TFSAs and RRSPs

Debbie Bongard - Jan 07, 2019

As Canadians there are a few options available when choosing an account to invest your money. Two of the most popular investment vehicles today are TFSAs and RRSPs, both registered accounts that were created by the government to encourage Canadian’s

TFSAs and RRSPs

As Canadians there are a few tax efficient options available when choosing an account to invest your money. Two of the most popular investment vehicles today are TFSAs and RRSPs, both registered accounts that were created by the government to encourage Canadian’s to invest for their financial futures. RRSPs and TFSAs have different advantages and disadvantages which can impact which investment vehicle is right for you. In this article, we provide a brief summary of each account as well as differences between the two.

Tax-Free Savings Accounts

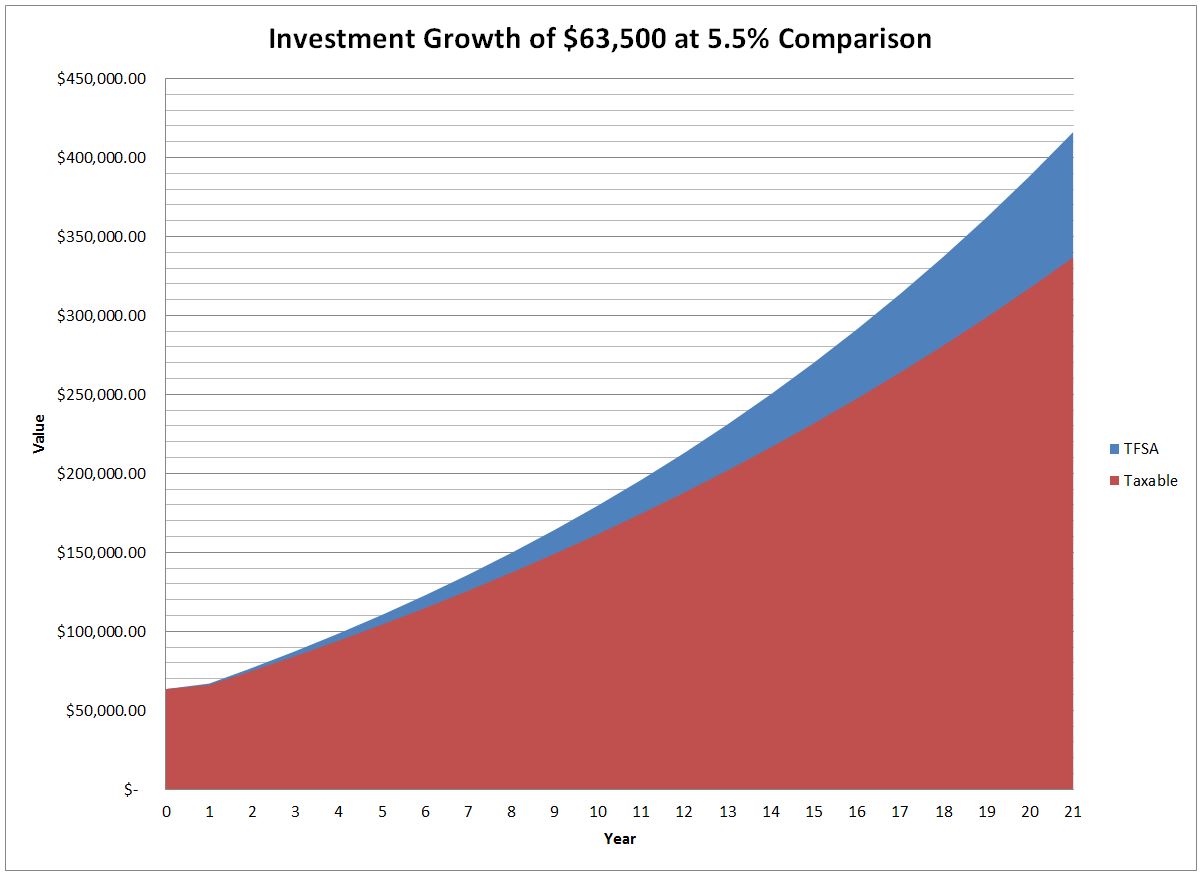

A Tax-Free Savings Account, TFSA, is a registered investment account available to Canadians over the age of 18 introduced by the government in 2009. As the name implies, any returns or income from money invested are tax-free. Therefore, if you contribute $1,000 to a TFSA, and it grows to $2,000, the $1,000 dollars of growth is not taxable. The best way to maximize the tax free benefits of a TFSA is through compound investment growth, where, over a longer time horizon, the difference between a TFSA and a taxable account become more pronounced.

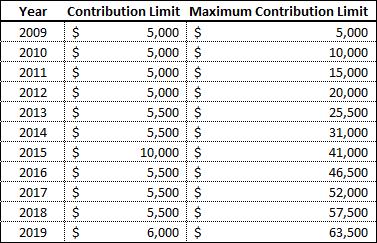

While TFSAs are a great investment vehicle, the contributions you can make to a TFSA are capped on an annual basis. As of 2019, the maximum that can be contributed to a TFSA is $63,500 (assuming you were 18 years of age or older in 2009). The contribution limit increases annually and for 2018 the contribution limit increased by $6,000. (Note, as of January 2019, the TFSA contribution limit is indexed inflation but increases intervals of $500) To check your TFSA contribution room, you can sign into your CRA portal, check your notice of assessment from your last tax return or call the CRA help line.

Contributions to a TFSA are made with after-tax income and if you do not make contributions in one year, you are able to carry forward any unused contribution room indefinitely. Additionally, due to the tax free benefits of the account, any withdrawals you make from your TFSA are tax free.

Furthermore, if you make a withdrawal from a TFSA you are able to recontribute the withdrawn funds the following year. For example, if you originally contributed $10,000 and it grew to $15,000, you would be able to withdraw the $15,000 in 2019 without any taxable consequences. In 2020, you would be able to contribute $21,000 to your TFSA, the annual contribution limit of $6,000 and the $15,000 you withdrew from the account in 2019.

With a TFSA, you are able to purchase a wide range of investments from individual stocks, GICs and bonds to diversified funds such as ETFs and Mutual Funds. These higher growth investment vehicles are more volatile than leaving your investments in a high interest savings account, but over a longer time horizon result in larger compound annual growth and can allow you to reap the most benefits of the TFSA.

The tax free benefits of a TFSA make it a great investment vehicle to save for large expenses that are a few years away, such as buying a house, as you are able to save funds tax free while benefiting from compound investment growth. Furthermore, the ability to recontribute funds to a TFSA after making a withdrawal means that you able to use your TFSA repeatedly for various goals over your life time.

Registered Retirement Savings Plans

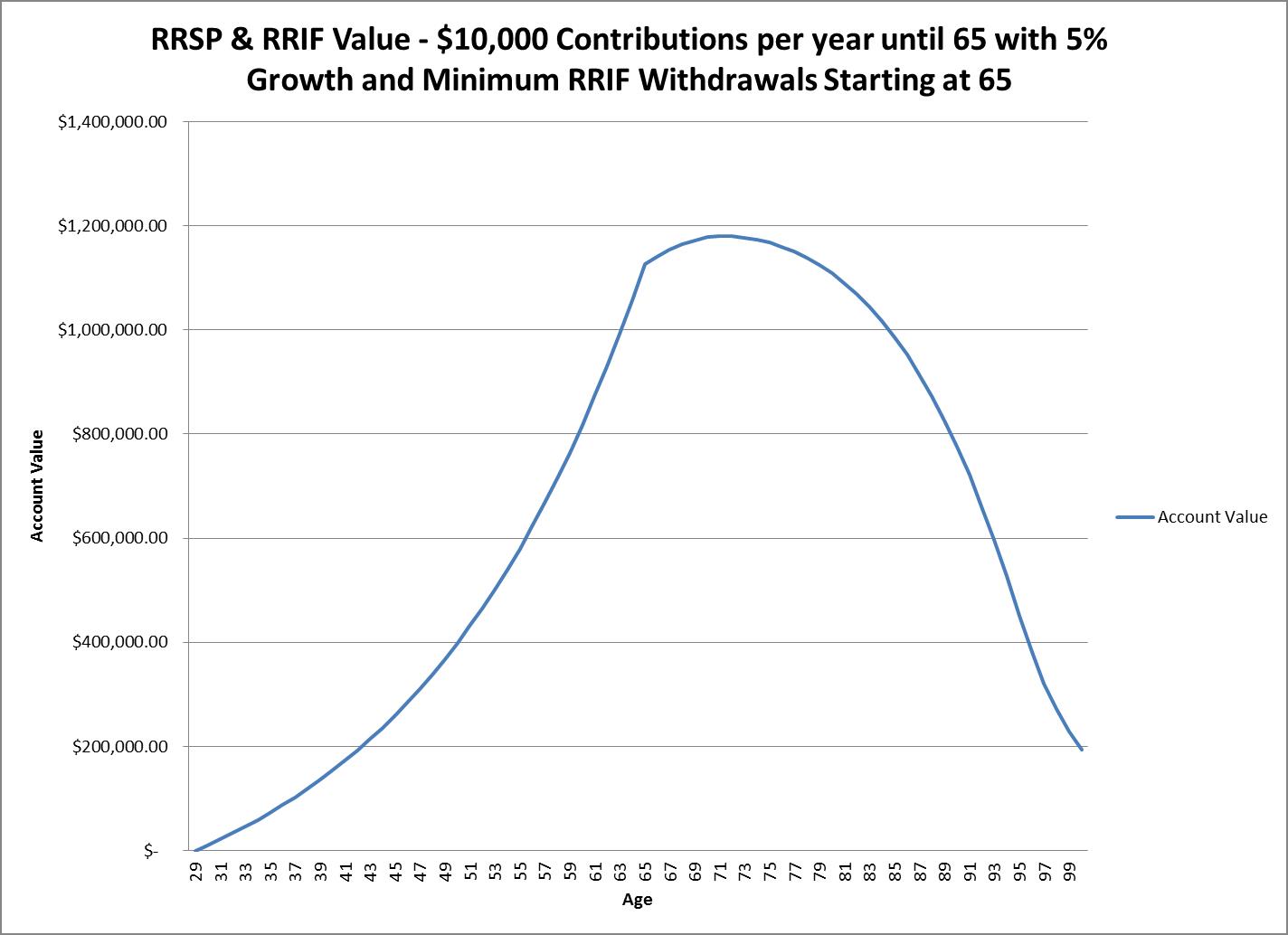

A Registered Retirement Savings Plan, an RRSP, is a registered investment account that is designed to help Canadians save and invest for retirement. In the past, many companies offered their employees a defined benefit pension plan, where an income stream would be provided to the retired employee upon retirement. In 1957, the government of Canada created the RRSP to allow Canadians without pensions to self-fund their own retirement. As defined benefit pensions plans have decreased over the last 60 years, the prevalence of RRSPs as a building block of investments savings in Canada has increased dramatically and has become the cornerstone of investment portfolios of most Canadians.

An RRSP is designed for long term savings and to eventually provide an income stream in retirement when it is converted to a Registered Retirement Income Fund by age 71. Canadians may contribute to an RRSP on a tax-deferred basis. Contributions made to an RRSP are made pre-tax with an offsetting income tax deduction equal to the amount of the contribution. Withdrawals that are made in retirement are taxable as income. With the tax deferral, one of the benefits you receive is theoretically a larger tax benefit from making contributions at a higher tax bracket during your working years compared to a lower tax bracket when you withdraw the funds in retirement. Additionally, the funds in the RRSP are able to compound over the next 20-30 years to create a nest egg to use to provide you income in retirement.

Furthermore, RRSP contributions allow you to receive a tax benefit while you are working that is applied at your marginal tax rate. A contribution to your RRSP will reduce your taxable income by the amount of the contribution, which can help reduce your annual tax bill and potentially receive a tax refund with your tax return. Like TFSAs, the annual contribution to an RRSP is capped. Currently, the cap is 18% percent of your earned income or $26,230, whichever number is less, also taking into account any group RRSP, defined benefit or defined contribution pension plans that you may have at work. Also like a TFSA, if you have missed your contribution in past years, you can catch up by contributing more at present. The amount you can contribute is listed in the Notice of Assessment you receive after filing taxes.

Typically, withdrawals from an RRSP are taxed as income at your marginal tax rate and included on your tax return. This does not make an RRSP an ideal investment vehicle for short term savings as it can greatly affect your income and taxes payable

RRSPs also have a special feature that allows you withdraw funds prior to retirement for the purpose of purchasing a house as a first time homebuyer through the Home Buyers’ Plan (HBP) or for higher education through the Lifelong Learning Plan (LLP). Each plan allows for funds to be withdrawn from the RRSP under certain conditions without taxable consequences and recontributed to the RRSP over a specified period. This flexibility allows you to use a portion of your RRSP for a shorter term goal such as purchasing a house while still saving for your retirement in future.

RRSPs are a great benefit to investors as they allow you to benefit from tax deductions while allowing compound investment growth to create a nest egg that will be available to use for income during retirement. RRSPs however are not good investment vehicles for short term investment savings as they have prohibitive rules that can greatly affect your taxes if you are not careful.

Comparing a RRSP to a TFSA

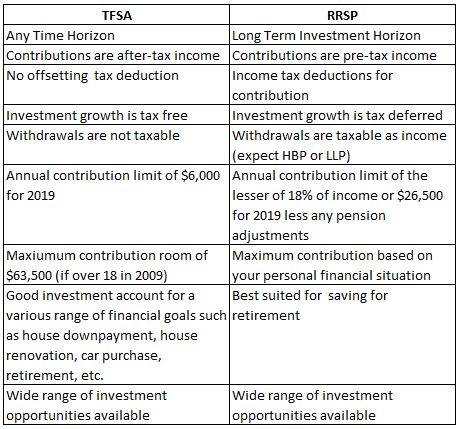

While TFSAs and RRSPs are both registered investment accounts that allow you to invest in various investment securities, the rules are quite different between the two and as a result it is important that you choose the right one for your individual financial goal and time horizon.

Many clients that we work with have multiple investment time horizons that they are working towards and each account can have a different goal, risk tolerance and time horizon. Much like you would use different knives in your kitchen for different tasks, TFSAs and RRSPs are highly differentiated to accomplish different goals. It is important that you know the difference between the two so you can best utilize the benefits of each account to your advantage.

If you liked this article, sign up for our newsletter.