Loonie Tunes, Indeed.

DHL Wealth Advisory - Nov 15, 2024

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

The dust is settling on last weeks landslide Presidential election with markets learning that Republicans are now in control of the Presidency, Senate, and the House of Representatives...

The dust is settling on last weeks landslide Presidential election with markets learning that Republicans are now in control of the Presidency, Senate, and the House of Representatives. At this point it is unclear how many of the campaign proposals may result in actual policy, over what time frame, and what their impact would be. But what we do have some confidence in is that the fundamental conditions that drive long-term market performance remain more favourable than hurtful.

- The economy has consistently defied expectations for a recession over the last two years, even expanding at an above-average pace, driven by robust consumer spending. While a moderate slowdown is likely, several indicators remain strong, including rising incomes, stable employment, healthy household finances, and improving loan growth.

- Corporate profits are on the rise, supporting a positive outlook for stocks. S&P 500 earnings growth is projected to accelerate from 0.5% in 2023 to 9% this year and 14% in 2025. Though next year's estimates may be a bit optimistic, the upward trajectory can help sustain the bull market, which has now entered its third year.

- Interest rates have likely peaked and are gradually moving lower. The Fed is cutting rates, not in response to an economic downturn, but because of an improvement in inflation, keeping the chances of a soft landing alive.

In our view, the tried-and-tested message over time - don't play politics with your portfolio - continues to hold true. Centuries of data will show that major economic trends that were in place before the election are likely to continue, and investors may want to avoid the urge to change strategies or portfolios because of the election. U.S. companies will be able to adapt to different policies as they have done successfully in the past, and global forces will continue to exert outsized influence.

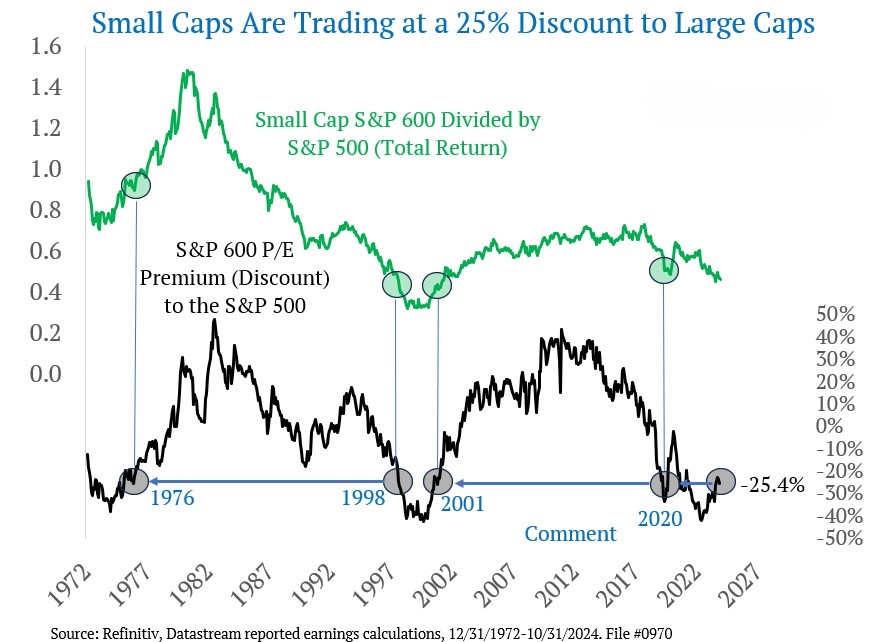

That said, the potential for tax cuts (personal and corporate) and deregulation may provide an additional tailwind to the theme of broadening market leadership, which has started to take shape since the start of the third quarter. Value-style investments and cyclical sectors, along with small- and mid-caps, have been left behind since the start of the bull market in October 2022 and have room to catch up as the rally broadens. Afterall, the P/E discount in Small Caps versus Large Caps is akin to observations made at the turn of the century. The S&P 600 is trading 25.4% cheaper than the S&P 500. We find this valuation relationship in 1976, 1998, 2001 and 2020.

In isolation, the potential policy shifts are seemingly positive for equities but negative for bonds. The red wave Republican sweep may bring fiscal concerns back to the forefront amid growing deficits and elevated debt.

As the post-U.S-election landscape unfolds, it's essential to refocus on long-term fundamentals rather than reacting solely to recent political shifts. History has shown that markets adapt over time, with various asset classes responding differently to changes in policy and sentiment. A well-diversified portfolio is positioned to withstand a range of potential scenarios, helping investors achieve steady progress toward their financial goals.

And last week we promised a return to our regular scheduled programing of Inflation 24/7. Well, this Wednesday we had U.S. Consumer Price Inflation (CPI) come in line with consensus for October. CPI prices increased 0.2% m/m, the same pace we have seen for four consecutive months. These data continue a string of six months of moderate consumer inflation, a measurable downshift from the first four months of the year. Nothing in the CPI report will preclude the Federal Reserve from one more quarter point rate cut before the end of the year.

Source: BMO Economics EconoFACTS: U.S. Consumer Prices (October)

Elsewhere, yes, parts of the post-election bump in markets reversed this week—the S&P 500 sagged 2% after last week’s 4.7% surge—but the U.S. dollar found a second wind. The currency was juiced by three factors: 1) The prospect of less rate relief from the Fed, per Fed Chair Jay Powell; 2) the growing appreciation that Trump’s tariff threats are real; and 3) the probability that the growth gap between the U.S. and other mature economies will remain wide in 2025. The Canadian dollar has been caught in the greenback tide, falling almost 2% just since last Tuesday to a four-year low of 71 cents ($1.408/US$). It hasn’t helped that Bank of Canada Governor Macklem suggested recently that the weak currency isn’t entering into policy decisions, and that deeply negative Canada/U.S. rate spreads are “not close” to their limits.

Source: Rates Scenario for November 14, 2024

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.