The First 100 Days...

DHL Wealth Advisory - May 24, 2024

North American markets hit new all-time-highs this week but finished in the red for the first time in over a month as concerns the Federal Reserve won’t cut interest rates this summer overshadowed a blockbuster earnings report from Nvidia...

North American markets hit new all-time-highs this week but finished in the red for the first time in over a month as concerns the Federal Reserve won’t cut interest rates this summer overshadowed a blockbuster earnings report from Nvidia. After several strong economic and labor data releases this week, some pundits pushed forecast for the Fed’s first rate cut back to September from July. Some profit taking was, however, inevitable following the best 2-week rally in the last 6-months.

So, with the US Federal Reserve stuck in neutral for a spell, the $32,000 question is how far can other global central banks carve out an independent path? That key question of recent months re-emerged in a significant way this week, as potential Fed rate cuts were pushed further into the future. First, the few U.S. economic data releases mostly surprised on the high side, after a run of downside results earlier this month. Notably, durable orders were solid through the spring, and S&P’s PMIs reported gains across the board in May. Second, the latest Fed Committee Minutes revealed that “various” members had actively considered whether rates eventually needed to go higher at the latest Fed meeting.

Source: BMO Economics Talking Points: Nvitable Divergence?

Now, don’t worry… Fed Chair Jay Powell has already suggested rate hikes are unlikely, and the recent moderate CPI probably soothed the concerns of others, but let’s just conclude that the “various” few are not going to be voting for rate cuts anytime soon. Markets now only have a full rate cut priced in by the December meeting, and more analysts are spying a no-cut year.

Source: BMO Economics Talking Points: Nvitable Divergence?

This shifting reality on the Fed finally made a minor mark on equities this week. Most major averages took a step back after hitting fresh record highs within the past five sessions, even with the support of yet another blow-out quarter by Nvidia. The Dow, which is not blessed with the presence of the AI/chip darling, saw its biggest setback in more than a year on Thursday, less than a week after reaching the promised land of 40k. The setback leaves the Dow up a pedestrian 4% so far this year—and we are now almost 40% of the way through 2024, for those counting—compared with an 11% gain for the S&P 500.

Source: BMO Economics Talking Points: Nvitable Divergence?

But does an on-hold Fed limit or even handcuff others, particularly the Bank of Canada? The chances of the BoC trimming rates at its upcoming meeting on June 5 actually rose this week, on yet another mild Canadian CPI inflation result and more softness in retail sales. On the latter, sales fell for the third month in a row in March, and are now up a paltry 1.9% from a year ago, or just 0.8% in real terms, and deeply negative on a per capita basis (remember, we have absolutely roaring population growth right now). Sluggish spending is clearly cooling underlying inflation. All the major measures of core CPI rose just 0.1% m/m in April (seasonally adjusted), holding the annualized increases below the 2% target since the start of the year.

Source: BMO Economics Talking Points: Nvitable Divergence?

The contrast between Canadian and U.S. inflation trends in 2024 could not be starker. To pick but one glaring example, markets cheered last week’s U.S. April CPI, where core still rose 0.3%, and we are expecting a mild 0.2% rise in next week’s core PCE deflator. Good news, but this is still above the latest 0.1% result in Canada. And after starting the year with Canada and the U.S. running at precisely the same headline inflation rate of 3.4%, the U.S. has seen no change while Canada’s rate has dropped to a much more comfortable 2.7%. Excluding those bothersome shelter components, Canadian inflation is now a minuscule 1.2%.

Source: BMO Economics Talking Points: Nvitable Divergence?

Inflation expectations and perceptions have scarcely been squashed in Canada either, but the economic case for rate cuts is still solid. After a small burst at the start of the year, it looks like GDP growth cooled considerably in the spring, with next Friday’s result likely to reveal a drop in March (even with a 2% rise in Q1 as a whole). Full year real GDP growth will barely top 1%, despite 3% population growth. The jobless rate has climbed a full percentage point in the past year, even with some gaudy employment gains. The housing market has been (eerily) calm in the prime spring season. And all measures of core inflation are now below 3%, and apparently headed lower with short-term trends all below 2%.

Source: BMO Economics Talking Points: Nvitable Divergence?

Bottom Line: Central banks will do what needs to be done for their domestic economies. But with the Fed standing pat for a long stretch, we continue to pencil in cuts in the June, September and December meetings (i.e., every other decision), based on the assumption that there will be a line of sight to Fed rate cuts at some point in the second half of the year.

Source: BMO Economics Talking Points: Nvitable Divergence?

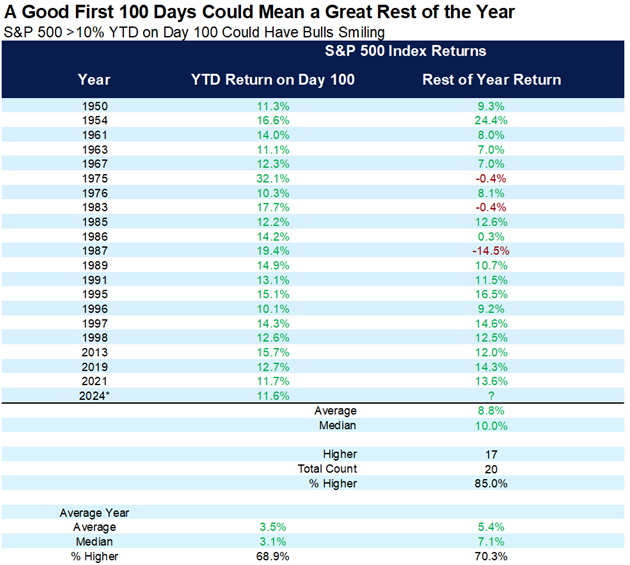

Meanwhile, Thursday was the 100th trading day of 2024.When the S&P500 is up 10% YTD on this day, the rest of the year is up a median +10%, average +8.8% and higher 85% of time. Much better than the average year. The last 9 times, 8 saw strong double-digit gains.

Source: Carson Investment Research

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.