Tarrifying?

DHL Wealth Advisory - Dec 06, 2024

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Equity markets rallied on this week wasting no time embracing the notion of a Santa Claus rally. What hasn’t welcomed the holiday season, or perhaps simply embraced an inner Grinchn mentality...

Equity markets rallied on this week wasting no time embracing the notion of a Santa Claus rally. What hasn’t welcomed the holiday season, or perhaps simply embraced an inner Grinchn mentality, has been the relationship amongst North America’s trading partners. More specifically USMCA or NAFTA 2.0. …And just when you thought we were done talking about US Politics…

During the recent U.S. election campaign, the topic of Canada came up all of once as far as we can discern in the months and months of rhetoric and debate, and that once was about water. There was never a mention of singling out America’s largest export market with any specific trade action, or about spiking the USMCA. Accordingly, the sudden threat by the incoming President that Canada and Mexico could face a whopping 25% tariff on all products on day 1 of the new Administration next January was a shock—even if the protectionist leaning was of little surprise. Previously, the biggest question was over whether Canada would even be subject to the proposed broad 10% import tax. Coming like a bolt from the blue, the remark last week initially battered the Canadian dollar and the Mexican peso, and spurred a thousand headlines, not to mention even more recriminations.

Source: BMO Economics Talking Points: Tariffying

However, it didn’t take long for the equity market to shrug off the initial reaction with the Canadian TSX closing out today hitting an all-time-high.

Not to make light of an incredibly serious situation, but it was almost as if the markets went through six stages of grief in less than six days:

Source: BMO Economics Talking Points: Tariffying

- Denial and shock: “25%? He must mean China, not Canada! This can’t be true.”

- Pain: “What have we done to deserve this? Sell the Canadian dollar, sell export-dependent stocks, sell the automakers.”

- Anger: “What kind of friend does this? What about the USMCA; didn’t he sign that? We won’t stand for this, we’ll retaliate. U.S. consumers are going to pay the price.”

- Bargaining: “What is it that he wants? Border security… sure, that’s good for us too. A crackdown on drugs… sure all for that too. Surely, we can come to some agreement. Look even Mexico’s President Sheinbaum had a ‘wonderful conversation’ with him. We can work this out.”

- Depression: “Gosh, even if we can avoid this 25% tariff, we could face something similar on any other perceived misstep. We may never have unfettered access to the U.S. market. This is going to depress business investment for years.”

- Acceptance: “We’re just going to have to learn to live with this persistent noise and uncertainty and focus on what we can control for the next four years

Source: BMO Economics Talking Points: Tariffying

The generally mild net reaction by financial markets—to wit, the peso is currently stronger than it was a week ago—suggests that almost no one believes that the 25% tariffs will actually be enacted. We are not involved in the political arena, so will not opine on the validity of the threat, but regardless of what economists and analysts believe, it is quite obvious that the President-elect views tariffs as some kind of magic economic elixir, which only causes good for the U.S. economy, and any pain is for others to absorb.

Source: BMO Economics Talking Points: Tariffying

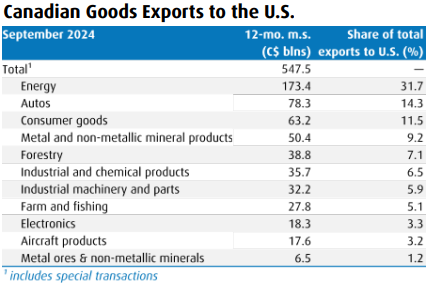

Why are pundits generally aligned in the belief this is more a tactic than a real threat? At the industry level, energy exports were C$173 billion in the latest twelve months, or nearly a third of Canadian goods exports to the U.S. That is the largest share of exports by a wide margin. But, one has to question the legitimacy of tariff threats on Canadian energy, when there are few obvious near-term alternatives to more than 3 million barrels per day of imports on the U.S. side. The immediate impact would be higher oil and consumer gas prices. Autos are another difficult case where various parts cross the border multiple times before ending up in a finished product. There would be a massive amount of pushback at the industry level given this heavy-duty infrastructure is not portable.

Source: U.S. Tariffs against Canada: The Latest Threat

Source: Where is Canadian Trade Most Exposed?

It is likely the initial impact would be higher prices in the U.S. for a whole host of products. BMO’s economic team estimates this could push up U.S. core PCE inflation by nearly a percentage point over the baseline forecast by the end of 2025. This would likely mean higher short-term and long-term Treasury interest rates than previously forecast and somewhat slower U.S. GDP growth as consumers and businesses cope with the double whammy of rising prices and higher financing costs.

Source: The Potential U.S. Implications of the New Tariff Threats

However, BMO’s Chief Economist Douglas Porter did some analysis on the “What if”… Well, IF 25% tariffs were levied across the board, there are policy levers and market responses that could somewhat mitigate the blow.First, the Canadian dollar would act as a partial shock-absorber, and its initial drop was a taste of what could come. In a full-25% world, with limited retaliation, a 5-10% further depreciation in the currency is entirely fathomable. At around $1.50/US$ (or 66.7 cents), the exchange rate could lessen the revenue blow for domestic producers.

Source: BMO Economics Talking Points: Tariffying

Second, the Bank of Canada would likely lean to even lower interest rates, essentially to support the parts of the economy it can support—i.e., domestic spending. We had been expecting the Bank to take its overnight rate down to 2.5% (from 3.75% now), but a 1.5% terminal rate, or even lower, would be more likely in a tariff scenario. Clearly, this is not an ideal situation for the Bank, as it risks inflating the housing market again, and firing up consumer borrowing. But desperate times…

Source: BMO Economics Talking Points: Tariffying

Third, fiscal policy would almost certainly loosen up further to provide support for the economy, if not to also meet demands on the defence spending front. Ottawa’s anchor of $40 billion budget deficits, and moving to less than 1% of GDP, already looked to have been cut free. And, a 25% tariff world would justify a change in stance… “desperate times” again. Roughly speaking, a fiscal loosening of around 0.5% of GDP (or about $15 billion) would not be out of the range of possibilities.

Source: BMO Economics Talking Points: Tariffying

Fourth, and perhaps a bit more on the dreamy side, individual Canadians may choose to spend more at home and aim for domestic producers, egged on by a much weaker currency.

Source: BMO Economics Talking Points: Tariffying

Taking all these mitigants into account, the damage could be limited to around 1% of GDP, at least in the first year. All that said, we defer to the more educated minds in the field of international trade and seemingly the vast majority of analysts and commentators who appear to believe that the tariffs won’t actually happen, that it is all bluster, and/or a negotiating tactic. To put it more poetically, it begs the question, is: “it is a tale told by an … President… , full of sound and fury, signifying nothing.”

Source: BMO Economics Talking Points: Tariffying

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.