Potential Impacts of Proposed U.S. Tariffs on Canadian and Mexican Imports

Christopher Bowlby - Nov 26, 2024

President-elect Donald Trump’s proposed 25% tariff on Canadian and Mexican imports has sent shockwaves through markets, threatening to disrupt trade, weaken the Canadian dollar, and impact key industries like energy, manufacturing, and autos.

On November 25, 2024, U.S. President-elect Donald Trump announced plans to impose a sweeping 25% tariff on all imports from Canada and Mexico, set to take effect in January 2025.

The rationale behind these tariffs is tied to U.S. concerns over illegal immigration and drug trafficking, particularly fentanyl, across its borders.

While this announcement may be a negotiating tactic to prompt policy changes in Canada and Mexico, it has sent shock waves through markets due to the significant economic and trade implications.

Economic Context and Trade Vulnerabilities

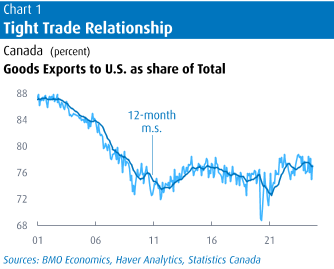

Canada’s economic reliance on trade with the U.S. underscores its vulnerability to these proposed measures:

- The U.S. accounts for approximately 75% of Canadian goods exports, which in turn represent 25% of Canada’s GDP.

- Energy exports alone contribute nearly a third (C$173 billion annually) of Canadian goods exports to the U.S., followed by manufacturing, industrials, and autos.

- Provincial exposure varies significantly. Ontario is particularly reliant on U.S. trade, with over 80% of its exports destined for the U.S., while Alberta is heavily dependent on oil exports. By contrast, British Columbia has less direct exposure, with a substantial portion of its exports going to non-U.S. markets.

If implemented, these tariffs would disrupt the integrated supply chains that have been central to North American trade under the United States–Mexico–Canada Agreement (USMCA). Sectors like automotive manufacturing, where components cross borders multiple times, would be particularly impacted, increasing costs and reducing efficiency.

Immediate Market Impacts

- Currency Depreciation

The Canadian dollar (CAD) is expected to weaken further, extending its recent decline past $1.41/USD. Currency adjustments typically offset part of the impact of tariffs, but further depreciation would raise import costs and fuel inflation in Canada. - Consumer Prices

In the U.S., tariffs on Canadian and Mexican goods could raise prices on essential imports, adding to existing inflationary pressures. Energy tariffs, for example, would likely result in higher oil and gas prices for American consumers.

Economic Growth Implications

- Canadian GDP Growth

The tariffs would have a net negative impact on Canadian growth, partially offsetting the current upward trajectory supported by robust domestic demand in housing and consumer spending.

BMO Economics projects a downward revision to Canada’s 2025 real GDP growth, currently forecasted at 2.1%. The impact would be more pronounced in the latter half of 2025 and into 2026. - Provincial Disparities

Ontario, with its significant exposure to autos and manufacturing, would face substantial risks. Alberta’s oil-dependent economy would also be affected, though immediate alternatives to Canadian oil for the U.S. market are limited.

Sector-Specific Impacts

- Energy

Tariffs on energy would be disruptive but less likely, given the U.S.’s reliance on Canadian oil imports (over 3 million barrels per day). Imposing tariffs on energy would also lead to higher consumer fuel prices in the U.S. - Manufacturing and Industrials

Exporters in these sectors would face margin compression, as Canadian firms would absorb part of the tariff costs to remain competitive. - Automotive

The highly integrated North American auto industry would face severe disruption, as components and finished products cross borders multiple times. This could lead to industry pushback in the U.S., potentially watering down the scope of tariffs.

Policy and Monetary Responses

- Bank of Canada

A weaker growth profile could prompt the Bank of Canada (BoC) to maintain a dovish policy stance, with rates potentially falling to 2.5% by September 2025, aligning with current projections.

However, the inflationary pressures from currency depreciation and potential supply shocks could limit the BoC’s ability to cut rates aggressively. - Trade Policy and Retaliation

Canada could respond with retaliatory tariffs targeting politically sensitive U.S. sectors, escalating the trade conflict and compounding economic risks for both nations.

Broader Economic and Business Implications

- Investment and Business Confidence

The uncertainty surrounding these proposed tariffs is likely to weigh on business confidence and investment, particularly in sectors tied to U.S. trade. This could exacerbate Canada’s existing challenges with productivity-enhancing investment.

With trade uncertainty, the burden of economic expansion may shift toward housing and consumer spending, creating an imbalance and exposing the economy to interest rate volatility. - U.S. Economy

The U.S. economy would not be immune to the effects of tariffs. Higher input costs for industries reliant on Canadian and Mexican imports, such as manufacturing and energy, could reduce profitability and competitiveness. Consumers would face higher prices, particularly for goods like autos, energy, and consumer products.

Conclusion

While the proposed tariffs may be a negotiating tactic, their potential implementation underscores the deep economic interdependence between Canada, Mexico, and the United States.

For Canada, the immediate risks include currency depreciation, sectoral disruptions, and downward pressure on growth. Policymakers and businesses alike face heightened uncertainty, which could stall investment and amplify economic vulnerabilities.

The broader implications extend beyond North America, as these tariffs challenge the spirit of the USMCA and highlight the fragility of globalized trade frameworks.