Enter Stage Left; Tariffs on Forest Fires.

DHL Wealth Advisory - Jul 10, 2025

North American markets spent the week flirting with new all-time-highs on Thursday as investor attention continues to focus around politics to the South...

North American markets spent the week flirting with new all-time-highs on Thursday as investor attention continues to focus around politics to the South. The first half of 2025 was marked by policy uncertainty, as the U.S. announced sweeping tariffs in early April that threatened to raise the effective tariff rate from 2.3% at the end of 2024 to over 25%, fueling recession concerns.

A subsequent easing of trade tensions has left the effective tariff rate at approximately 15% (likely between 5% - 10% on imports from Canada. Encouragingly last week, the U.S. reached an agreement with Vietnam, reducing the tariff rate to 20% (40% on goods that are shipped but that don't originate from Vietnam), down from the 46% announced in early April. Additionally, U.S.-Canada trade talks are progressing following the Canadian government's decision last week to drop the U.S. digital service tax.

Although U.S. tariff rates have declined from their peak levels, they remain a central focus of the U.S. administration's agenda and are poised to rise significantly compared with previous years. In fact, this week we saw Trump’s tariff letters go out to a number of countries. However, these countries are generally insignificant from percent of trade perspective. The recent “tariff letters” (if enacted) would take global trade policy part of the way back to the chaotic days of early April. However, the evidence so far points to previously announced tariffs not quite living up to their initial billing.

Through May of this year, the calculated tariff rate (customs duties as a share of imports) reached 8.8%—much lower than expectations of over 25% before the May 12th deal with China. Whether the delayed impact is a result of tariff affected goods not yet making their way to shelves or companies postponing price increases in the hopes that tariffs are later rolled back, it has meant a more muted effect on the U.S. economy (i.e, firmer growth, less inflation).

Meanwhile, Canada also appears to be getting off easier than expected, as the calculated tariff rate on Canadian exports to the U.S. fell to 1.9% in May (from 2.3% in April). The decrease is largely attributable to finished motor vehicles seemingly avoiding auto tariffs, as calculated tariffs on that category fell to less than 0.1% in May (from 2.9% in April). But levies on Canada are likely headed higher because of potential copper tariffs and the 50% tariffs already in effect on steel and aluminum.

The upshot, in our view, is that U.S. economic data has proven resilient, supported by a healthy, albeit easing, labour market. This resilience was on display in last week's jobs data, with nonfarm payrolls rising by 147,000 in June, above expectations for a 118,000 gain. Additionally, the unemployment rate fell to 4.1%, while initial jobless claims fell to a six-week low of 233,000.

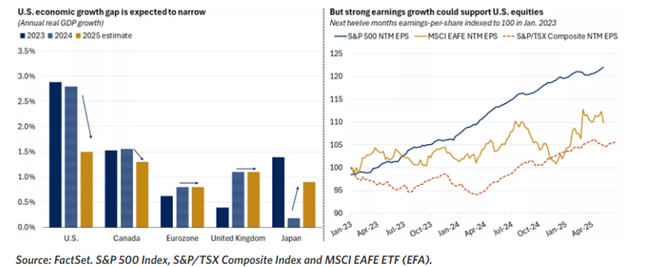

Meanwhile, US markets have played catch-up to international markets in recent weeks. Since 2010, U.S. economic growth has outpaced most developed markets, contributing to U.S. equity outperformance versus overseas in 12 of the past 15 years. However, this trend reversed in the first half of 2025, with overseas stocks—particularly in Europe—leading gains. Expansionary fiscal policy in Germany and deeper rate cuts by the European Central Bank have helped boost European equities and lift regional growth expectations.

Despite a narrowing gap in economic growth, U.S. corporate profits are expected to continue outpacing those of Canadian and overseas peers. We anticipate stronger U.S. profit growth ahead, likely bolstered by AI tailwinds and a more accommodative policy environment.

The strong performance from overseas stocks in the first half highlights the importance of maintaining strategic allocations to overseas investments as part of a well-diversified portfolio. In the near term, however, it appears that strong momentum and improving investor sentiment suggests greater opportunity lies in U.S. markets versus overseas, so we continue to recommend maintaining a weighting towards U.S. stocks.

Sources:BMO Economics AM Charts: July 9, 2025, BMO Economics AM Charts: July 10, 2025

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.