Good Debt and Bad Debt: How to Avoid Living in the Red

Debbie Bongard - Aug 09, 2019

With the inevitability of having to take on some significant debt in your lifetime, it is important that you understand different types of debt and how to effectively manage it. Are some types of debts better than others? Which debt should I pay off

In an ideal world, we would all be ‘living in the black’. No debts, no problems – right? This expectation, however, is highly unrealistic for the majority of Canadians. People don’t tend to have $500,000 lying around to buy a house, or $30,000 to pay for post-secondary education. With the inevitability of having to take on some significant debt in your lifetime, there is an important distinction that needs to be understood regarding good and bad kinds of debt. Moreover, what types of debts should you pay off first?

First, let’s make a distinction between good and bad debt.

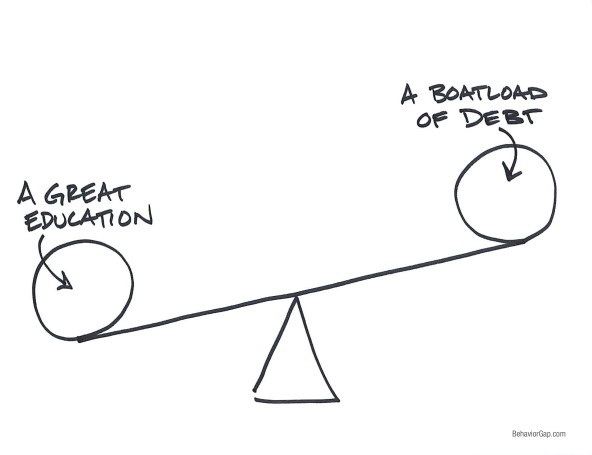

Good debts. Good debts are debts that hold the potential to improve your future financial position. Taking out a loan for a technical college, university, or other form of post-secondary education, is an example of a good debt because education can increase your employability and can set you up for higher earning potential. Further, good debts tend to have lower interest rates, may be tax deductible, and are sometimes tied to real estate. A home mortgage is another example of a good debt.

Bad debts. A bad debt, on the other hand, is when you are borrowing money to purchase assets that will immediately begin to depreciate in value. In other words, if the debt incurred does not go up in value or generate future income, it is a bad debt. Common examples of bad debts include new car purchases, various consumer goods (i.e. clothing), and credit card debt. Bad debts tend to have high interest rates and aren’t secured to property.

It is important to note that the relationship between incurring good debts and greater income in the future is not without flaw. It is not guaranteed that taking on good debts will pay off in the future. For example, if you take out a business loan with the objective of starting a small business, it does not mean that your business will necessarily succeed. Similarly, pursuing a post-secondary education does not necessarily translate into employment, due to various external factors, such as unemployment rates and technological development that can hinder your ability to find a job.

Depending on your financial priorities and your personal motivation to be debt-free, your debt repayment schedule will look different. Some people want to tackle their largest debt first, and others find it more rewarding to pay off the debts with smaller balances. Some people also prefer to live very frugally and pay off all debt as quickly as possible, whereas others pay it off slower so as to not hugely impact their standard of living. While these are highly personal decisions, here are a few general tips and tricks that will help you manage life in the red and debt repayment.

Make all minimum payments. Before focusing on paying down one debt, ensure that you can make the minimum payments on all of your debts. Failing to make minimum payments can hurt your credit score which can limit your ability to get approved for credit cards and take loans from a bank. Setting up automatic deposits and calendar reminders are good ways to ensure that you are keeping track of your different accounts. Marking your payment schedule in your calendar also allows you to see the progress you are making and stay motivated.

Pay down high-interest debts first. Having enormous credit card bills can be viewed as equivalent to burning cash. For high-interest debts, you incur large amounts of interest in addition to the principal amount, meaning a significant portion of your monthly payment is not actually going towards paying off the principal loan, but instead paying interest. Once you have paid the minimum payments on all of your debts, you should focus your efforts on paying down those with high-interest rates.

Example: Let’s say you are going to put $1,000 towards some personal debt repayment. If you are putting that $1,000 towards a $5,000 credit card bill that has a 20% interest rate you will be saving a lot more money than if you were to put the $1,000 towards a $5,000 student loan that has a 5% interest rate. Choosing either option will feel the same to you in the moment, but paying off the high interest debt can result in significant savings in the long run.

Negotiate. You don’t get without asking. While some bills like mortgage payments, car payments, and property taxes are non-negotiable, there are some types of bills that you might be able to get reduced. Some negotiable bills include expenses such as cable or satellite television, internet, phone bills, and car insurance rates. If you can prove that you have a reliable history of making your payments, present competitor’s superior prices/rates, and show you are ready to switch service providers, you have strong leverage to negotiate for lower prices and rates. The worst case is just that they say no.

Even saving a small amount of money on these types of monthly payments will free up more money so that you are able to pay off other debts faster.

Don’t quit. Paying off any form of debt can take years and years and can be a frustrating process, but don’t quit. If you were attempting to pay off the largest debt and are frustrated with the amount of time it is taking, switch up your strategy and start paying off some of the smaller debts. Being able to tackle the smaller debts and check them off the list can give you confidence in your progress and motivate you to keep working towards your personal financial goals.

Remember: Debt repayment is a marathon, not a sprint; so make sure that you give yourself small rewards when you hit certain milestones.

As with all personal financial matters, different strategies work best for different people when it comes to debt management. By reflecting on your personal financial situation and financial priorities, you can begin to make a solid debt management plan using some of the previously mentioned tips. If you are feeling overwhelmed by your debts, please don't hesitate to reach out to any financial professionals on our team for assistance.