MWW - All Quiet on the (Middle) Eastern Front?

DHL Wealth Advisory - Apr 17, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

The two-week ceasefire between the U.S., Iran and Israel continues to provide a welcome de-escalation in a conflict that has shaken global markets.

The two-week ceasefire between the U.S., Iran and Israel continues to provide a welcome de-escalation in a conflict that has shaken global markets. The relief rally since this announcement has been sharp, with equities hitting all-time highs today and oil tumbling roughly $40/barrel from its high, or ~35%.

However, it remains to be seen if consensus toward a more permanent agreement can be found over the next fortnight on issues including nuclear security, traffic through the Strait of Hormuz, and security guarantees.

Therefore, while volatility has dropped sharply in recent days, we are not necessarily out of the woods. There remains a risk of further market stress in the near term, especially as we approach the end of the current ceasefire on April 21. That said, reasons for optimism are on the rise with a 10-day ceasefire between Lebanon and Israel, and another round of talks between Iran and the U.S. potentially happening this weekend.

Still, we interpret the willingness to engage in a mutual ceasefire, the start of direct negotiations, international support/pressure for a deal, and hopefully an improvement in transit through the Strait of Hormuz as positive signals around an eventual resolution in this conflict, even if the path might be bumpy.

The bad news, in our view, is that even assuming a moderation in oil prices from here, this likely won't be the peak in inflation in what should be a temporary spike in the reading. U.S. gas prices in April are running higher than the Consumer Price Index (CPI inflation) survey showed in March, and the spike in oil prices will feed into other goods prices too. We expect inflation pressures to peak in the second quarter before moderating slowly in the second half and falling back more rapidly in early 2027.

That said, there were still glimmers of better news in last week’s CPI inflation report. Shelter inflation, which captures housing costs, continues to trend lower, and price increases across other services were moderate too. We think these signals should make us more confident that price pressures will normalize once we have moved through the latest spikes in goods and energy prices.

Canadian inflation data for March will not be released until later this month. However, a similar spike in price growth should be anticipated based on what we have seen in domestic gas prices. Average prices in March were up nearly 30% over those in February, and economists are forecasting an acceleration in headline CPI inflation rates to nearly 3% year over year over the second quarter, up from estimates of 2.3% before the Iran shock.

Similar to our views on U.S. inflation, we expect the pick-up in Canadian price pressures to be narrowly concentrated around oil-sensitive goods and temporary, especially given a sluggish labour-market backdrop.

We think these developments should serve to sharpen U.S. political incentives to find a durable conclusion to the conflict that helps bring oil prices lower over time. In a midterm year, we continue to see President Trump's approval ratings deteriorate, with views on his handling of the economy and foreign policy both deep underwater (despite putting an end to 9 wars in 12 months...). A more prolonged energy crisis could risk exacerbating his approval slide.

As we often talk about, markets are forward-looking and are now starting to see an end to this conflict. Looking further ahead, while the path to an eventual agreement remains opaque, we continue to believe this is the most likely outcome. Importantly, a peace deal could set the stage for investors to shift their focus away from energy price risks and back to fundamentals around growth and corporate earnings.

We think these fundamentals, including broadening corporate profitability, tax cuts and fiscal stimulus, lower interest rates and U.S. deregulation, should remain intact, although slightly bruised, by this crisis.

The overall tone from this week’s slate of economic data was constructive. China reported firmer-than-expected Q1 GDP at 5.0% y/y (well up from 4.5% in Q4), even with a marked cooling in exports, retail sales and industrial output in March amid the war. Even the U.K., which has been struggling heavily to grow, posted a surprisingly perky February GDP gain of 0.5%, lifting output at a 2% rate over the past three months. Meanwhile, U.S. indicators were mixed for March, but the really early results in April have been surprisingly upbeat. For example, both of the regional factory surveys from the Empire State and Philly popped, while the weekly ADP report shows a distinct upswing in employment in recent weeks—a tantalizing hint that the hiring lethargy around the turn of the year has truly been shaken off.

With respect to earnings, outside of the energy sector and parts of technology, we would expect earnings estimates in most sectors to be revised a little lower this year, consistent with the downgrades we are seeing in domestic, U.S. and international growth forecasts. However, despite these adjustments, we think economic and earnings growth is still likely to be firmly positive in 2026.

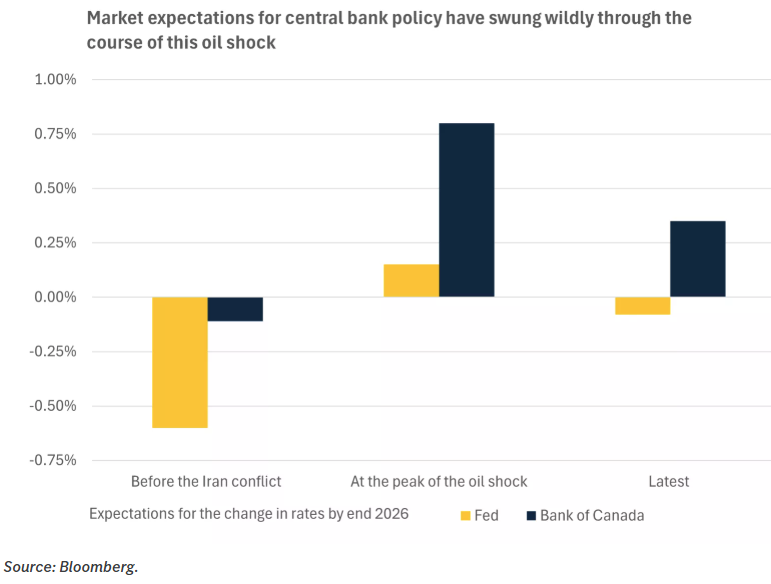

For central banks, there have been some wild shifts in market interest-rate expectations over recent weeks. In the U.S., markets priced out expectations for interest-rate cuts this year during the peak of the Iran scare and even flirted with a chance that the Fed could hike. However, as oil prices plummet, we are seeing expectations for easing build again. We think there could be scope for the Fed to cut rates by the end of the year, depending on the path for oil prices and inflation.

Moves in Canadian interest-rate expectations have been even larger. Markets went from pricing in a rate cut before the oil shock to anticipating three or more hikes at the peak of this scare. We have seen these bets fall back to imply one or two rate hikes alongside the decline in oil prices. While risks are tilted toward policy tightening given near-term inflation concerns, we think it is more likely that the central bank stays on hold. Interest rates at 2.25% are offering some support for an economy dealing with shocks to energy prices and U.S. trade policy. This stance feels appropriate, especially given that we think the unfolding inflation spike should be temporary.

Overall, the conflict in Iran has dominated the news cycle and market sentiment since March. In our view, however, if tail risks are fading, the market should continue to turn its attention back to the still supportive fundamentals that had been driving positive performance before this shock.

Sources: BMO Economics Talking Points: All Quiet on the (Middle) Eastern Front?

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.