MWW - Fog of War, Haze of Ceasefire, Mist of Blockade

DHL Wealth Advisory - May 15, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Some of our long-time readers will recall our notes from 2021–2023, when it felt like every MWW had a single leading character: Inflation. We often apologized for the lack of variety, but at the time, it was the only story markets cared to read.

This past week we had a slew of economic data that showed a rise in inflationary pressure, largely stemming from the war in Iran. It’s hard for some investors to reconcile events in the Middle East (and $100+ oil) with all-time highs in equity indices. Understandably, the media is focused on the conflict in Iran, but there are many other macro influences when it comes to equities. The same elements that were supportive for stocks prior to March are still in play. Surely, it’s not the same story as it was back in February as higher energy prices will be an offset to the stimulus, but so far it still adds up to an economic recovery. That part is clear. Equity prices would not likely sit at all-time highs if we were headed toward a recession. That’s where we are as of today. Where we are going is a different debate as this is a fluid story and ultimately, we don’t know exactly where oil prices will settle. What we do know is that if the rise in energy prices is much more prolonged, it likely has more serious consequences for the economy and equities. That part might not be completely priced into the major indices.

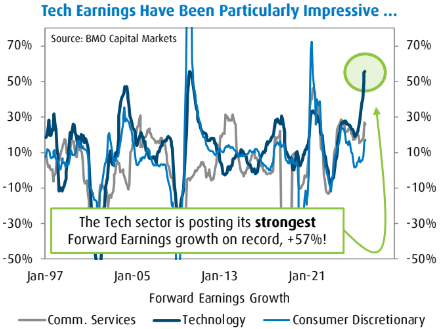

The events in the Middle East were certainly shocking at first and equity markets reacted accordingly. That said, once investors refocused on earnings in April it felt like equities were basically looking past the situation in Iran. This is a bit of an exaggeration, but dynamically speaking it certainly looks that way. The earnings picture for the S&P 500 is absolutely stunning right now. Not only are earnings expectations recovering broadly BUT the Technology sector is growing at rates never seen before. This is obviously a positive, but it raises the question of whether it’s sustainable, AND also whether we might be getting a tad ahead of ourselves.

There’s good news on the sustainability issue, for the broader market at least. The lagged effects of stimulus sparked the recovery in earnings estimates. It doesn’t always look that way when analyzing a specific security, but the ebbs and flows in the economy explain trends eventually seen in earnings. This is where the causality lies. A world marked by lower interest rates usually leads to a recovery in the economy and earnings. If past trends in rates is any indication, the acceleration in S&P 500 earnings might just last throughout the year and much of 2027. This is only one part of the equity equation, but it is highly supportive at this time.

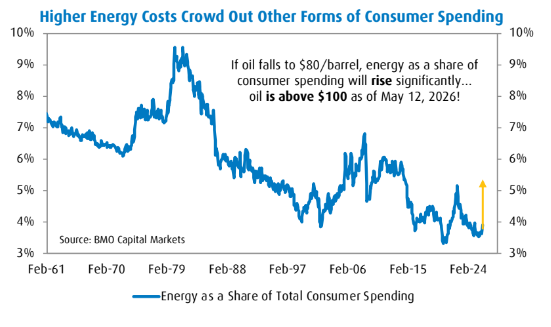

Coming back to the topic de jour, the U.S. has an embedded inflation problem in its economy. It largely has to do with the dwindling labor supply in recent years relative to history. This is due to several developments, including negative demographics trends (Baby Boomers retiring) and immigration policy. This has been a common discussion for some time, but it’s even more consequential for inflation than what’s happening in the Middle East. For the former, we need to worry about a potential rise in wage inflation, while the latter is largely about energy costs. Note that a spike in energy costs does typically lead to a broader rise in price levels due to production costs, shipping costs, and a host of other issues. The impact of a rise in energy prices comes with little delay as it is almost simultaneously visible at the gas pump. In that vein, it feels like a sudden rise in tax rates for both consumers and businesses. Which is what we saw in this week’s inflation data.

Energy as a share of consumption spending is already up half a percentage point. This will inevitably crowd out some spending on other items. On the bright side, one good thing we can point to is that the events in Iran are happening while the U.S. economy is doing well. Earnings are growing, and there is plenty of stimulus in the pipeline that argues for a continuation of this dynamic. Further, while nobody is going to argue that higher energy prices are good for consumer spending, the share of consumer spending allocated towards energy has steadily lowered over time and is in a clear downward trend.

All in, the US Fed is likely to sit on the sidelines for at least the next few meetings as they are wanting to look through what could be a temporary spike in energy prices. Economists still think it is possible that we could see a US rate cut by the end of the year, should oil prices and inflation moderate, but it would not be a surprise to see the Fed stay on hold. The upshot is that bonds might struggle to recover, and pundits continue to expect the 10-year Treasury yield to remain stuck in the 4.0%-4.5% range. In Canada, the shift in market pricing towards potentially multiple interest rate hikes looks overdone. Instead BMO’s economics team expects the Bank of Canada to leave rates unchanged at 2.25%, providing modest support to the economy in the face of weak activity rates and rising labour market slack.

Markets are forward looking, and the move to new record highs reflects the (seemingly) waning risks around the Iran conflict and an improving economic and earnings backdrop. Importantly, with much of this positive news now priced in, it might be hard to maintain the recent momentum in stocks. In our view, it would not be a surprise to see a period of market consolidation, characterized by slower and bumpier gains in the coming months (today gave us a touch of that).

However, looking through these fits and starts, we think the latest economic signals remain supportive of this ongoing bull market, and we continue to recommend remaining invested in a diversified allocation to equities.

Sources: BMO Capital Markets - Portfolio Strategy - It’s Time To Have A Serious Conversation About Inflation

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.