MWW - See You On The Dark Side of the Truce

DHL Wealth Advisory - Apr 10, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Global equities just wrapped up their best week in exactly a year as tensions in the Middle East took a welcomed step back.

What a difference a week can make...

Global equities just wrapped up their best week in exactly a year as tensions in the Middle East took a welcomed step back. An eleventh-hour agreement forestalled President Donald Trump’s threat to destroy infrastructure across Iran and set the stage for direct peace negotiations between the two sides as part of a two-week ceasefire deal.

Trump’s initial post on Tuesday indicated the basis for this agreement was a 10-point plan put forward by the Iranians, a list that excludes many core U.S. security objectives on which the war was originally predicated. Narratives were shifting by early Wednesday when President Trump noted he had a different version of the 10 point plan.

All eyes will be on Pakistan this weekend as key administration officials will be traveling to Islamabad to begin more direct talks (versus the intermediaries both sides have been using to date). It is fair to say that significant points of contention remain. Even though the U.S. military has seen awe-inspiring tactical success on the battlefield, strategic success is open to interpretation. Iran’s leadership has changed, but regime 3.0 is more hard line than its predecessors. The Strait of Hormuz has historically operated under international freedom of navigation rules, but Iran has now proven its ability to shut the waterway and may gain control of daily goods flow from the Arabian Gulf going forward. Hopefully, this two-week ceasefire will provide time for the U.S. and Iran to advance a mutually acceptable framework that leads to a long-term deal. The initial market reaction to the ceasefire was euphoric with strong stock and bond rallies around the globe; oil prices fell close to 20%.

And that’s the heart of the issue for investors: the price of oil and the inflationary impact to the consumer and the state of the economy. Adam Smith, one of the earliest observers of North American business, suggested all industry exists for one basic purpose: to serve the consumer. Indeed, consumption is the staff of life for economic activity, driving over half of Canadian two-thirds of U.S. GDP.

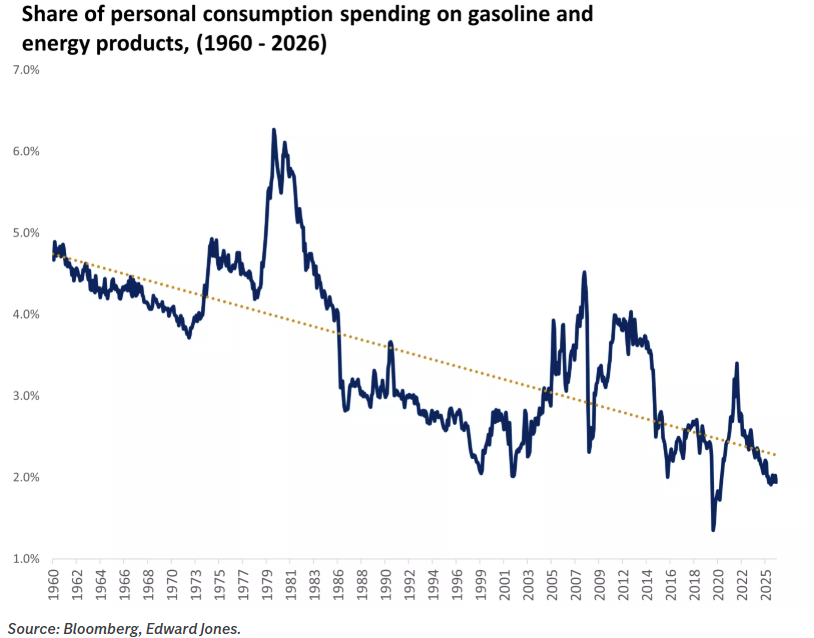

We shared the below table a few weeks ago, but it’s worth revisiting today given the price at the pump is front of mind. The sticker shock is unpleasant, but energy is a smaller drag on consumers than it used to be: Energy spending as a share of total consumer spending is materially lower than it was during the 1970s and early 1980s (roughly 2% today versus about 6% then), suggesting that the direct hit to household purchasing power from a given oil shock is smaller today.

Canada and the U.S. are far more insulated on the supply side — Canada has been exporting energy for decades, the U.S. has been a net exporter of oil since 2019, and North American natural-gas prices have remained relatively insulated from the disruption, even as Europe and Asia face a supply crunch. Canadian and U.S. producers stand to benefit from higher prices, even if that support does not fully offset the drag from weaker consumer spending.

Oil still matters, but less in a services-based economy — Large oil-price moves still hurt, but the global economy is simply less oil-intensive than it was during the original energy crises. Since 1950, the amount of energy required to produce one unit of GDP has fallen by roughly 70%, reflecting efficiency gains and the growing importance of the services sector.

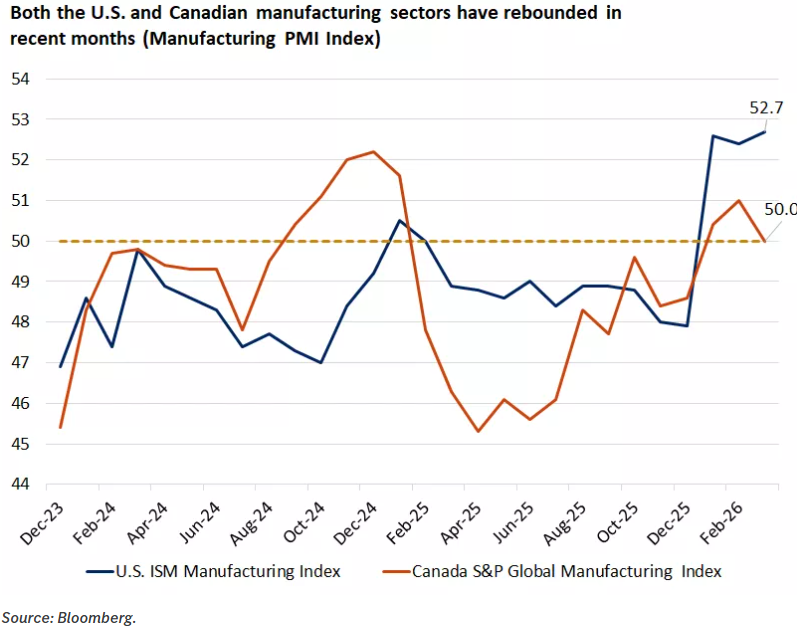

Next week officially marks the beginning of a Q2 earnings season with Fundamentals very much in focus. The U.S. and Canadian economies also continue to show signs of resilience in recent economic datapoints. Last week, U.S. retail sales and ISM manufacturing data came out above expectations. The retail-sales figure for February showed retail sales excluding autos advancing by 0.5% monthly, above forecasts of 0.3% and last month's flat reading. This points to a U.S. consumer that continues to spend at a healthy rate, heading into the Iran crisis. Meanwhile, ISM manufacturing for March came in at 52.7, above forecasts of 52.3, and still indicating expansion in the U.S. manufacturing economy.

Similarly, in Canada, the S&P Global Manufacturing survey came out at 50.0 for March, below last month's 51 reading, but still in expansion territory.

Overall, the U.S. and Canadian economies seem to be on pace for steady growth in the first quarter, with no meaningful signs of cracks, in our view, despite the geopolitical uncertainty that emerged in March. We will continue to monitor both inflation and economic growth metrics in the weeks and months ahead, but the early signals of resilience are a good reminder that these economies entered the current crisis from a position of relative strength.

Bottom Line: Don’t play politics with your portfolios.

Overall, despite the headline noise, the U.S. S&P 500 is basically flat on the year, while the Canadian TSX is up a staggering 6% (largely on the back of the index concretion in metals and oil). We believe that for long-term investors, now is not the time to make emotionally charged investment decisions, but to instead consider a simple pulse check on your portfolio:

1) Do you remain aligned with your strategic allocations in equities and bonds? There may be an opportunity to rebalance if some investments have moved in an outsized way.

2) Do you have excess cash or cash-like instruments that could be used opportunistically? If so, this might be a good time to look at quality investments that have repriced lower and gradually add them to portfolios.

You can take these steps on your own or talk to our team who can help ensure that you remain on-track to meet your financial goals. Remember, your diversified investment plan is designed to help you withstand bouts of market volatility over the long term, regardless of the geopolitical uncertainty we may be facing today.

Sources: Weekly Strategy Perspectives – A BMO Private Wealth Publication

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.