Almost That Time of Year.. In-law Visits, and Eggnog. Lots and lots of Eggnog...

DHL Wealth Advisory - Nov 22, 2024

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

North American markets were mixed on the week with Canada’s S&P TSX hitting fresh all-time-highs, while our neighbours to the South were also in the green, but failed to reclaim record territory – granted, it’s only been a week...

North American markets were mixed on the week with Canada’s S&P TSX hitting fresh all-time-highs, while our neighbours to the South were also in the green, but failed to reclaim record territory – granted, it’s only been a week. There wasn’t a whole lot moving markets this week as we wind down yet another corporate earnings seasons that continues to show the resiliency of consumers. There was a bit more action going on in Canada this week where we saw inflation numbers come in slightly ahead of expectations.

Canadian consumer prices rose 0.4% in October, bumping up the annual inflation to 2.0% from 1.6% the prior month. The back-up is no big surprise, as the combination of higher gasoline prices, a meaty annual rise in property taxes, and a tough comparable from a year ago prompted the temporary rise. Still, the report is a bit hotter than anticipated, with both of the Bank of Canada's main measures of core inflation pushing up by two ticks on a yearly basis—trim to 2.6% and median to 2.5%, with the three month paces a bit warmer still. On a seasonally adjusted basis, the report rained +0.3% m/m increases, with headline, food, and both major core metrics rising at that clip; while not overly concerning, that's also far from soothing. We will note that 7 of the 10 provinces are still reporting headline inflation rates with a 1-handle; unfortunately, the three that are above that key level are among the four largest provinces in the country.

Source: Canadian CPI: Wickedly Defying Gravity

Property taxes were always going to be a big part of this report, as the October release captures the average annual increase—this year weighed in at a hefty 6 pounds (or 6.0%), the largest since 1992 and compared with a 4.9% rise a year ago. An average property tax increase over the prior 30 years was 2.5%—that difference adds about 1 tick to overall inflation.

Source: Canadian CPI: Wickedly Defying Gravity

Bottom Line: This heavy result should take some more steam out of the call for another 50 bp rate cut from the Bank of Canada in December. We have been in the 25 bp camp from the start and this report only reinforces that expectation, along with evidence that housing is stirring, the Fed will turn more cautious, and a limping loonie. There are still the important Q3 GDP (next Friday) and jobs reports (following Friday) ahead of the next rate decision on December 11. At this point, most signs suggest the prudent course of action is a 25 bp rate cut path.

Source: Canadian CPI: Wickedly Defying Gravity

Meanwhile, BMO Chief Market Strategist Brian Belski published his 2025 Market Outlook this week, so we thought it would be a helpful to review some of his key points. To sum it up: Bull Market Is Alive and Well in 2025, Despite Likelihood of More Mooted Returns. His S&P 500 goes from 6,100 to 6,700.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

Diving into things a bit more, Belski’s overarching investment strategy that has been in place since 2009 remains resolutely bullish – US stocks are in the midst a 20–25-year secular bull market. Spawned from the ashes of the great financial crisis, this secular bull has exhibited several different spurts (cyclical bulls), not to mention its fair share of bumps and bruises (two cyclical bears: 2020 and 2022, and close to a third: 2011). After all, US stocks have averaged an annual return of 14% since 2009. Moreover, the “up” cycles have decidedly skewed not only returns, but also duration relative to negative periods since 2009.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

For instance, when looking at all rolling monthly one-year periods since 2009, positive returns were achieved nearly 85% of the time with an average gain of more than 16%. By contrast, the 15% of negative periods had an average loss of roughly 6%. Thus, it has been correct to own stocks. After all, we are investors – not market timers and as such not infatuated or fixated on making market calls. Unfortunately, much of the herd and bate-click headlines prognosticate the end of this bull market or downright emphatically attempting to nullify periods of stock strength.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

While it is impossible to know exactly how long this bull market will last, we can look at history to give us some guidance. The average S&P 500 bull market over the past 50 years has lasted an average of roughly 6 years, with the longest being 11 years (3/9/2009 - 2/19/2020) and the shortest being 1.9 years (3/23/20 – 1/3/22) according to his analysis (Exhibit 4). In fact, all bull markets except for the pandemic rebound made it to a third year, suggesting there is plenty of room for US stocks to run from current levels considering stocks just hit their two-year bull market mark last month. However, it is also worth noting that even despite his continued optimism, historical data shows that the third year of bull markets has produced the lowest average returns (Exhibit 5). However, two bull markets managed to produce double-digit gains during their third year, and only one saw third-year losses, the 1974 bull market, which was triggered by the fallout from the oil embargo (Exhibit 3). In fact, if the anomalous 1974 period is excluded, his current outlook matches almost perfectly to historical performance patterns.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

It is no secret that some of the largest stocks have been the driving force behind market gains for much of the past two years and this has led to concentration worries amongst investors given the bloated valuations of some of these stocks. However, an interesting development has occurred during 2H. The S&P 100 index (or the largest 100 S&P 500 stocks) has underperformed the rest of the index for the first time since late 2022 when the bull market began and is something Belski finds reassuring since the S&P 500 has hit a series of new records without this segment of the market leading the way. Similarly, participation levels have also improved dramatically since 2H started as 276 S&P 500 stocks have outperformed the broader index – by far the highest semi-annual level of this bull market and more than 15% above its 10-year average. Belski believes these trends, should they continue as he expects, represent an ideal environment for stock pickers.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

However, it now appears to be a time for some common sense and prudency, and yes – humility. Given that 2023 successfully reversed an oversold cyclical bear market from 2022, while 2024 rewarded easing inflation, steady economic growth, a resilient employment back drop, and a US Federal Reserve that is entering an accommodative phase – it is clearly time for markets to take somewhat of a breather. Bull markets can, will, and should slow their pace from time to time, a period of digestion that in turn only accentuates the health of the underlying secular bull. So, he believes 2025 will likely be defined by a more normalized return environment with more balanced performance across sectors, sizes, and styles.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

So, what does this mean from an investment perspective? In a simple sense, he continues to believe investors will need to own a little bit of “everything” and not tilt too far in one direction or another from a sector, style, and size perspective. However, this should not be interpreted as a recommendation to be more passive when making decisions – to the contrary, he believe active investment strategies will be even more important next year as many of the largest stocks that drove performance within sectors are unlikely to maintain that momentum in 2025, forcing investors to search for other opportunities further down the market cap spectrum.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

Belski maintains his overweight sector opinions for Financials and Technology. Indeed, these have been two of the best performers in 2024 and based on the fundamental underpinnings for both, he would expect these trends to continue during 2025. Yes, Technology is probably the poster child for concentration risk, but it is important to remember that the sector includes 69 stocks across seven industries and a deeper dive shows there are plenty of areas within the sector apart from the highest profile names expected to deliver significant earnings growth and at much more reasonable valuations.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

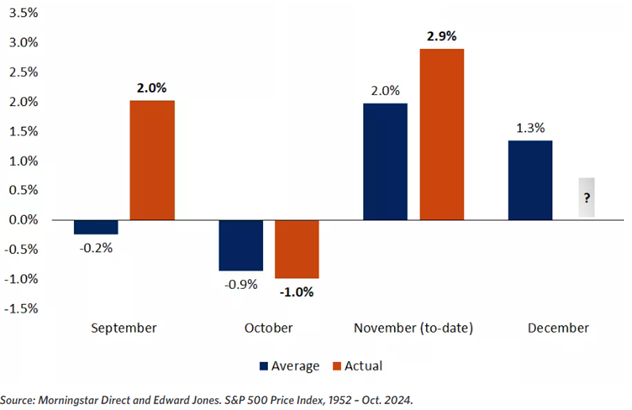

Next week we will revisit Belski’s 2025 outlook for Canada, but let’s not quite call it a close on 2024. Afterall, we are now entering a seasonally stronger time of year for markets. Especially in U.S. election years, November and December historically have been positive months in the markets, and momentum may resume in the weeks ahead. Just take a look at the below chart that illustrates the average S&P500 returns for the final 4 months of the year.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.