MWW - Tariffs: The Plan, The Courts, The Sequel

DHL Wealth Advisory - Feb 27, 2026

Fresh off the Olympics, the markets’ new sport was climbing an ice-wall of worry this week. From the ripple effect of the Supreme Court ruling on IEEPA tariffs; to the latest AIpocalypse fable...

Fresh off the Olympics, the markets’ new sport was climbing an ice-wall of worry this week. From the ripple effect of the Supreme Court ruling on IEEPA tariffs; to the latest AIpocalypse fable; to tensions with Iran; to the State of the Union address, it was full of challenges. The end result in a back-and-forth week was a small net pullback in U.S. equities, and an end to a 10-month streak of gains for the Down Jones Industrial average. Surprisingly, looking to the S&P500, which is the broadest sense of the US market, the S&P 500 has been stuck in a 2% range for almost four months now. Effectively unchanged.

From an economic perspective, it’s the renewed uncertainty around the trade file that has the most relevance, at least for now. In an otherwise relatively quiet week on the data front, the reality that U.S. tariff rates are back in flux caused some consternation. Not helping was that the brand new, and never previously attempted, Section 122 tariffs were first threatened at 10%, then 15%, then set at 10%, with a warning they’re going to 15%, for some, all within a few days. It was like the good old days of early 2025 all over again. The net impact has been a lower overall tariff rate, with particular relief for economies that had not managed to reach a full deal with the U.S., including China, Brazil and India.

What will ultimately replace the Section 122 tariffs, which have a 150-day time limit? In theory, Congress could extend these broad tariffs, but there appears to be very little appetite for that, especially in the run-up to the mid-term elections. For the purposes of our economic forecast, we will assume that the Administration is able to largely re-create its tariff wall through sectoral and country-specific measures—but the risk seems to be that the end result is less, not more. That’s unsurprising, given the lack of widespread support for tariffs.

While we have marveled at the lack of economic impact over the past year from the trade war, especially in the U.S. data, it cuts both ways. Yes, inflation did not get driven substantially higher by tariffs, although it also didn’t fade even with mild energy prices. (And, January’s U.S. Producer Price Inflation showed some real heat in core goods prices, which popped 0.7% m/m and are now up a meaty 4.2% y/y, double the pace of a year ago.) And, yes, the economy managed to grind out 2.2% real GDP growth last year, very close to pre-trade-war expectations. But on the flip side, the trade deficit in goods actually widened slightly for all of 2025 to a new record high. And, manufacturing payrolls have declined by 83,000 over the past 12 months (-0.7%), even as factory output has eked out a 2.5% advance. So, perhaps no pain, but also no gain.

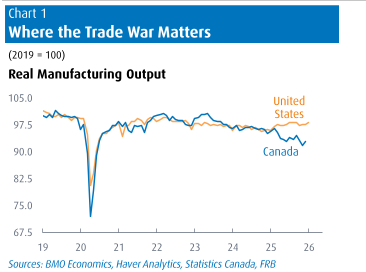

Unfortunately, we cannot say that there has been “no pain” in the Canadian economy from the trade war. In contrast to the moderate rise in U.S. manufacturing output in the past year, Canada’s factory sector saw a 3.6% drop in real output (Q4/Q4), including a 10% dive in primary metals (Chart 1). And while the President often rails about Canada “stealing” the auto industry, the reality is that Canadian assemblies have withered to just 1.2 million units in the past year. That’s half the pace of just a decade ago, well below the size of the domestic market alone (which is nearly 2 million vehicles), and comparable to U.S. production (of 10.4 million vehicles) on a per capita basis. Even so, U.S. Trade Representative Greer made it amply clear in media interviews this week that the Administration expects Canada to accept meaningful base tariffs as a part of any renewal of the USMCA.

Canada’s Q4 GDP results revealed a 0.6% annualized decline, below expectations and the second quarterly drop in 2025. While overall GDP did manage to scratch out 1.7% growth for the full year, it got a big helping hand from government spending (which contributed nearly half a point to GDP). Besides the public sector, the other major pillar of support for the economy amid last year’s trade trauma was the consumer. Despite very weak consumer confidence and a big slowdown in population growth, real consumption managed to rise 2.3% last year, a tad firmer than the prior two years (both 2.2%). Lower interest rates and a variety of tax relief measures helped, and the upswing in domestic travel also provided important support. The sturdy spending trends look sustainable, as the household saving rate averaged 4.9% in 2025, almost unchanged from the prior year.

Even as the Canadian economy remains challenged by relentless trade uncertainty, the TSX continues to find its own path. Prior to a Friday stumble, the index managed to rise more than 1% this week to hit an all-time high above 34,500 and up 8% in the first two months of the year. A rebound in gold and firmer oil prices assisted, but Q1 bank earnings were also greeted favourably. Economy-wide profits rose more than 6% in 2025, topping nominal GDP growth of 4.3% on the year. More broadly, Canada may be benefitting from a diversification push away from U.S. markets, where valuations are rich.

Just as one small sample of that shift into Canada in the past year was a welcome swing in Foreign Direct Investment (FDI) into a rare surplus. For Q4 alone, quarterly net FDI inflows were $11.6 billion, driven by M&A activity. Looking at the four-quarter trend reveals that for the first time in more than a decade, and only the second time in the past 18 years, Canada had a net inflow in FDI in 2025 (of $17.3 billion). For perspective, that alone would have funded more than half of the current account deficit (of $30.4 billion) last year. There are three major types of FDI: M&A, greenfield investments, and reinvested earnings. In 2025, the latter remained in a large outflow position of $47 billion (and is normally in a deficit because of Canada’s large stock of outstanding investments abroad), while M&A was in a large offsetting surplus. Net new FDI investments were thus in a surplus of $17.6 billion for the year, which is encouraging news for an economy looking for new growth avenues.

Overall, investors may be breathing a bit of a sigh of relief that the Supreme Court decision has come in as expected, and that the administration has also reacted in line with expectation – that is to say, acting unexpectedly.

More broadly, the tariff narrative represents only a small piece of the overall macroeconomic backdrop. The good news is that we continue to see U.S. economic growth that is positive and growing in line with trend levels, and corporate earnings that are on pace for strong double‑digit growth in 2026. In this environment, we recommend staying diversified and staying invested, and tuning out headlines that are noisy but do not meaningfully impact the macroeconomic picture.

Source: BMO Economics Talking Points: Tariffs: The Plan, The Courts, The Sequel

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.