50 Shades of Cooling

DHL Wealth Advisory - Sep 20, 2024

Wall Street was muted Friday following an exciting week of trading that saw the S&P 500 and the Dow Jones Industrial Average hit all-time highs...

\

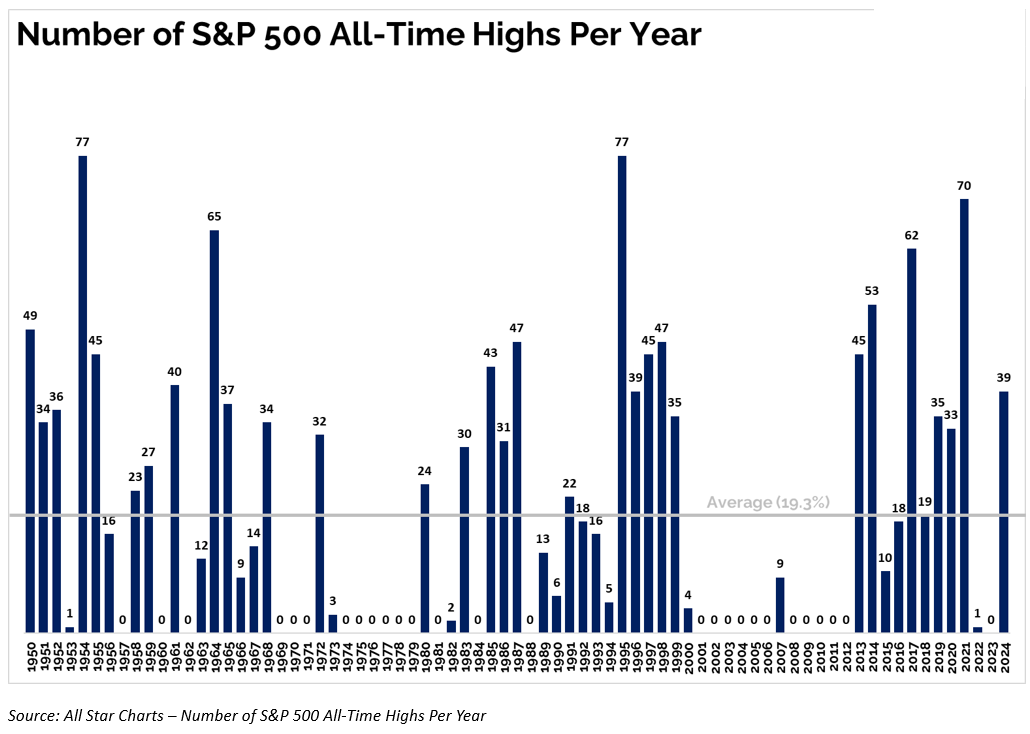

Wall Street was muted Friday following an exciting week of trading that saw the S&P 500 and the Dow Jones Industrial Average hit all-time highs. Bullish momentum on Thursday drove the S&P 500 to a 39th all-time high this year, while the Dow hit a 5th 1000-point milestone closing above 42,000 for the first time. Volatile is the word that will be used frequently over the next few weeks as investors face a barrage of uncertainty with the third quarter earnings season, an election cycle, and a central bank that is now working to preserve economic growth without re-stoking inflation. Despite the uncertainty, the Fed has significantly improved the odds of a soft landing and after four years, the U.S. seems to have solid economic growth, low inflation, and low unemployment.

After weeks of speculation the U.S. Federal Committee cut policy rates by 50 basis points on Wednesday, lowering the target range for the fed funds rate to 4.75%-to-5.00%, and marking the first cut since 2020. The reason for the large start was quite clear in the policy statement. Inflation had improved, and the labour market had deteriorated sufficiently to warrant bigger (than 25 bp) action. Chair Powell reaffirmed the “timely” move is a commitment to remain ahead of the curve. Indeed, more rate cuts are coming with the median dot plot projection showing an additional 50 bps of easing by the end of this year.

Source: BMO Economics AM Charts: September 19, 2024

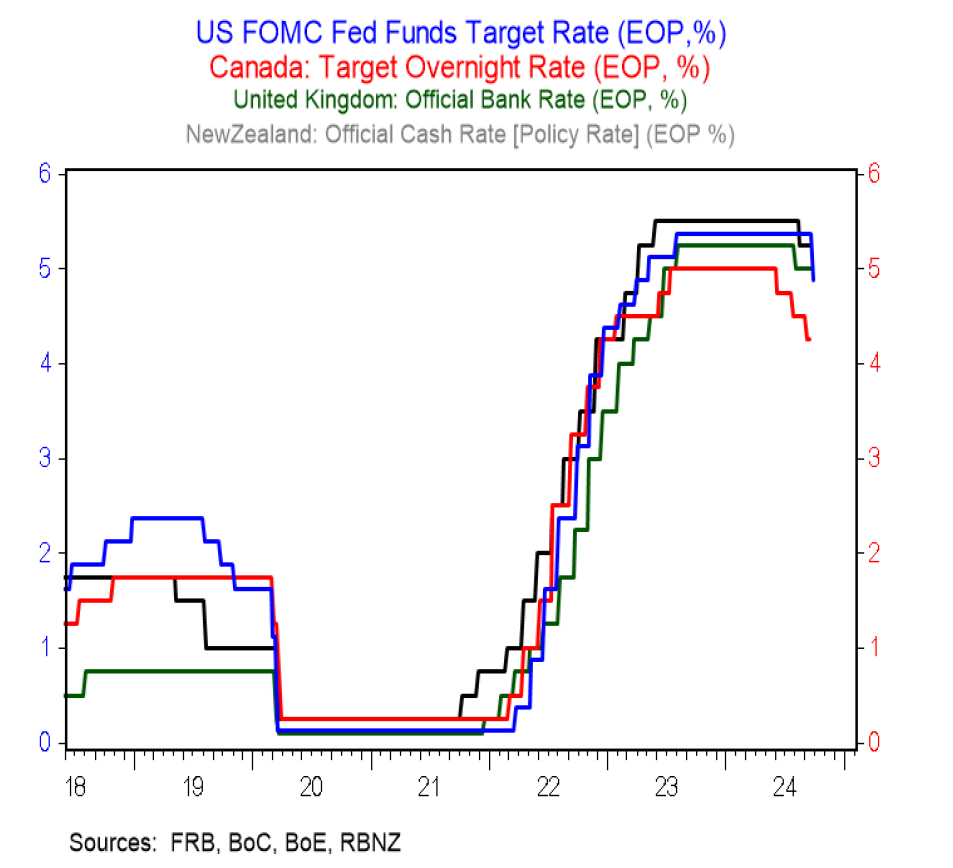

The four major central banks that had been the most aggressive hikers on the way up, and nearly moving in lockstep during 2022, are all now taking some different paths down the mountain. With the U.S. Fed’s 50 bp slash this week, its overnight rate has moved back below the Reserve Bank of New Zealand’s 5.25% rate. The Fed is now even below the Bank of England’s 5.0% rate, with the latter’s decision to hold rates this week. That’s the first time since June 2022 that U.S. short-term rates have dropped below U.K. rates. And lo and behold the pound is at its strongest level since—wait for it—early 2022. Meantime, back in Canada, the Bank of Canada (BoC) fell away from the most aggressive hikers in 2023 (after leading for a spell), and it’s not going back. The supersized Fed move opens the door wide for the BoC to match, data permitting.

Source: BMO Economics AM Charts: September 20, 2024

The two major events for Canada this week each surprised on the dovish side of the ledger. First up was the August Consumer Price Index, which saw an outright decline in prices and a drop in the annual rate to 2.0%—meeting the BoC’s target for the first time since early 2021. (We will point out that since the pandemic began, lo those 54 months ago, inflation has averaged a 3.6% annualized pace.) The core rates were mostly favourable as well, with median prices up just 2.3% y/y. And, as many were quick to note, inflation was a mere 1.2% ex-mortgage interest costs. This news arrived soon after Governor Macklem suggested that further downside for growth or inflation could readily prompt the Bank to cut faster and deeper. Then the Fed took its big step. Suffice it to say that it’s now hard to find anyone arguing against some outsized BoC cuts.

BMO Economics Talking Points: Goldilocks and the Wee Bears

The lone argument standing in the way of faster rate action from the Bank is the possibility that core inflation could reignite. And we cannot completely dismiss that possibility. Wage pressures certainly are still lingering, with a pilots’ strike at Air Canada only averted by a large four-year pay hike. The housing market remains in a slumber, but we all know that bear can awaken quickly and with a fearsome appetite. And, finally, the Canadian economy has been showing some signs of stirring from its sleepy 1% pace of the past two years. Retail and manufacturing sales were both solid in July, pointing to some potential upside for next week’s monthly Gross domestic product (GDP) release. The Bank is now openly gearing policy to reviving growth—it’s possible that the process may already be underway.

BMO Economics Talking Points: Goldilocks and the Wee Bears

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.