Total Eclipse... Of the Jobs Report.

DHL Wealth Advisory - Apr 05, 2024

Stocks rebounded Friday but still posted declines on the week following the worst session in over a year on Thursday. Investors are torn between wanting a strong economy to support further corporate earnings growth and wanting a weaker jobs market...

Stocks rebounded Friday but still posted declines on the week following the worst session in over a year on Thursday. Investors are torn between wanting a strong economy to support further corporate earnings growth and wanting a weaker jobs market that will give the Federal Reserve the green light to begin cutting interest rates. Friday’s session saw traders flip the “good news is good news” side of the coin as they embraced a stronger-than-expected jobs report and looked past a jump in rates.

Markets are understandably confused, but the fundamental economic circumstances which are the actual data series being released, like the jobs report on Friday, just continue to affirm two things: strong employment growth, and that the economy is not anywhere near recession…

The U.S. labour market appears to be strengthening, not slowing, and risks delaying Fed easing. Nonfarm payrolls blasted 303,000 higher in March, the most since last May and nearly 100k above the consensus call. This boosted the Q1 average to 276,000, which is up from 212,000 in the prior quarter and from 251,000 in 2023. Widespread gains across the private sector (232,000) were complemented by continued strong hiring in the public sector (71,000). And, unlike in recent months, the household survey showed a much stronger pulse, with employment rising for the first time in four months, by almost half a million. This was largely in line with a surge in the labour force amid rising population growth and a two-tenths climb in the participation rate. A tight labour market is drawing in more job seekers and most are finding work, with the unemployment rate edging back to 3.8%.

Source:BMO Economics EconoFACTS: U.S. Nonfarm Payrolls (March)

Diving into the data a little more, average hourly earnings growth picked up to a 0.3% monthly pace, but favourable base effects clipped two tenths from the yearly rate to 4.1%, the slowest since 2021. Bottom-line: The FOMC will take some modest comfort from slower wage growth and greater labour force participation, but employment is simply growing too fast to loosen the labour market and ease price pressures in the services sector. Look for Fed officials to continue walking back expectations of a near-term rate cut.

Source: BMO Economics EconoFACTS: U.S. Nonfarm Payrolls (March)

Meanwhile, Canada’s labour market reported dramatically different results on Friday. Canadian Employment fell 2,200 in March, only the second decline in 18 months, and abruptly snapping a strong start to the year. Amid the ongoing surge in population (up by another 91k last month alone for those 15 and over), this small stutter in job creation sent the unemployment rate up a full 3 ticks—a large move for a month—to 6.1%, up exactly 1 percentage point from a year ago. We would suggest that the job market is officially no longer tight, and may be quickly tipping the other way.

Source: BMO Economics EconoFACTS: Canadian Employment (March)

To some extent, it almost feels like Canada was due for a sour jobs release, given the softness in underlying growth over the past year. Still, it's a bit of a surprise in light of the solid start to 2024 on the growth front. Probably the two most important stats from this report are: 1) the 1 point rise in the unemployment rate over the past year to 6.1%, and 2) the stickiness of wages growth at 5.1% in the face of that softness. That combination leaves the Bank of Canada in a tricky spot, with the job market clearly softening, yet still spinning off strong income gains. On balance, the BoC will likely view the overall results as pointing to more disinflationary pressure ahead, and will await the next couple of inflation prints, but a June cut is looking a bit more likely now.

Source: BMO Economics EconoFACTS: Canadian Employment (March)

For the past few weeks now we have been saying that given the uninterrupted nature of the stock-market rally since last November, a pullback and consolidation phase should be expected, and perhaps we saw the start of that this week. However, the combination of resilient economic growth, a reacceleration in corporate profits, and the upcoming start of a rate-cutting cycle at a time when financial conditions are already easy is likely to help sustain the expansion and bull market. We expect this environment to be supportive for investments, but, in our view, the greater opportunity lies within equities, particularly in areas of the Canadian and U.S. market that have lagged and carry lower valuations.

More specifically, small- and mid-cap stocks look particularly interesting. Historically, they've been among the strongest-performing asset classes 12-18 months following the last Federal Reserve rate hike, but they've lagged since the Fed's last hike in July of last year. As investors' confidence about the economic outlook increases, that could help release the catch-up potential of the asset class.

In our view, the recent broadening of the market gains, with the equal-weight S&P 500 outperforming its market-cap peer, and with value-style investments outperforming growth over the past month, is a sign that the bull market is not exhausted. We think conditions are more like the soft landing scenario of the 1995-1998 period rather than the hard landing of 1999-2000. The average stock in the S&P 500 trades at a reasonable 16.7 P/E, with more stocks and sectors participating in the rally. To that point, 10 of the 11 S&P 500 sectors are higher over the past three months. For comparison, three months before the burst of the tech bubble, seven of the 11 sectors were lower.

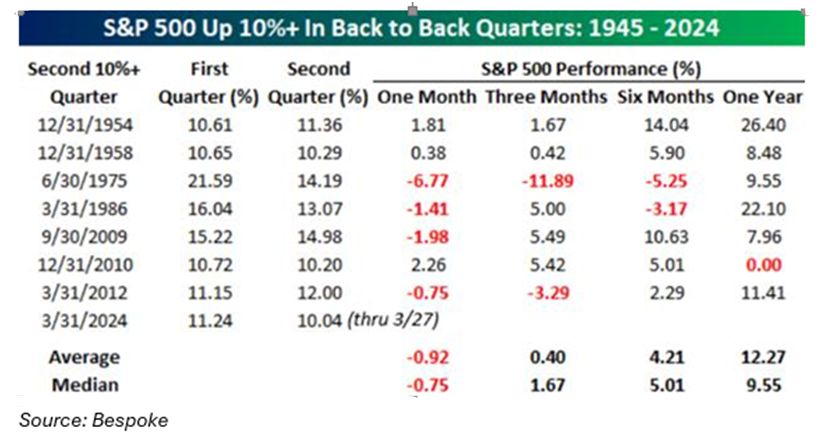

Interestingly, since 1945, there have been 7 instances when the S&P500 has been up +10% in back to bank quarters. The market is positive on average the next 3-, 6-, and 12-months after. The point here is that strength begets strength.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.