Sp-OILER Alert. This Time Will Be Different.

DHL Wealth Advisory - May 30, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Markets were back to their winning way this week having just completed the strongest month since November 2023...

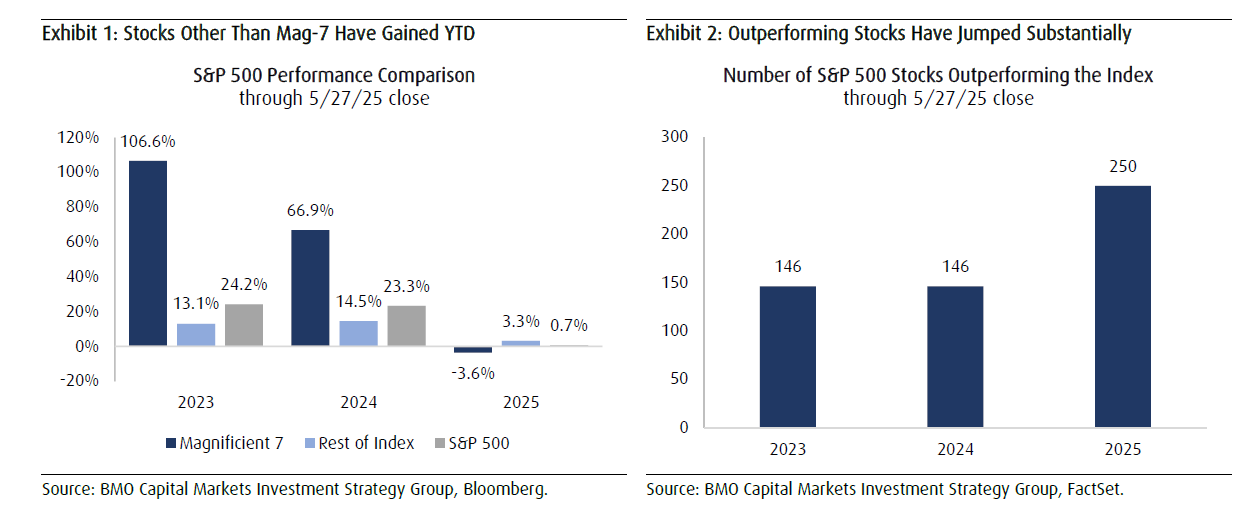

Markets were back to their winning way this week having just completed the strongest month since November 2023. Given all the uncertainty related to trade policy and its potential macroeconomic impact, we believe most investors have been solely focused on overall index performance as the “on-and-off again” nature of the headlines stemming from these developments have whipsawed the S&P 500 over the past two or so months. Indeed, after having one of its deepest corrections in years and one of its strongest correction rebounds, the index is barely positive for the year.

However, we have always contended that the US market is a “market of stocks” with opportunities available in all types of market conditions and this time has proved to be no different. Unfortunately, given all the “macro” focus many investors appear to be either missing or ignoring some key beneath-the-surface trends that we believe strongly favor a highly selective investment approach for the US market. Most notably, 2025 market performance trends have undergone a significant shift compared to the prior two calendar years as participation levels have jumped quite substantially with roughly half of S&P 500 stocks outperforming YTD. In other words, significantly more stock picking opportunities have emerged this year despite near-zero overall market returns.

It is no secret that the so-called magnificent seven stocks have been the driving force behind market performance ever since this bull market began in late 2022, and this has led to concentration worries amongst investors given the bloated valuations of some of these stocks, particularly since a few have been among the worst 2025 performers. However, 2025 market performance excluding these stocks has been significantly better. For instance, the rest of the S&P 500 has gained 3.3% compared to a loss of 3.6% for the magnificent seven stocks YTD (Exhibit 1). This is something that we find reassuring because the overall market has held up relatively well despite the poor performance of these behemoths. Translation: many more stocks within the index are picking up the slack and lessening the previously outsized influence of these largest stocks. Looked at in a different way, half of S&P 500 stocks are outperforming so far this year, which is an increase of over 100 stocks (or 20% of the index) compared to the prior two calendar years (Exhibit 2). We believe these trends, should they continue as we expect, are an ideal environment for stock pickers.

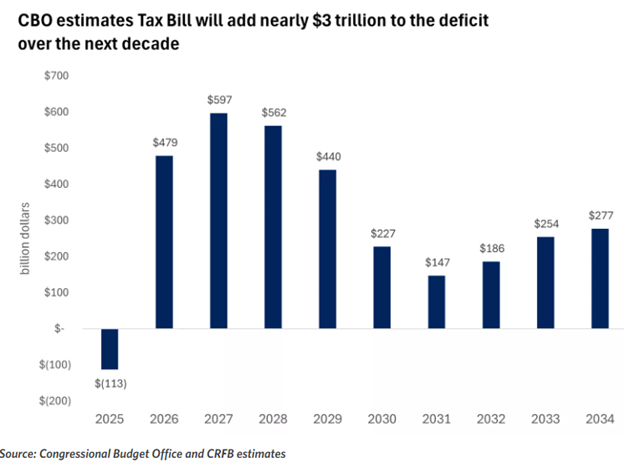

Elsewhere, last week the U.S. House passed Trump’s Big (Huge) Beautiful Tax Bill by one vote, the narrowest of margins. The bill primarily extends the 2017 current tax cuts and includes additional proposals that were highlighted during the Trump campaign. To help cover the cost of the tax proposals, the draft bill included several provisions to raise revenue, When netting out the tax cuts, new spending, revenue provisions, and additional interest-rate cost, the Congressional Budget Office estimates that the bill would add nearly $3 trillion to the U.S. budget deficit over the next decade.

Many of the tax cuts are front-loaded, designed to be in force from 2025 to 2028, while and the spending cuts are backloaded, likely pushing the deficit to 7% of GDP in the next two years. The likely increasing deficit is mathematically a positive from an economic standpoint, adding to GDP, though its impact is likely to be partly offset by the drag from tariffs. We expect a modestly stimulative fiscal policy supporting growth but also feeding into deficit concerns. However, we would highlight that the final bill could look very different than the House version that was just passed. This is likely the start of a long process, with Congress setting a goal of a final bill signed into law on July 4.

The reason we bring this up is that Canadians should pay close attention to this one. The far-reaching bill includes a section that could impact the withholding tax applied to dividends paid to Canadians by U.S. corporations. While the proposed bill may still change as it moves through the Senate, it is worth keeping an eye on. The U.S. bill proposes tax changes to countries it deems to impose unfair foreign taxes on its people and businesses. The bill would authorize the U.S. Treasury Secretary to designate these countries as a "discriminatory foreign country". Under that designation, the U.S. can choose to enact changes to previously established withholding tax rates on U.S. source income, overriding the tax treaty that’s been in place since 1942. Dividends, interest and royalties received from U.S. companies could see the withholding tax rate increased to as high as 50% in as little as four years.

Canada may be particularly at risk of becoming designated as discriminatory in part because of the digital services tax (DST) that was introduced in June 2024. The DST applies a rate of 3% on revenue earned from certain digital services that rely on engagement, data, and content contributions of Canadian users and certain sales or licensing of Canadian user data.

Canadian corporations that receive dividends from U.S. subsidiaries are currently subject to a 5% withholding rate under the existing treaty. If the proposed changes go through, this tax rate would increase by 5% per year until it reaches 20% above the current statutory rate of 30%. Because the final bill could look very different than the initial drafts, we do not recommend taking any actions at the moment.

Source: BMO Capital Markets US Strategy Comment: Checking in on GARP

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.