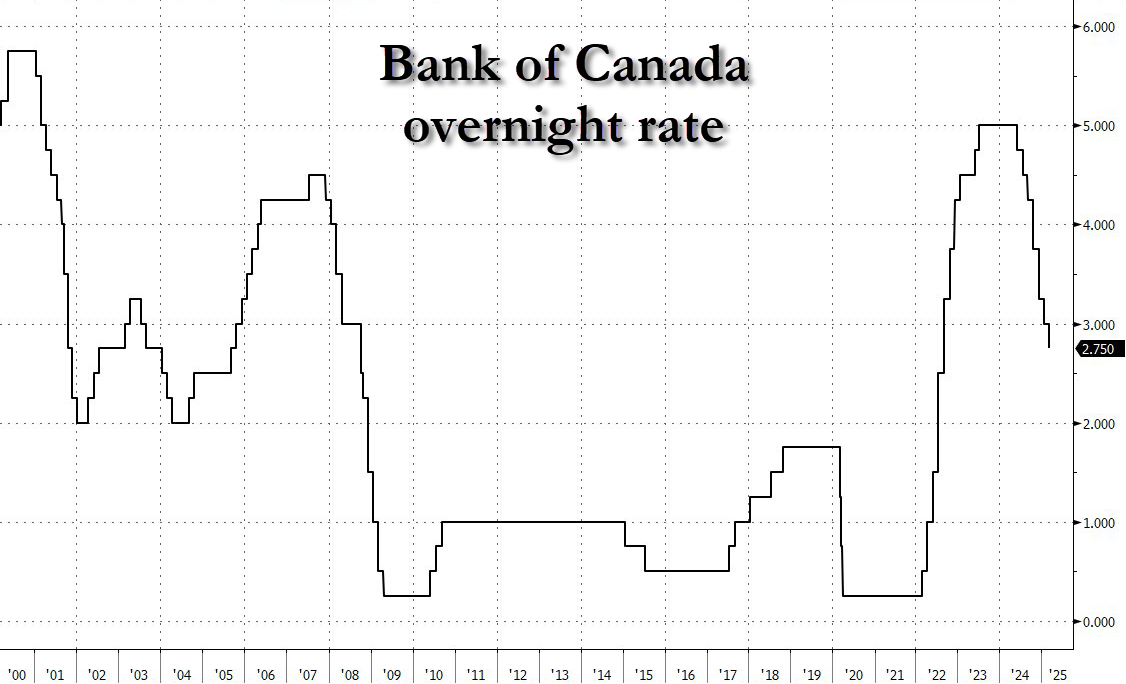

The Bank of Canada (BoC) delivered its seventh consecutive rate cut in March, reducing the policy rate by 25 basis points to 2.75 percent. This move was widely expected by markets and aligned with consensus forecasts, bringing the cumulative rate cuts to 225 basis points since the easing cycle began nine months ago. However, despite continuing to lower borrowing costs, the central bank’s statement reflected a shift in tone, signaling growing concerns over trade-related uncertainty, persistent inflationary pressures, and a deteriorating economic outlook.

While the BoC acknowledged that Canada’s economy ended 2024 on a stronger-than-expected footing, with robust GDP growth and employment gains, its assessment of early 2025 conditions was markedly less optimistic. The statement highlighted a sharp decline in consumer and business confidence, largely attributed to the uncertainty surrounding the evolving U.S.-Canada trade conflict. Businesses reported lower sales outlooks and investment plans, while consumers expressed heightened concerns about job security and financial well-being. The Governing Council underscored that while previous rate cuts had supported domestic demand, the emerging effects of tariff risks and financial market volatility could weaken the economy significantly in the months ahead.

The BoC’s statement also provided a nuanced discussion on inflation dynamics, acknowledging that while headline inflation was set to rise to around 2.5 percent in March due to the expiration of the GST/HST holiday, its broader concern was with core inflation persistence. Although core price measures had shown signs of moderation, shelter costs remained a major inflationary force, with mortgage interest costs still up nine percent year-over-year, though easing from previous double-digit increases. The statement further noted that short-term inflation expectations had increased due to tariff fears, yet policymakers remained more focused on medium- and long-term inflation trends, which they believe will ultimately determine the path of future rate decisions.

In discussing monetary policy implications, the BoC emphasized the limits of its ability to counteract the economic drag from trade disruptions. Governor Tiff Macklem stated unequivocally that “monetary policy cannot offset the impacts of a trade war,” reinforcing the notion that while interest rate adjustments could help cushion the economy, they could not prevent the structural damage that ongoing tariff escalations might inflict. The statement also highlighted that while the BoC remained open to further rate cuts, any additional easing would be contingent on how inflationary pressures evolve relative to weakening demand. The Governing Council noted that it would closely monitor how firms pass through higher costs to consumers and assess whether price pressures begin to feed into broader inflation expectations.

The labour market outlook also played a key role in the BoC’s assessment. Although the unemployment rate declined to 6.6 percent in early 2025, the central bank pointed to slowing job growth in February and warned that the combination of rising tariffs, a weaker currency, and tighter credit conditions could lead to labour market disruptions in the coming quarters. Wage pressures, which had been a persistent concern for policymakers in 2024, were now showing clearer signs of moderation, and the BoC removed references to wage growth being “sticky.” Instead, the statement characterized wage growth as softening, suggesting that labour market conditions may start to exert disinflationary pressures.

A crucial factor complicating the BoC’s decision-making process is the timing and extent of the impact from U.S.-Canada trade tensions. While exports had temporarily surged in early 2025 as businesses front-loaded shipments to avoid impending tariffs, policymakers warned that this dynamic would likely lead to an even sharper decline in economic activity later in the year. The BoC acknowledged that businesses were becoming increasingly cautious in their hiring and investment decisions, which could slow overall growth momentum. In addition, the recent depreciation of the Canadian dollar against the U.S. dollar has raised the cost of imported goods, further amplifying inflation risks at a time when demand is already softening.

While markets had previously anticipated two more 25-basis-point rate cuts by mid-2025, bringing the terminal rate to 2.25 percent, the BoC’s more measured tone in its March statement led to a slight recalibration of expectations. Investors initially reacted to the rate cut with a decline in Canadian bond yields, but as the less dovish guidance became clearer, yields steepened later in the session, reflecting reduced conviction in the likelihood of aggressive further easing. The Canadian dollar initially weakened on the rate cut but stabilized as markets digested the BoC’s more cautious stance.

Looking ahead, several critical factors will shape the trajectory of the BoC’s monetary policy. The April inflation report is expected to show a temporary downward adjustment in headline CPI due to the expiration of the carbon tax holiday, but core inflation trends—especially in shelter and services—will be closely scrutinized. Trade policy developments remain the most significant source of uncertainty, as any escalation in U.S.-Canada tariff disputes could materially alter the BoC’s outlook. Additionally, the labour market’s trajectory will be crucial, as further signs of employment softening could provide a rationale for additional rate cuts. The Federal Reserve’s stance will also influence the BoC’s decision-making, particularly if U.S. monetary policy diverges significantly from Canada’s, affecting capital flows and exchange rate dynamics.

In conclusion, the Bank of Canada remains on an easing trajectory, but policymakers are becoming increasingly cautious about the scope and timing of further rate reductions. While the central bank continues to balance the risks of a slowing economy against persistent inflationary pressures, it has made it clear that monetary policy alone cannot counteract the effects of a trade war. The coming months will be critical in determining whether the BoC proceeds with additional easing or adopts a more extended pause, waiting for further clarity on inflation trends and trade developments before committing to another policy move. As uncertainty remains high, investors, businesses, and policymakers alike must remain vigilant in monitoring economic conditions, as shifting inflation expectations, labour market dynamics, and global trade developments could all play a decisive role in shaping Canada’s economic landscape for the remainder of the year.

Canadian CPI Surges Amid Tax Reversal and Persistent Core Inflation Pressures

Canadian inflation trends took a sharp turn upward in February, with consumer prices rising 1.1 percent month-over-month (0.7 percent seasonally adjusted), marking the most significant monthly increase in nearly a year. On an annual basis, headline inflation climbed to 2.6 percent, a notable acceleration from January’s 1.9 percent. The primary driver behind this inflationary spike was the mid-month expiration of the GST/HST holiday, which had previously provided temporary relief to consumer prices. However, while the tax reversal played a major role in lifting inflation, the underlying data suggest that price pressures remain broad-based and more persistent than previously anticipated.

Even after adjusting for the direct impact of the tax change, seasonally adjusted inflation remained firm at 0.4 percent on the month, with price gains extending across multiple categories. Excluding food, energy, and taxes, core CPI still advanced by 0.3 percent, underscoring that inflationary pressures cannot be attributed solely to transitory tax distortions. Recreation prices surged by 3.4 percent, food costs rose 1.9 percent, clothing prices increased 1.6 percent, and alcohol climbed 1.5 percent, with these categories seeing the largest price jumps due to the tax reversal. However, the breadth of inflationary pressures went beyond tax-sensitive components, suggesting that underlying price stickiness remains a challenge for policymakers.

The Bank of Canada’s core inflation measures, CPI-Trim and CPI-Median, both advanced 0.3 percent month-over-month, bringing their annual rates to 2.9 percent. This reading was hotter than expected, and the shorter-term inflation momentum remains a concern. The three-month and six-month annualized rates for core inflation continue to run above 3 percent, reinforcing the notion that underlying inflation pressures are not yet fully contained. Additionally, the share of consumer basket items rising above 3 percent increased modestly, indicating that inflation breadth is worsening rather than improving. Given the BoC’s focus on inflation persistence, these indicators will be critical in shaping its future rate decisions.

The implications of the February inflation report extend beyond the immediate spike in headline CPI, as it presents a complex picture for policymakers at a time of heightened trade and economic uncertainty. While the expiration of the GST/HST holiday was expected to drive a temporary rise in inflation, the continued strength in core measures suggests that price pressures may prove more persistent than the central bank had initially anticipated. This presents a dilemma for the BoC, which has been gradually easing monetary policy in response to weakening economic momentum but remains concerned about the risk of entrenched inflation.

The outlook for inflation remains highly uncertain, as conflicting forces are set to influence price dynamics in the coming months. The weaker Canadian dollar, which has depreciated amid global trade tensions, is likely to raise the cost of imported goods, adding upward pressure to inflation at a time when domestic demand is already softening. Rising economic uncertainty, coupled with a weakening labour market and deteriorating consumer sentiment, may dampen household consumption, which in turn could exert a cooling effect on inflation.

Looking ahead, several critical factors will shape the trajectory of inflation and monetary policy. April’s CPI report will be particularly important, as it will provide clarity on how inflation trends evolve following the end of the carbon tax holiday. If core inflation remains elevated, it could force the BoC to pause its rate-cutting cycle, waiting for clearer signs of disinflation before proceeding with further easing. Additionally, the direction of U.S.-Canada trade policy will play a significant role in determining inflation risks, as any escalation in tariffs could lead to additional cost pressures on Canadian businesses and consumers.

For the Bank of Canada, the path forward remains fraught with uncertainty. While the central bank has prioritized supporting economic growth through rate cuts, the persistence of core inflation presents a significant challenge. If inflation proves more entrenched than expected, policymakers may need to reassess the pace and magnitude of further easing. At the same time, a rapid deterioration in economic conditions or an escalation in trade tensions could tilt the balance toward additional rate cuts, despite lingering inflation concerns.

In conclusion, the February inflation report underscores the challenges facing the BoC as it navigates a highly uncertain macroeconomic environment. While the expiration of the GST/HST holiday temporarily distorted inflation figures, the underlying trend of persistent core inflation suggests that price pressures remain more resilient than anticipated. With conflicting forces at play—ranging from weakening demand to inflationary trade disruptions—the BoC will need to closely monitor economic developments before making its next policy move. For investors, businesses, and policymakers alike, the coming months will be pivotal in determining whether inflationary pressures subside or if persistent price stickiness forces the BoC to take a more cautious approach in its monetary easing strategy.

March FOMC Meeting and Updated Summary of Economic Projections

Source: Bloomberg

The Federal Open Market Committee (FOMC) concluded its March meeting by maintaining the federal funds rate at 4.25%-4.50%, a widely expected decision. However, the meeting delivered critical insights into the Federal Reserve’s evolving policy stance, reflecting an increasingly complex economic landscape characterized by slowing growth, persistent inflation, and heightened uncertainty. The Fed’s updated Summary of Economic Projections (SEP) reinforced this dynamic, showing downward revisions to economic growth, upward revisions to inflation forecasts, and a more cautious policy outlook moving forward.

The FOMC statement contained a notable shift in tone, removing prior language that suggested risks to employment and inflation were "roughly in balance." Instead, the statement emphasized that uncertainty surrounding the economic outlook had increased. Chair Powell, in his post-meeting press conference, downplayed the significance of this change, stating that it was not intended to send a policy signal. Nevertheless, this shift in communication underscores the Fed’s growing concerns about the economic trajectory and highlights the challenge of navigating between the dual risks of inflation and slowing growth.

The updated economic projections reflected a worsening trade-off between inflation and economic activity. GDP growth projections were revised downward, with the Fed now expecting the economy to expand by only 1.7% in 2025, a notable decline from the previous forecast of 2.1%. Growth in 2026 was also downgraded to 1.8% from 2.0%. This downward revision suggests that the economy is losing momentum, a concern reinforced by the fact that 16 out of 19 FOMC participants now see downside risks to growth. The labor market, while still robust, is expected to weaken slightly, with the unemployment rate forecasted to rise to 4.4% in 2025, compared to the previous estimate of 4.3%. A growing number of FOMC members—17 out of 19—now see the risks to labor market projections skewed to the upside, signaling that concerns about employment deterioration are increasing.

Despite these indications of weaker growth, inflation forecasts were revised higher. Core PCE inflation, the Fed’s preferred measure of underlying price pressures, is now expected to reach 2.8% in 2025, up from the previous estimate of 2.5%. Headline PCE inflation is projected to come in at 2.7% for 2025, reflecting the impact of supply chain constraints and rising costs associated with tariffs. While the Fed maintains its long-term projection of inflation returning to 2.0% by 2027, the majority of policymakers now view inflation risks as skewed to the upside, implying greater caution in implementing policy easing.

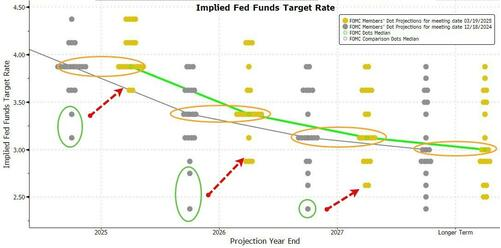

Despite these economic headwinds, the median policy rate projections in the Fed’s dot plot remain unchanged, indicating two rate cuts in 2025. The median forecast for the federal funds rate at the end of 2025 stands at 3.9%, implying two 25-basis-point rate cuts this year, followed by additional easing in 2026 and 2027, bringing rates down to 3.0% over the long run. However, the dispersion of rate projections has shifted in a more hawkish direction. The average 2025 dot increased to 4.0%, up from 3.8% in December, suggesting that a growing number of policymakers are leaning toward fewer rate cuts this year. Eight members now expect just one or no cuts in 2025, while only two participants anticipate three cuts. This shift highlights the Fed’s hesitancy to ease policy too soon, particularly in the face of persistent inflationary pressures.

One of the more surprising developments from the meeting was the Fed’s decision to significantly slow the pace of balance sheet reduction, known as quantitative tightening (QT). Starting in April, the central bank will reduce its monthly Treasury security runoff from $25 billion to $5 billion while maintaining the existing $35 billion cap on mortgage-backed securities runoff. This decision, which Fed Governor Christopher Waller dissented against, marks a notable shift in the Fed’s approach to managing financial conditions. Powell emphasized that this move does not signal a change in monetary policy but rather reflects the Fed’s preference to gradually approach an ample level of reserves. The QT slowdown suggests that policymakers are becoming more concerned about liquidity conditions and financial stability risks, particularly given the ongoing debt ceiling uncertainties.

During his press conference, Powell reinforced the Fed’s commitment to maintaining policy flexibility. He stated that the current stance is well-positioned to address economic uncertainties, adding that the central bank will adjust its policy as needed based on evolving economic conditions. If inflation remains stubbornly high, the Fed can keep rates elevated for an extended period. Conversely, if the labor market deteriorates more than anticipated, the Fed has room to ease policy in response. Powell also addressed concerns about tariffs and their impact on inflation, reiterating that while tariff-induced price pressures could delay disinflationary progress, the Fed’s baseline assumption is that these effects will be transitory.

Markets responded positively to the FOMC decision, interpreting the combination of QT tapering and retained rate-cut expectations as a mildly dovish signal. The S&P 500 gained 1.3% on the day, marking its strongest post-Fed rally since 2022. Treasury yields fell, with two-year yields dropping six basis points, reflecting a slight easing of rate-cut expectations. While equity markets welcomed the QT adjustment as a sign that the Fed remains attentive to liquidity conditions, the overall policy stance remains mixed. The Fed’s statement was hawkish, acknowledging higher inflation risks and weaker growth, while the economic projections reflected a stagflationary environment. The dot plot signaled a more hawkish shift in policymaker sentiment, yet the balance sheet decision introduced an element of dovishness, suggesting that the Fed is carefully managing financial conditions.

The March FOMC meeting reinforced that the Federal Reserve is navigating a highly uncertain economic environment. On one hand, slowing growth and rising uncertainty argue for a more accommodative stance. On the other, persistent inflation and resilient labor markets suggest that restrictive policy may need to remain in place for longer than previously expected. This dynamic raises key risks for markets. If the Fed underestimates inflation persistence, it may need to maintain rates at higher levels for an extended period, delaying the anticipated rate cuts. Conversely, if growth deteriorates more sharply than expected, the Fed may be forced to pivot toward more aggressive easing.

For investors, this environment underscores the importance of maintaining flexibility in portfolio positioning. Fixed-income markets may remain volatile as rate-cut expectations continue to evolve, making duration positioning crucial. Equities may face headwinds in cyclical sectors, while defensive and quality-growth stocks could outperform in an environment of elevated uncertainty. Real assets, commodities, and inflation-sensitive investments remain relevant as hedges against ongoing price pressures.

Looking ahead, the next key catalyst will be the upcoming tariff announcements expected in April. Additional trade policy changes could further complicate the Fed’s efforts to balance growth and inflation risks. With monetary policy uncertainty still elevated, market participants should prepare for continued volatility as the Fed assesses the evolving economic landscape.

U.S. CPI Report: A Softer Inflation Print Eases Market Concerns

Source: Bloomberg

The latest Consumer Price Index (CPI) report provided a welcome sign of easing inflationary pressures, breaking a three-month streak of acceleration. Headline CPI rose by 0.2% in February, a notable slowdown from January’s 0.5% increase. On a year-over-year basis, inflation moderated to 2.8%, down from 3.0% the previous month and coming in below the consensus expectation of 2.9%. The report signals some relief for markets, as consumer price growth showed signs of cooling across several key categories, particularly in shelter, energy, and discretionary spending. However, while this deceleration may calm fears of a reacceleration, inflation remains above target, and the Federal Reserve will likely seek further confirmation before altering its policy stance.

A significant contributor to February’s inflation reading was the shelter index, which increased by 0.3% and accounted for nearly half of the total rise in CPI. Although still elevated, this represented a more measured increase compared to recent months. Rent and owners’ equivalent rent (OER) both decelerated to 0.28% in February, marking the slowest pace since late 2021. On an annual basis, shelter costs remain up 4.2%, underscoring the ongoing challenges in housing affordability, though the data suggests a gradual normalization. Energy prices remained relatively subdued, rising only 0.2% overall, as a 1.0% decline in gasoline prices helped offset notable increases in electricity and natural gas, which climbed 1.0% and 2.5%, respectively.

The transportation and travel sectors also played a role in February’s moderation, with airline fares dropping sharply by 4.0%, a welcome reversal from previous gains. New vehicle prices dipped slightly, falling 0.1%, while used vehicle prices rebounded with a 0.9% increase. The decline in airfare, coupled with easing auto prices, contributed to a more favorable inflation print, particularly for discretionary consumer spending categories. Food inflation remained contained, rising 0.2% for the month, with food at home unchanged and food away from home continuing to climb at a steady 0.4%.

Core CPI, which excludes food and energy, also registered a softer reading, increasing by 0.2% in February after a stronger 0.4% rise in January. The year-over-year rate moderated to 3.1%, down from 3.3% previously. While this suggests some progress, core inflation remains well above the Federal Reserve’s 2.0% target. Notably, core services inflation, excluding housing, continued to run hot at an annualized three-month pace of 4.8%, though this was an improvement from January’s 5.3%. Other service-based components, such as medical care, recreation, and apparel, saw price increases of 0.3%, 0.3%, and 0.6%, respectively.

The softer CPI report has shifted market expectations toward a more dovish outlook for monetary policy. Based on the details of the report, Goldman Sachs now estimates that core Personal Consumption Expenditures (PCE) inflation, the Fed’s preferred gauge, rose by 0.29% in February, translating to a year-over-year rate of 2.7%. This projection suggests that inflationary pressures, while persistent, may be moderating enough to justify policy adjustments later in the year. Market pricing has increasingly reflected expectations of three quarter-point rate cuts by the end of 2025, with the first likely to occur as soon as June.

While February’s inflation data is encouraging, it does not yet mark a decisive turning point. The Federal Reserve remains cautious, as certain categories, particularly core services, continue to exhibit inflationary persistence. A premature policy shift could risk reaccelerating inflation, especially if wage growth remains firm or energy prices reverse course. Policymakers will require further confirmation that inflation is on a sustained downward trajectory before considering rate cuts.

For investors, this report strengthens the case for a soft-landing scenario in which inflation gradually moderates without severely disrupting economic growth. If this trend continues, risk assets could benefit, while long-duration bonds may see renewed demand as rate-cut expectations solidify. The upcoming release of the February PCE report will be crucial in determining whether this disinflationary momentum persists and how the Fed may respond in the coming months.