Risk Adversity & Your Emergency Fund: Finding the Balance

Debbie Bongard - Nov 28, 2019

If you have heard one piece of personal financial advice, it is likely one that preaches the importance of having an emergency fund. It is one of the only things that nearly all financial experts unanimously agree upon. While its’ importance goes unc

Risk Adversity & Your Emergency Fund: Finding the Balance

If you have heard one piece of personal financial advice, it is likely one that preaches the importance of having an emergency fund. It is one of the only things that nearly all financial experts unanimously agree upon. While its’ importance goes uncontested, just how much money you should set aside in your emergency fund is argued among many.

Some personal finance experts argue that you should set aside three-months worth of your living expenses, while others argue that an individual would ideally have one-years worth of living expenses covered in your emergency fund. So, what is the right answer?

This article does not aim to provide you with a simple formula that will help you determine just how much money you should set aside for your emergency fund. The truth is that there is no appropriate definitive answer to that question.

Money is highly personal. As such, you need to consider various factors, such as your lifestyle, risk aversion level, and personal and financial goals when setting up your emergency fund. It is these factors, among others, that will shape the decisions you make surrounding your emergency fund. How much money should you put in your emergency fund? Moreover, where are you going to hold the money in your emergency fund?

What is an emergency fund?

An emergency fund is a stash of money that is set aside in case unexpected circumstances arise that have the potential to pose a threat to your financial wellbeing. An emergency fund provides you with a financial cushion in the event you suddenly lose your job, have a medical emergency, experience car troubles, and other unforeseen circumstances. One of the most notable benefits of having this safety net of cash is the peace of mind it brings you knowing that you are protected in the case of an emergency.

Emergency funds are typically kept in a savings account - safely stowed away from the unpredictability of the stock market. As a result, the funds are also not earning the investment income they would if properly invested in the stock market.

What is risk aversion?

By definition, risk aversion is the behavior of humans, who, when exposed to uncertainty, attempt to lower that uncertainty.

People inherently possess very different levels of risk aversion. As an extension of such, people’s lifestyles and the choices they make will differ greatly. Your personal financial plan should be created with this in mind. Your risk aversion level will have a direct impact on the types of investment decisions you make, as well as how much money you need in your emergency fund to feel comfortable and secure.

In reference to personal finance, a highly risk adverse individual would likely hold investments with known, manageable risks. Since the risks on these more stable investments are generally understood, they typically produce much lower returns. An individual who possesses a low aversion to risk would be much more likely to invest in more uncertain securities in pursuit of higher returns on their investment.

Understanding how much risk investors can tolerate is critically important for determining the types of instruments they should invest their money in. Why shouldn’t the concept of risk aversion be incorporated into an individual’s emergency fund plan, then?

How can your level of risk aversion inform decisions surrounding your emergency fund?

The easiest way to answer this question is with an example:

As a compromise between the personal financial experts that argue your emergency fund should cover three-months of living expenses vs. those who argue your emergency fund should cover a year’s worth of expenses, for the sake of this example, let’s say we want our hypothetical emergency fund to cover six-months of living expenses.

A 2019 survey by Lowest Rates Canada, estimates that an average single Canadian living in Toronto will have approximately $2,780 in monthly expenses. This includes housing, transportation, groceries, phone and internet, and modest entertainment expenses. Given our six-month requirement, our emergency fund should have $16,682.88 in it. For simplicity’s sake, we are going to say that our emergency fund should have $16,000 in it.

Now, let’s consider two individuals that possess very contrasting levels of risk aversion – the first having a high level or risk aversion, and the second having a very low aversion to risk and uncertainty.

-

High risk aversion

Along with displaying very safe financial habits (i.e. having a highly diversified investment portfolio composed of low-risk, low-return stock), an individual who is highly risk adverse would likely place great importance on establishing an emergency fund. This is because they want to protect themselves in the face of future uncertainty. So, for a highly risk adverse person, where is the safest place to keep your emergency fund?

As mentioned previously, the safest place to put your emergency fund money is in a savings account. A savings account allows your money to earn interest without being subject to the unpredictability and volatility of the stock market. While the interest earned on the money in this savings account will be less than the historical average rate of return of the stock market, you can be assured that every dollar in the account will remain untouched until you decide to withdrawal it.

Example:

While Canadian savings accounts typically have an interest rate of approximately 1%, for the sake of this example, we are going to assume we are using a high-interest savings account that will give us a 2% rate of return.

Assuming you contribute $16,000 into your savings account and let it sit earning compound interest at an interest rate of 2% for 20 years (you don’t have an emergency for 20 years), the total value of your investment would be $23,775.16. The total interest you have earned on your initial contribution over the 20-year period is $7,775.16.

-

Low risk aversion

Now, let’s take a look at an individual who has a low aversion to risk. Along with displaying riskier financial habits (i.e. investing in individual stock that could provide high returns, thus are higher-risk), an individual with low risk aversion will likely not prioritize establishing an emergency fund. If you’re inherently not particularly anxious about future uncertainty, you will likely have less motivation to plan for events that could harm your future financial wellbeing. So what would an emergency fund look like for a person who has low risk aversion?

Stowing money away safely in a savings account would not necessarily be the appropriate answer for individuals with low aversion to risk. A low risk adverse individual would be more inclined to invest their money in the stock market as it offers the possibility of a higher return. By assuming more risk and having to weather the ups-and-downs of the market, they have the ability to earn a higher rate of return on their money.

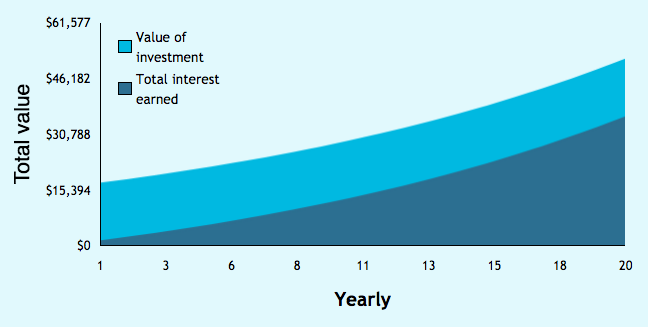

Example:

While it can vary greatly depending on the individual and their investment decisions, the historical average rate of return of the stock market is approximately 6-10%.

Assuming similar conditions as the aforementioned example, investing $16,000 of ‘emergency fund money’ into the stock market (with an expected 6% rate of return) would result in the total value of your principal investment equaling $51,314.17 after 20 years of compounded growth. Total interest earned on your initial investment would be $35,314.17.

Comparing the two situations:

The high risk adverse individual earned $7,775.16 in interest on their original investment. The low risk adverse individual earned $35,314.17 in investment income. If asked to choose which outcome is preferred, any objective investor would choose the latter. It is important to remember, however, that people who invest in the stock market have to be able to mentally and financially withstand the stock market’s short term volatility. There are also countless other factors that affect an individual’s willingness to assume risk.

An individual’s age is another variable that can impact what level of risk the individual is willing to take on. For example, an individual who has saved diligently and is now enjoying a very comfortable retirement may be less inclined to invest their ‘emergency fund’ money in the stock market. It is highly unlikely that an individual’s primary financial goal, at the age of retirement, is to continue to accumulate wealth. Therefore, they would likely not assume the heightened risk associated with the stock market’s short term volatility.

Going back to the original question, “how much money should I keep for emergencies?”

Unfortunately, providing you with a black or white answer to this question is not sufficient, as it greatly simplifies a financial decision that is more complex and demands greater thought. Determine where you lie on the risk tolerance spectrum by examining your personal risk tolerance level. Any decisions to be made surrounding your emergency fund, including how much you should set aside and in what type of account, should be made with this in mind.

The reality is that the vast majority of people fall somewhere in the middle of this risk tolerance spectrum. Adopting a mix of lower-risk financial behaviors (i.e. keeping some money in a savings account) and higher-risk financial behaviors (i.e. investing in the stock market) can provide you with a degree of financial security, while also allowing you to invest in securities that offer can offer you a higher rate of return.

Conclusion

Undoubtedly, the emergency fund serves as a fundamental component of any good personal financial plan. As with all financial dealings, what your emergency fund looks like will be a personal decision. By assessing your lifestyle, your level of adversity to risk, and your pre-existing financial cushion, you will be able to determine just how much you want to contribute to your emergency fund and what sort of account that money will sit in.

If you have any questions, please do not hesitate to reach out to myself or any member of the Bongard Wealth Advisory Group to learn more.