What's An Olympic Games Without a Scandal... Canada Just Started Early!

DHL Wealth Advisory - Jul 26, 2024

It was another week of volatility as the rotation trade out of mega-cap technology and into almost everything else continued to unfold...

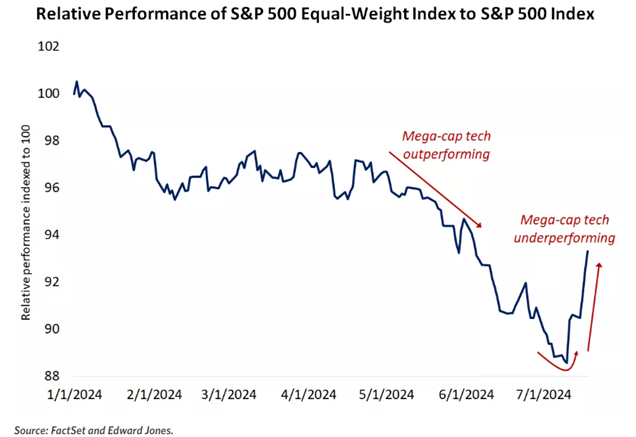

It was another week of volatility as the rotation trade out of mega-cap technology and into almost everything else continued to unfold. While equities have delivered solid returns this year, overall S&P 500 gains have been flattered by the sharp gains in the largest tech companies. It’s worth reminding readers that the S&P 500 is market-cap weighted, meaning larger companies have a larger influence on index moves. The average year-to-date gain for the mega-cap tech names (Apple, Microsoft, Amazon, Alphabet, Meta, NVIDIA, and Tesla) of ~30% has been a powerful force for much of 2024, a continuation of 2023's trend in which the vast majority of the S&P 500's 26% gain was attributable to the so-called "Magnificent 7" cohort.

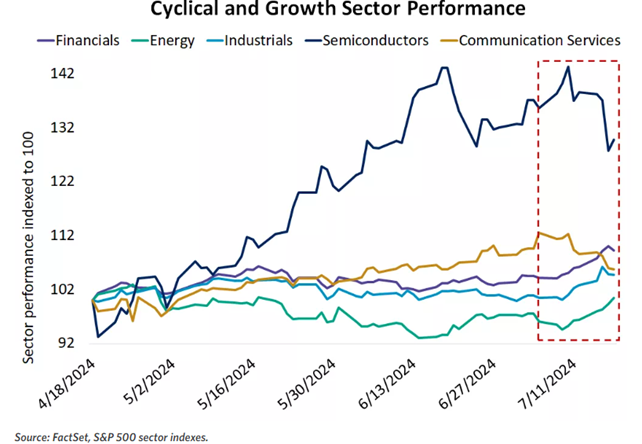

This tide turned noticeably last week, with the S&P 500 equal-weight index materially outperforming, reflecting the underperformance of the largest technology and communication services names, while cyclical sectors, like financials, industrials and energy, outperformed recently. We don't believe this signals the end of mega-cap tech leadership, as we have long advocated that the combination of defensible earnings streams and long-term AI growth prospects will remain a tailwind for that group. That said, we think the shift in recent weeks reflects what could be a more durable trend in which lagging sectors and segments of the U.S. large-cap market play catch-up. Earnings and valuations should support this trend. The rate of Magnificent 7 earnings growth has begun to moderate, while the growth rate of S&P 500 profits, excluding the Magnificent 7, is forecast to accelerate in each of the next four quarters. Against that backdrop, and the elevated valuations for high-flying tech stocks, we think the broadening of market leadership can continue this year.

Perhaps the most notable tide change last week was the renaissance in small-and-mid-cap stocks (SMID). SMID-cap stocks have been one of the best-performing areas within the stock market during July following a prolonged period of underperformance throughout this bull market, a reversal we thought has been long overdue. Much of the rhetoric justifying the move earlier in the month seemed to focus on the growing likelihood of a Donald Trump victory over Joe Biden in the upcoming election based on the polling data. However, election uncertainty returned with Biden dropping out of the race, seemingly to be replaced with Kamala Harris, with some polling data showing that a Harris-Trump match-up would be a much closer call. So far, this unexpected turn of events has not seemed to derail the recent momentum of smaller-cap stocks, and to be frank, we do not think politics matter all that much for this group to build upon July's strength in the coming months.

Source: SMID-Caps Finally Getting Some Attention

We have written several reports highlighting what we viewed as the mismatch between relative performance and the fundamental underpinnings of these stocks, and nothing has changed in that regard, in our view. In fact, even with this most recent rebound, relative underperformance remains quite extreme compared to historical standards, and this sort of weakness has typically been followed by swift rebounds over the past 30 years. In addition, the probability of a US Fed rate cut occurring as soon as September has increased substantially in recent weeks and smaller-cap stocks have tended to be main beneficiaries of Fed easing once it begins. Therefore, we continue to advise investors to increase exposure to this area since we believe that recent momentum is likely to persist based on these circumstances.

Source: SMID-Caps Finally Getting Some Attention

Speaking of asset rotation, Canada has exhibited some ebbs and flows of outperformance, but nothing sustained. We believe performance trends during the second half will be defined by a rotation into more undervalued, cyclical and smaller cap areas, part of an overall broadening of equity performance in both the US and Canada for remainder of 2024 and likely beyond. Therefore, this “shift” should prove to be a strong tailwind for Canadian equities, as fundamentals remain strong and revision trends have been broadly improving since the end of the first quarter.

Indeed, equity markets have already demonstrated what the broadening of performance could look like as the TSX has sharply outperformed the S&P 500 so far in July, with all S&P/TSX sectors outperforming the S&P 500 month-to-date. Overall, we continue to believe Canada is positioned for a significant catch-up trade, with Canadian small cap particularly well positioned even within the broader context of Canadian value. Additionally, with rates trending lower we believe the high yield sectors remain poised for a strong relief rally into year-end.

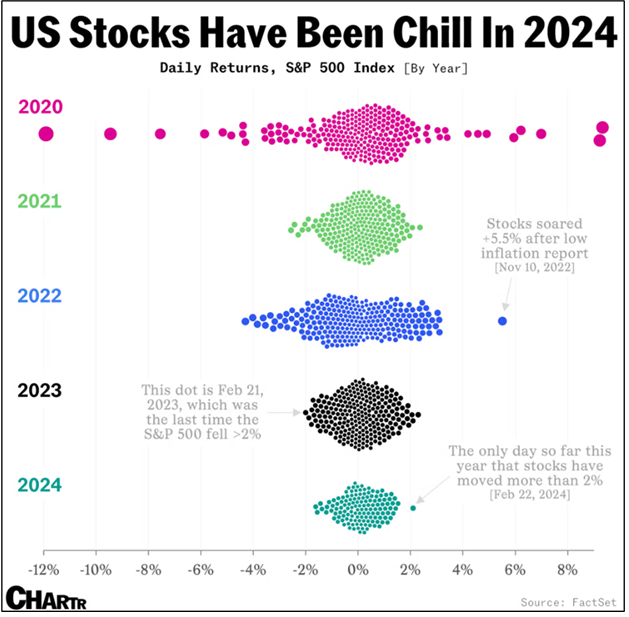

Ending with a very interesting chart that shows the lack of volatility witnessed thus far in 2024. Investors tend to have a recency bias, believing what happened recently is the “norm”. Well, the lack of volatility so far in 2024 has definitely not been normal. Take for instance the incredibly tight trading range of the S&P 500.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.