Registered Education Savings Plans

Debbie Bongard - Apr 02, 2019

As a parent, you are probably hoping that your children will pursue post-secondary education or some form of higher learning after they graduate high school – and for good reason. Post-Secondary education is an invaluable asset – it can lead to a ful

Registered Education Savings Plan

As a parent, you are probably hoping that your children will pursue post-secondary education or some form of higher learning after they graduate high school – and for good reason. Post-Secondary education is an invaluable asset – it can lead to a fulfilling and successful career, increase their earnings potential and set your children on the path to living a healthy financial life into retirement.

However, tuition fees and associated university or college expenses have increased substantially. If we consider that the average undergraduate tuition fees in Canada were $1,764 in the early 1990s and that the average as of 2018 was $6,838, then educational expenses are outpacing inflation.

Further, the job market today is incredibly competitive and as a result, many young people in the early stages of their careers are looking to enhance their marketable skills in earning a second degree. This increases post-secondary education expenses even more – when we add up all the costs, it becomes imperative that education planning should be an important family wealth management consideration.

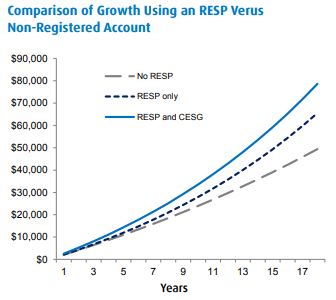

One of the most common saving tools for parents is a Registered Education Savings Plan (RESP). RESP contributions are not tax-deductible, nor are they considered taxable when withdrawn. Over the life of the RESP, you can contribute up to a maximum of $50,000 per child over a 31-year period, with no minimum annual contribution payment. However, you may be eligible for additional federal government grants via the Canada Education Savings Grant (CESG). Under this program, the Government of Canada will typically pay a grant of 20% of annual contributions up to a maximum $500 per beneficiary; this grant can be rolled over to the following year, where the maximum grant will subsequently be $1000 per beneficiary. When you make an RESP contribution, the government will pay a grant based on the beneficiary’s free contribution room; the grant amount is calculated as the lesser of the following three options:

-

20% of the RESP contribution amount;

20% of the RESP contribution amount; -

20% of available CESG contribution room;

-

$1000 (20% of $5000 dependent on if there is unused grant room from a previous year).

Children born after 1997 are eligible for CEGSs totalling $7,200. Your child may be eligible for additional education grants through various federal and provincial programs; more information can be found here.

Each RESP has a subscriber, which is usually the parents or grandparents, a promoter which is where the RESP is purchased through, such as your primary bank, and a beneficiary, who is the student if their enrolment at a post-secondary institution is confirmed and followed through.

The main benefit for using an RESP is that all contributions, any education grants received, and investment income is able to accumulate tax-sheltered. Additionally, when income and CESGs are paid out towards educational expenses they are named Education Assistance Payments (EAP). An EAP may consist of growth on principal contributions, CESGs as well as other federal and provincial payments, such as the Canada Learning Bond (CLB).

Any EAP is reported on the beneficiary’s T4A slip in each year that attend a qualifying post-secondary institution and are recipients of EAPs from their RESP. This is another key benefit to using an RESP as a primary savings vehicle, upon withdrawal payments are taxed at the hands of the beneficiary which results in little or no tax liability on the income.

EAPs may be paid out to the beneficiary under 2 circumstances:

-

They are enrolled in a qualifying educational program at a qualifying post-secondary educational institution;

-

The beneficiary has reached age 16 and is enrolled in a specified educational program

A qualifying educational program is a full-time college or university level program with a minimum length of 3 consecutive weeks and requires students to spend a minimum of 10 hours per week on courses and syllabus work. A specified educational program is a part-time program at the post-secondary educational institution. Again, the program must run for a minimum of 3 consecutive weeks – however, specified educational programs require students to spend a minimum of 12 hours per month on courses and syllabus work. The following institutions offer specified educational programs:

-

A university, college, Cégep, trade school or another designated Canadian educational institution;

-

A Canadian educational institution that is certified by Employment and Social Development Canada (ESDC) as offering non-credit courses that develop or improve skills in an occupation;

-

A university, college or other educational institution outside of Canada that offers courses at a post-secondary education level; the student must be enrolled on a full-time basis in a course that runs for a minimum of 13 consecutive weeks.

For the first 13 consecutive weeks of enrolment in a qualifying educational program, the maximum EAP is $5000. However, after completing the first 13 weeks, there is no limit on the amount of the EAP given that the beneficiary continues to remain qualified to receive EAPs. If, for whatever reason, there is a yearlong period wherein the beneficiary is no longer enrolled in a qualifying program, the $5000 limit will be reinstated for the first 13 weeks if they choose to enrol again. For a specified educational program, the maximum EAP is $2500 for the first 13 weeks. There are three types of payments available through an RESP: accumulated income payments, post-secondary payments and RESP payments to a designated educational institution.

Accumulated Income Payments (AIPs)

An AIP is a withdrawal of accumulated income from your RESP when your beneficiary does not attend a qualifying or specified educational program. As a subscriber, you may withdraw the accumulated income under the following conditions:

-

You are a Canadian resident;

-

The RESP has existed for at least 10 years; and

-

All beneficiaries listed under the RESP are at least 21 years of age and will not be attending post-secondary education.

-

If all beneficiaries are deceased, you may withdraw the accumulated income without meeting standards 2 and 3.

-

If the beneficiary is unable to pursue post-secondary education due to severe and prolonged mental impairment, the CRA may allow you to withdraw the accumulated income without meeting standards 2 and 3.

-

If the plan is being closed at the end of the 35th year, the CRA may allow you to withdraw the accumulated income without meeting standards 2 and 3.

When the income is returned as an AIP it is taxed at the hands of the subscriber as ordinary income with an additional tax levy of 20% or 12% in Quebec. The income tax can be deferred, and the tax levy avoided if the subscriber has sufficient RRSP contribution room. A maximum of $50,000 of the accumulated income may be used to make a regular or spousal contribution. As a result, only income in excess of $50,000 will be taxed as regular with the additional tax levy. Under certain conditions, the accumulated income can also be transferred to a Registered Disability Savings Plan (RDSP) if the beneficiary is listed under both the RESP and the RDSP.

Post-Secondary Education Payments (PSE)

If the beneficiary’s education expenses exceed the maximum EAP payment, utilizing a PSE may be in your best interest. A PSE is the return of the original RESP contributions with no tax consequences. If the beneficiary decides not to pursue post-secondary education, all contributions can be returned to the subscriber with no tax consequences through PSEs. However, under this pretense, you may have to repay any CESGs in the RESP.

RESP payments to a designated educational institution

This payment refers to any amount that is left in the RESP after maximizing EAPs, and wherein conditions to return capital through an ESP or AIP cannot be met, the balance can be bestowed to a designated educational institution in Canada.

To sum, do not act impulsively in making a decision to collapse an RESP. It is important to consider whether the beneficiary may eventually want to pursue post-secondary education later in life. Further, you have the option to keep an RESP open for a maximum of 35 years and CESGs may be shared with other siblings with the available grant room. Speak to a Financial Advisor concerning the best payment structure for you.