December 2024 Market Newsletter: 2025 Market Outlook

Christopher Bowlby - Dec 30, 2024

As we enter 2025, the markets are poised for a year of balanced growth, driven by monetary easing, stabilizing inflation, and shifting market leadership.

Since the U.S. election, we have seen financial markets push to levels of exuberance and euphoria, driven by dreams of lower interest rates, decreased regulations, and an improved deal-making environment for 2025 once President Trump takes office. For 2024, the Santa Claus rally came early. However, since American Thanksgiving, we have seen the euphoria wear off as equities pulled back, with the Dow recording a 10-day decline—a streak not seen since 1974. Earlier this week, the Federal Reserve provided an expected interest rate cut of 25 basis points (bps) at its final meeting of 2024, culminating in a total of 1% in monetary policy easing for the year.

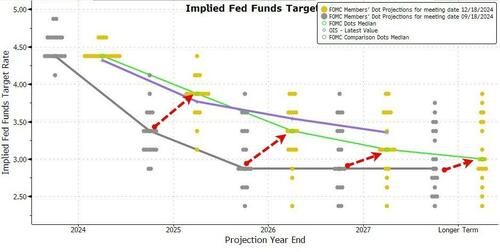

The main highlight of the meeting was not the rate cut but rather the updated Summary of Economic Projections, which indicated that the Federal Reserve is entering a new phase of the normalization process with a more cautious outlook on rate cuts in the coming year and a higher terminal rate anticipated in 2027.

While equity markets sold off dramatically and the U.S. dollar rose to multi-year highs as participants repriced monetary policy expectations, we were not surprised by the FOMC’s continued mantra of being data-dependent, especially in light of recent economic data. U.S. GDP continues to grow at a 3% pace, while core CPI remains stubbornly high, with recent figures showing slight month-over-month increases over the past five months. Additionally, the threat of tariffs and increased uncertainty on the fiscal policy front—with the collapse of the spending agreement, the possibility of a government shutdown, and the debt ceiling looming once again—have added to the market's volatility.

Looking forward to 2025, we expect that we will continue to see a generally positive outlook for equities. While the Trump rhetoric post-election day has largely been welcomed by financial markets, the realities of governing will begin to emerge once he takes office on January 20th. Many promises, such as reduced taxes, are unlikely to materialize until late 2025 or even 2026, whereas the impact of tariffs and increased protectionism may add inflationary pressure to CPI much sooner.

Adding to this, market leadership is anticipated to shift as 2025 progresses, requiring investors to remain nimble. Quality cyclicals, supported by rate cuts and stabilizing macro indicators, are expected to outperform as the equity market broadens beyond its recent concentration in technology-driven sectors. As equity markets diversify, opportunities are expected to emerge across a wider range of industries, reducing the dominance of the "Magnificent 7" stocks seen in recent years. Rate cuts and stabilizing inflation are likely to contribute to this more inclusive market environment.

The U.S. economy enters 2025 with strong momentum, bolstered by several unique growth drivers. A key factor is the structural impact of the ongoing AI revolution, which is driving significant corporate and research spending. Investments in AI infrastructure—including data centers, semiconductors, and energy generation—are creating economic tailwinds not seen in other developed economies. At the same time, U.S. consumers remain a key pillar of economic strength. Robust household balance sheets, coupled with steady wage growth, have allowed consumer spending to remain resilient despite higher borrowing costs. Additionally, corporate sentiment is expected to rise following the Trump administration's renewed focus on deregulation, supporting earnings growth and a more balanced equity market.

The Canadian economy and the TSX are not without drama. The Trudeau government is in turmoil following the resignation of Deputy Prime Minister Chrystia Freeland on the day of the Fall Economic Statement. Canadian GDP is sputtering, and the looming threat of tariffs on January 20th could cripple the already limping economy. This has been reflected in the performance of the Canadian dollar, which has fallen below 70 cents for the third time in 20 years after holding steady for the first ten months of 2024. This decline reflects both Canadian economic weakness and U.S. dollar strength. The combination of 175 bps of rate cuts by the Bank of Canada, paired with the threat of disrupted trade and stubborn inflation south of the border, has led to further dislocation in monetary policy. Finally, with the NDP signaling they will vote to bring down the government, an early 2025 election seems imminent.

Furthermore, we expect that despite the challenges facing the Canadian economy, we will see above-consensus growth in Canada next year. As one of the most interest-sensitive economies globally, Canada is only now beginning to see the effects of aggressive monetary easing by the Bank of Canada. Additionally, policymakers in Ottawa recognize the importance of preserving the Canada-U.S. trade relationship and will likely work to address President Trump’s concerns to mitigate the risk of 25% tariffs. (Earlier this week, Trudeau announced a $1.3 billion plan to enhance surveillance and create a joint "strike force" targeting transnational organized crime.)

Despite this strong outlook, several risks could weigh on growth. Potentially inflationary policies, geopolitical uncertainties, and rising federal deficits could complicate the Federal Reserve’s path forward and create additional challenges as 2025 progresses. In particular, the elevated forward P/E multiples in equity markets, coupled with tariff and fiscal consolidation risks, could temper investor optimism. While deregulation and pro-growth policies may offer support, the potential for valuation compression remains, particularly if fiscal tightening impacts economic expansion more than anticipated.

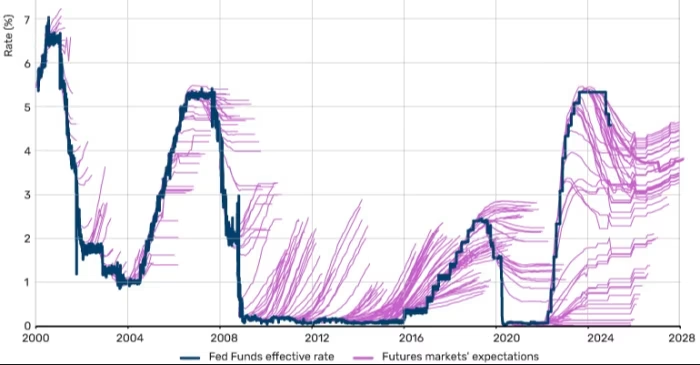

Overall, we would like to leave you with this chart from the Financial Times, which highlights the challenge of making predictions, particularly about the future of something as complex as the economy.

Source: Financial Times

We wish you a very happy holiday season and look forward to speaking with you in the new year.

Chris, Debbie, Mark and Rosemary

Bank of Canada

The Bank of Canada announced a 50 bps cut to its overnight lending rate at its December meeting, reducing it to 3.25%. This marks the fifth consecutive reduction, with a cumulative decrease of 175 bps since June, positioning the Bank of Canada as the most aggressive among G10 central banks. Governor Macklem stated that while the Bank has been aggressive in 2024, it will adopt a more gradual approach going forward as it moves toward a neutral stance. The Bank reiterated that it will remain data-dependent, and barring unexpected behavior from CPI and GDP, we anticipate a more measured path of rate cuts in 2025.

Federal Reserve

At its December meeting, the FOMC reduced the Fed Funds rate by 25 bps to a target range of 4.25–4.50%. This decision was widely anticipated following the previous week’s CPI report, which showed persistent inflationary pressures across both headline and core inflation gauges.

Source: Bloomberg

The biggest surprise was the updated Summary of Economic Projections, which showed a slower anticipated pace of rate reductions in 2025. This reflects the Fed’s heightened sensitivity to structural and inflationary dynamics within the economy. Additionally, the longer-run neutral rate projection was revised upward to 3.00% from 2.875%. Core PCE inflation is expected to remain above the 2% target until 2027, underscoring the entrenched nature of price pressures.

2025 Outlook

Looking ahead to 2025, we expect a return to a more normalized environment with balanced performance across equity markets. While 2023 and 2024 delivered significant gains driven by the "Magnificent 7" stocks, 2025 is likely to be characterized by monetary easing, stabilizing inflation, and a strong labor market, providing a solid base for stock fundamentals. We anticipate high single-digit to low double-digit performance with stable price-to-earnings multiples, supported by earnings growth and improved market breadth.

The current secular bull market for U.S. stocks, which began in 2009, remains intact, underscoring the market's resilience through multiple cyclical bear phases. Gains in 2025 are expected to reflect a healthier balance across sectors, with market leadership anticipated to rotate throughout the year. This rotation will likely favor quality cyclicals, which stand to benefit from stabilizing macro indicators, rebounding capital market activity, and easing monetary policy. Following two years of outsized returns concentrated in mega-cap technology stocks, 2025 is poised to deliver more evenly distributed performance across a broader range of sectors, requiring a nimble investment approach.

The U.S. economy is set to remain the global growth engine in 2025, even as global GDP slows to an estimated 3%. Monetary policy is expected to continue easing, albeit at a more gradual pace, offering sustained support for corporate profitability and consumer spending. Earnings growth in the S&P 500 is forecast to accelerate, driven by mid-single-digit revenue growth and margin expansion, resulting in an estimated 13% EPS growth. This broad-based earnings recovery signals a shift toward healthier equity market dynamics, with improved contributions from sectors outside of technology.

Investor sentiment has strengthened post-election, buoyed by a focus on pro-growth policies such as deregulation and fiscal discipline. While valuation levels remain elevated, they are expected to stabilize due to robust earnings growth and the supportive monetary policy environment, with only modest P/E compression anticipated. At the same time, risks associated with fiscal consolidation and elevated term premiums must be carefully managed to sustain market optimism.

However, several headwinds could temper the pace of growth in 2025. Proposed tariffs, fiscal consolidation efforts, and geopolitical challenges introduce potential volatility and uncertainty. While deregulation and productivity enhancements may unlock growth opportunities, they also highlight vulnerabilities in fiscal sustainability and global trade dynamics. Trade policies aimed at protecting domestic industries could exert inflationary pressures, complicating the Federal Reserve's path forward.

Overall, we maintain a cautiously optimistic outlook for 2025. The anticipated broadening of market leadership, improved earnings trajectory, and continued monetary easing create a supportive environment for equity investors. However, the complexity of fiscal and trade policy shifts will require a disciplined and adaptable investment strategy to navigate the evolving landscape effectively.