December FOMC Meeting Deliver A Hawkisk Rate Cut

Christopher Bowlby - Dec 19, 2024

The Federal Reserve concluded their December FOMC meeting and reduced the Fed Funds rate by 25 bps while signaling a dramatically less aggressive rate-cut cycle.

Yesterday, the Federal Reserve concluded their December FOMC meeting and reduced the Fed Funds rate by 25 bps to a target range of 4.25 - 4.50%. This decision was widely anticipated by the markets, especially following the previous weeks CPI report which showed persistent inflation pressures across both headline and core inflation gauges.

Source: Bloomberg

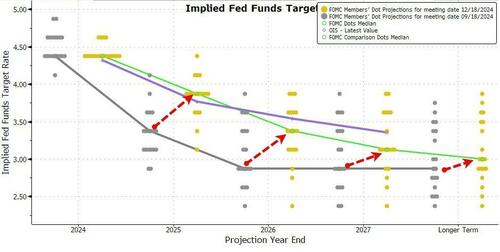

The big surprise of the meeting was the updated Summary of Economic Projections which showed a slower anticipated pace of rate reductions in 2025, reflecting the Fed’s heightened sensitivity to the structural and inflationary dynamics within the economy and the longer-run neutral rate projection was revised upward to 3.00% from 2.875%. Additionally, core PCE inflation is expected to remain above the 2% target until 2027, further showing the stubbornness of entrenched price pressures.

Revised Economic Projections

The updated SEP provided further granularity into the Federal Reserve’s economic outlook for the medium term:

- GDP Growth: The projection for real GDP growth in 2024 was raised to 2.5%, reflecting continued economic resilience and robust activity across sectors.

- Unemployment Rate: The unemployment forecast for 2024 was revised down to 4.2%, with stabilization expected at 4.3% through 2027.

- Inflation Forecasts: Both core and headline PCE inflation projections were adjusted upward, reflecting the persistence of inflationary pressures despite tightening monetary conditions.

Of particular note, the longer-term neutral rate continued its upward trend, reaching 3.00%. This signals an acknowledgment of the economy’s capacity to operate with structurally higher rates, a development that shapes expectations for the Fed’s terminal rate in this cycle.

Source: Bloomberg

Chair Powell’s Guidance

Chair Jerome Powell’s post-meeting remarks offered additional clarity on the Fed’s evolving strategy:

- Policy Near Neutral: “We are significantly closer to neutral, but policy remains meaningfully restrictive.”

- Inflation Challenges: “The slower pace of cuts for next year reflects both the higher inflation readings this year and the expectation inflation will be higher.”

- Data-Driven Adjustments: “Actual cuts will depend on incoming data. Today’s SEP is just the general sense of what the Committee thinks is likely to be appropriate.”

These statements underline the Federal Reserve’s resolve to maintain optionality in its policy decisions, ensuring alignment with its dual mandate objectives.

Market Reaction

Financial markets responded swiftly to the Fed’s cautious tone:

- Currency Markets: The U.S. dollar strengthened to its highest level since November 2022.

- Equities: Equity markets sold off with the worst days since July as markets repriced expectations for rate cuts in 2025 and the terminal rate in 2027.

- Treasury Yields: Mid-curve maturities experienced the sharpest movements, with the 5-year yield rising 16 bps post-announcement. The 2s10s yield curve remained relatively unchanged, while the 5s30s spread flattened.

Conclusion

The December FOMC meeting underscored a hawkish shift in the Federal Reserve’s approach to monetary easing. By revising its economic projections and reducing the trajectory for rate cuts, the FOMC reaffirmed its data dependency and pushed CPI back to the forefront. Chair Powell continues to try and avoid re-hiking rates to combat a second spike in inflation reminiscent of the Arthur Burn's Fed in the 1970s.

With President Trump taking office in a month's time, the threat of tariffs adding fuel to persistent inflation definitely was a factor in this hawkish pivot and more conservative outlook for the FOMC.

While Chair Powell indicated that he remains confident that they will reach their goals of their dual mandate, there is more uncertainty in the base case. We expect that Chair Powell is potentially setting the table for a pause either in January or the the March meeting, depending on the path of inflation over the holidays.