Rod Stewart Was Wrong.

DHL Wealth Advisory - Jun 07, 2024

The majority of North American benchmarks hit record highs this week as central banks around the world officially kicked off their rate cutting campaign...

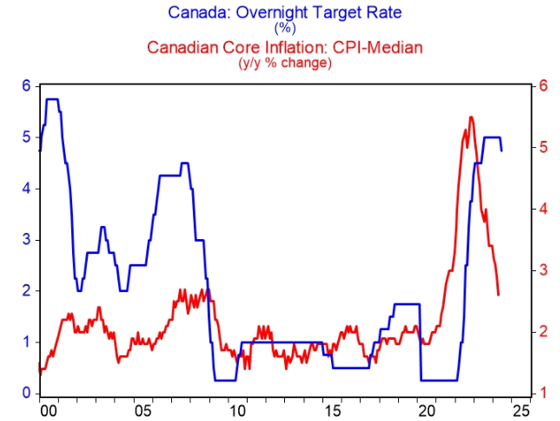

The majority of North American benchmarks hit record highs this week as central banks around the world officially kicked off their rate cutting campaign. On Wednesday the Bank of Canada was the first G7 central bank to cut its key lending rate 25 basis points to 4.75% - the first reduction in more than four years. Some of you may recall, or have chosen to forget this period entirely, but central banks around the world aggressively slashed interest rates to basically zero after Covid-19 (or governments) shut down the global economy.

The BoC rate cut was largely built in by financial markets, but was far from a sure thing, so the wording really in their press release really matters here. The overall tone was constructive for further cuts, and frankly a bit more dovish than most would have expected, but still with a healthy dose of caution. The Bank is clearly impressed with the broad moderation of underlying inflation in 2024, and plainly states that policy does not need to be so restrictive any longer, but is also obviously wary about moving too quickly.

The key message from Wednesday is that they are going to take this on a meeting-by-meeting basis, so every Consumer Price Index (CPI inflation) report matters, as does every GDP and jobless rate release, to a lesser extent. Canadian economists have been pencilling in rate cuts every other meeting for now as a base case, but—like the Bank—that call is data dependent. There are two CPI (and jobs) reports prior to next BoC rate decision; if the inflation reports mimic the very mild results seen so far this year, a cut is very much on the table for that decision as well.

Source: BMO Economics EconoFACTS: BoC — The Big Ease-y

Given the importance these rate cuts play into the strength of the broader economy and, by extension, the stock market, we have pulled some key quotes from Governor Macklem's Opening Statement (which has more meat than the press release):

• On further cuts: "If inflation continues to ease, and our confidence that inflation is headed sustainably to the 2% target continues to increase, it is reasonable to expect further cuts to our policy interest rate. But we are taking our interest rate decisions one meeting at a time."

• On the breadth of inflation: "...the proportion of CPI components increasing faster than 3% is now close to its historical average, suggesting price increases are no longer unusually broad-based"

• On why they thus cut: "This all means restrictive monetary policy is working to relieve price pressures. And with further and more sustained evidence underlying inflation is easing, monetary policy no longer needs to be as restrictive."

• On what could go wrong: "We don’t want monetary policy to be more restrictive than it needs to be to get inflation back to target. But if we lower our policy interest rate too quickly, we could jeopardize the progress we’ve made. Further progress in bringing down inflation is likely to be uneven and risks remain. Inflation could be higher if global tensions escalate, if house prices in Canada rise faster than expected, or if wage growth remains high relative to productivity."

Source: BMO Economics EconoFACTS: BoC — The Big Ease-y

Frankly, one 25 bp move, which had mostly been priced in, is not going to make a big impact to the economy all by itself. However, it will give at least a small bump to sentiment among borrowers, and brighten the mood in what has been a remarkably quiet housing market. As rates continue to gradually recede in coming quarters, the weight will be lifted off the struggling household sector, likely setting the stage for a modest improvement in growth in the year ahead.

Source: BMO Economics EconoFACTS: BoC — The Big Ease-y

Bottom Line: Rod Stewart was not paying attention in Econ 101. The first cut may not be the deepest, but it is the most significant, as it marks the official turning point after more than two years of restrictive policy. This is indeed likely to be the first of a series of cuts, although that series is not going to be a straight line down by any means. The Bank's tone is a bit more dovish than expected, but each and every cut this year will require evidence that inflation is calming.

Source: BMO Economics EconoFACTS: BoC — The Big Ease-y

Source: Bank of Canada, Statistics Canada

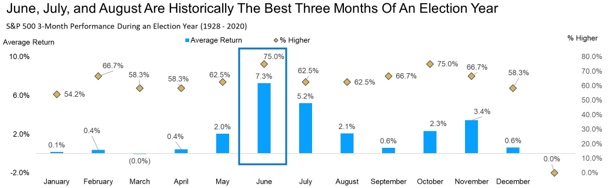

Meanwhile, we are here. June, July and August. Yes, summer, but it has historically been the best three months during an election year.

Source: Carson Investment Research, Factset 06/04/2024

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.