And to Think He Still Managed a Few Rounds of Golf...

DHL Wealth Advisory - Jan 24, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

At the time of writing, in the past 100 hours we have had the freshly-minted President threaten to impose tariffs for various ‘transgressions’ on the EU, China, Russia, and of course Canada and Mexico...

At the time of writing, in the past 100 hours we have had the freshly-minted President threaten to impose tariffs for various ‘transgressions’ on the EU, China, Russia, and of course Canada and Mexico, as well as any other country that sells into the U.S. market; demand that the Fed and every other central bank bring down interest rates forthwith; cajole OPEC to lower oil prices with haste; pull the U.S. out of the Paris Agreement; yank U.S. funding for the World Health Organization; axe the EV mandate; curtail immigration; and introduce the $500 billion Stargate plan. And how have markets responded to this whirlwind of news?

Source: All Tariffs, All The Time

…Markets have delivered positive equity returns, and yes, in Canada too. In fact, the US market is heading for its best start for a new US president since Ronald Reagan was sworn in to power in 1985.

Source: S&P 500 Sees Best Start for a President Since 1985: Markets Wrap - Bloomberg

As much as markets would prefer to look past the President’s pronouncements, at least until proposals are actually enacted, it seems they have little choice but to follow the bouncing ball. For example, the U.S. dollar fell heavily on Inauguration Day, as tariffs received only light mention in the speech, while Canada and Mexico were initially spared. However, before the day was out, the President said that “maybe” those 25% tariffs would be in place for the NAFTA partners by February 1—and down went the loonie. Meanwhile, broader tariffs on others will be studied until April 1 (yes, April Fool’s day). In the middle of this, Russia was threatened with additional sanctions, as well as tariffs, if it didn’t soon end the Ukraine conflict. In other words, and just to be clear, Russia could very well face the same harsh trade treatment as Canada. Note that U.S. imports from Russia totalled all of $3 billion in the past 12 months (down 90% from 2021), while imports from Canada were $410 billion over the same period—none of which the U.S. apparently needs, per the President to folks at Davos on Thursday.

Source: All Tariffs, All The Time

We suggested in recent weeks that there is a great deal of debate among analysts and economists over the degree of inflationary risk for the U.S. economy from tariffs. This uncertainty is expected to push the US Fed to the sidelines at next Wednesday’s interest rate decision. Despite the President’s considered advice, rates are expected to stay on hold for a few months - markets are still only looking for 1-2 cuts for all of 2025. This week’s thin slate of economic data did little to move the needle, with home sales defrosting, but jobless claims rising and consumer sentiment softening somewhat in January.

Source: All Tariffs, All The Time

It’s a very, very different set of calculations confronting the Bank of Canada, as they too will decide on rates on Wednesday. (Repeating, this overlap of BoC and Fed rate decisions will happen five times this year; the other four are all the dates in the second half of 2025.) While the tariff threat is of some academic interest in the U.S., it is an existential risk to Canada. Thus, in direct contrast to the Fed, the BoC is widely expected to trim rates again by 25 bps to 3.0%. True, it’s not a total lock, job growth has somehow sprung back to life. This week’s Canadian inflation data was mostly as expected, with the headline 1.8% inflation rate among the lowest in the industrialized world—Japan’s rate is now double that!

Source: All Tariffs, All The Time

Meanwhile, BMO’s Chief Investment Office Brian Belski put out an interesting piece this week on the ongoing tariff rhetoric. His view on US/Canada trade consternation has remained consistent since his December publication (Trade Concerns = Control What You Can Control). Yes, from his perspective, the tariff threats were clearly just the opening volley of the USMCA renegotiations Trump campaigned on – thereby eliciting the intended reaction - and more importantly (in his view), revealing significant information surrounding renegotiations.

Source: Focus on Fundamentals Over Trade Noise

While a 25% broad tariff on the United States’ two largest trading partners is even more unlikely now, he continues to believe some form of targeted tariffs could be imposed over the next several months, barring significant action and concessions by Canada. Overall, he believes, just like what happened in 2018, common sense will ultimately prevail and the USMCA will be renegotiated with the result generating a relatively minor impact on Canadian equities.

Source: Focus on Fundamentals Over Trade Noise

Indeed, investors should control what they can control and focus on the normalization process that is occurring and will continue to occur in 2025. Belski believes Canadian economic growth is ultimately tied to US growth and will continue to converge with the US in 2025 – a view that has not changed. YES, while this could add some volatility, Belski continues to believe the strong relative value and improving growth profile of the TSX means Canada can still outperform in 2025, despite persistent trade noise.

Source: Focus on Fundamentals Over Trade Noise

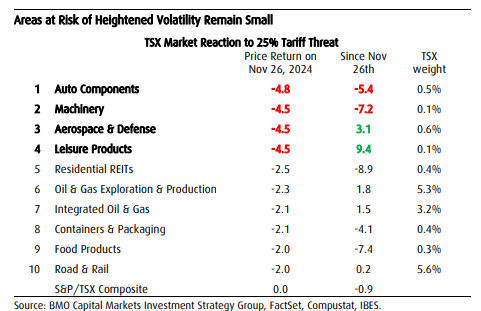

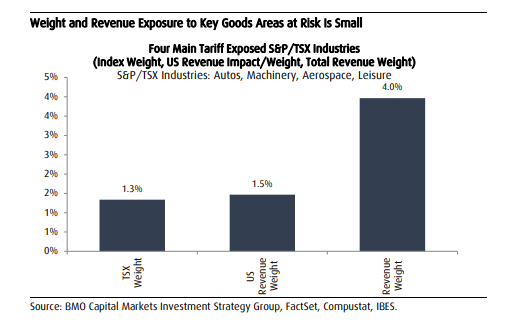

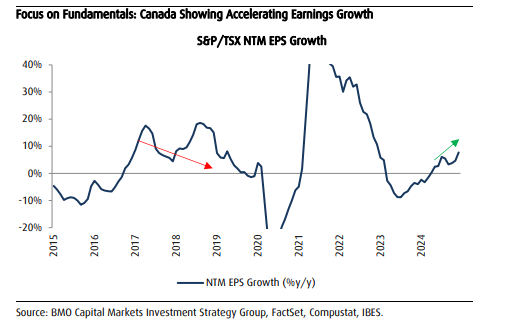

Focus on Fundamentals:

- Key Goods Producing Areas at Risk in the TSX are Small Weight (1.3% of TSX), and Limited US Revenue Risk (1.5% of TSX)

Source: Focus on Fundamentals Over Trade Noise

- Earnings. The TSX is seeing an acceleration in earnings momentum and increasing valuations

Source: Focus on Fundamentals Over Trade Noise

In fact, here’s a Friday Factoid for you: Canada’s TSX close on November 25, just prior to the first threat of 25% tariffs: 25,410. Two months later, at Thursday’s close? 25434 (up 0.1%, or essentially unchanged). This resiliency in the face of the tariff threat reflects the following: a) global markets have rebounded mightily; b) the TSX is not a good reflection of the Canadian economy, given its massive weightings in financials, energy and materials; and c) investors may just not take the tariff threat as anything more than a negotiating stance. A Wall Street Journal article this week suggested as much, citing the threat as a way to quickly re-open USMCA negotiations… since denied by the President. Fake News, of course.

Source: All Tariffs, All The Time

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.