Goodbye Summer; Hello Pumpkin Spice World.

DHL Wealth Advisory - Aug 29, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

As we begrudgingly say goodbye to the final week of summer, we thought it would be helpful to highlight some key observations and trends in the market that we have been discussing with clients or that we believe have been flying under the radar...

As we begrudgingly say goodbye to the final week of summer, we thought it would be helpful to highlight some key observations and trends in the market that we have been discussing with clients or that we believe have been flying under the radar of investors as there seems to be an inordinate amount of attention paid to index-level performance, in our view.

Global markets, but most notably, US stocks have staged an impressive rally from the tariff-induced sell-off earlier in the year with latest levels near record highs. August just marked the fourth consecutive month of gains. However, with valuation now extended from a historical perspective, sentiment has seemingly shifted more negative in recent weeks following a few not-so-great economic reports with more investors questioning the sustainability of stock market momentum particularly since the perception is that only a handful of mega-cap stocks have been driving the recent gains.

To be clear, we remain firmly in the “this remains a bull market” camp from both a cyclical and secular perspective. Nonetheless, we are attempting to address some of these concerns. First, market breadth or participation is not nearly as narrow as some have suggested. Second, more passive investment strategies have certainly had a great run given index-level performance, but fundamental dispersion levels remain elevated suggesting to us that investors should be choosier within their stock selection. Finally, given elevated valuation levels we believe that valuation-weary investors could potentially benefit by focusing on some “forgotten” areas of the market and for us the most obvious is the small-to-mid-cap space (SMID).

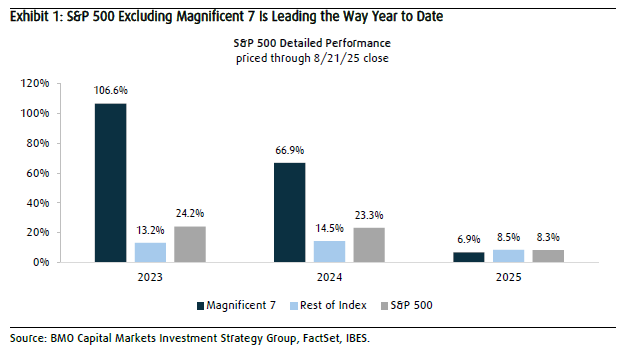

It is no secret that the so-called Magnificent-7 stocks have been the driving force behind market gains for much of the past two+ years and this has led to concentration worries amongst investors given the bloated valuations of some of these stocks. However, an interesting development has occurred alongside the most recent market rebound this year. Year to date, these seven stocks have underperformed the rest of the index by about 1.5%, and assuming this trend holds throughout the year, it would be the first calendar year during this bull market where the rest of the index outperformed (Exhibit 1).

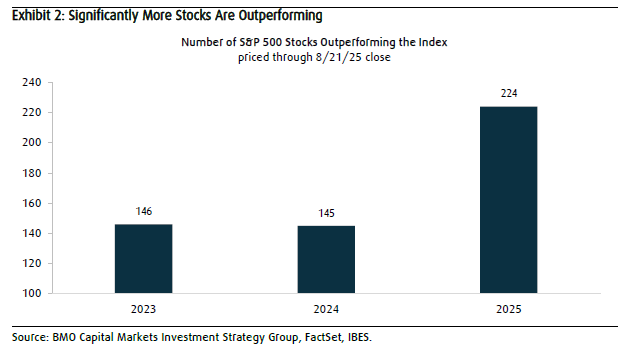

And this is something we find reassuring since the S&P 500 is around records again without this segment leading the way and is a significant departure from 2023-24. In addition, participation levels have also improved dramatically this year as roughly 45% of S&P 500 stocks have outperformed the broader index compared to about 29% for the prior two calendar years (Exhibit 2).

Elsewhere, Friday we had Canadian Q2 GDP that showed the Canadian economy contracted at an annualized rate of 1.6% in Q2, deeper than expected, but just a tick below the Bank of Canada’s -1.5% projection. The trade war took a huge toll on trade in the quarter, with net exports slashing 8.1% from growth, the second most on record (only the pandemic was worse). That was driven by a 26.8% dive in exports, while imports slipped a lesser 5.1%. The uncertain backdrop also weighed heavily on business investment, with machinery & equipment spending plunging 32.6% the fourth-largest decline on record.

It wasn't all bad news, as the rest of the domestic economy was firmer. Household spending rebounded, up 4.5% while government spending/investment added notably to growth as well. Residential investment was also firm at +6.3%. Final domestic demand rose 3.5% annualized, reflecting the resilience and perhaps Canadians' bias to buy/travel domestically.

For the BoC, there's nothing here screaming for a September cut, though it will certainly keep the chatter around further easing intact. The Bank had Q2 GDP at -1.5%, so the miss was minor. And, the strength in domestic demand highlights the economy's resilience. One negative is that Q3 is tracking softer than their +1% estimate (closer to +0.5%), but it's still very early, and things can change materially.

Key Takeaway: It should come as no surprise that the Canadian economy struggled in Q2 as tariffs ramped up. However, the domestic strength is somewhat comforting, although the sustainability of that momentum is an open question. Arguably, the economy is evolving largely in line with the BoC's July forecast. Policymakers opted to stay on hold then, so this report likely doesn't push them any closer to cutting in September, with the labour and inflation data still to come.

After a strong rally in the stock market, with the S&P 500 and Canadian TSX now up over 25% since the April 8 lows, we believe some consolidation are likely in the weeks ahead. This comes as we move toward the seasonally choppier months of September and October, and as inflation may move higher and economic data may soften in the coming quarters.

However, historically, we also know it’s normal to experience two to three pullbacks in the market in any given year, especially in years with elevated uncertainty. And we see any coming bouts of volatility as opportunities for investors to diversify and to add quality investments at better prices. We believe this is especially true now that we appear to have more meaningful catalysts in place, including a Fed that seems more willing to shift policy rates lower, and a Bank of Canada that also may continue cutting interest rates.

Sources: BMO Capital Markets US Strategy Comment Pictures to Ponder as Summer Winds Down, BMO Economics EconoFACTS: Cdn. Real GDP (Q2, June) — Trade War Takes a Toll

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.