We'll Take More Random Holidays, Please.

DHL Wealth Advisory - Feb 16, 2024

It was a volatile, but positive week for North American markets as investors aggressively sold off a stronger-than-expected US CPI Inflation report on Tuesday. Despite Tuesday being the worst day for the market in almost a year...

It was a volatile, but positive week for North American markets as investors aggressively sold off a stronger-than-expected US CPI Inflation report on Tuesday. Despite Tuesday being the worst day for the market in almost a year, markets clawed their way back to gains on the week with the S&P 500 trading steadily above the 5,000 threshold.

The story of the week was U.S. CPI inflation, both the headline and core measures, came in well-above market expectations for January. The data really put a dent in the moderating inflation narrative that has taken hold in the markets and among some Fed officials. Headline CPI increased 0.3% in January, above the consensus forecast of 0.2%, and notably above the downwardly-revised December reading of 0.2%.

The “hotter” than expected reading was driven once again by the usual suspects -- strong price increases in food, services, and housing components, despite the anticipated decline in gasoline prices. Shelter alone contributed over two-thirds of the monthly increase. Shelter (+0.6%), services ex. energy (+0.7%), medical care services (+0.7%), transportation services (+1.0%), energy services (+1.4%), food at home (+0.4%) and food away from home (+0.5%) all surged last month. From a year ago, headline CPI inflation moderated to 3.1% from 3.4% in December. The consensus was hoping for a sub 3.0% reading. This inflation report for January, along with resilient first-quarter U.S. economic growth, calls into question market forecasts for aggressive and early rate cuts this year. The inflation data are much more in-line with our expectations for a June/July initial rate cut.

Source: BMO Economics EconoFACTS: U.S. Consumer Price Index (January)

At the end of the day it all comes down to the consumer. Generally, personal consumption accounts for two-thirds of GDP in Western economies. While one couldn’t tell by looking at consumer spending, the Fed's most aggressive rate-hiking cycle in 40 years has had an impact in slowing economic activity. Housing and manufacturing, two of the most interest-rate-sensitive sectors of the economy, have been under pressure. Housing activity has been subtracting from economic growth for nine straight quarters but turned slightly positive in the last quarter. And the ISM Purchasing Managers Index (PMI), a proxy for manufacturing activity, has been in contraction for 15 consecutive months.

With the Fed now preparing to pivot to rate cuts, the outlook for these sectors is gradually brightening. The average 30-year mortgage rate has dropped about 1.1% from its peak, the NAHB homebuilder sentiment survey has ticked higher, and a shortage of housing supply is helping activity stabilize. On the manufacturing front, orders are now growing faster than inventories, and the ratio between the two, which tends to lead the PMI index by about three months, suggests an acceleration in activity and a return to expansion in the months ahead.

What all this means is that, in our view, the window for a hard landing or a recession appears to be closing as central bank policy becomes gradually less restrictive. That is not to say that a soft landing or no landing is inevitable, especially in Canada as the economy continues to deal with the debt and housing imbalances, but we are moving further away from the worst-case scenarios, in our view.

Meanwhile, if you feel there’s a bit of DeJa Vu going on in the market, you aren’t entirely wrong… Last year a narrow group of mega-cap technology stocks drove most of the S&P 500 gains as enthusiasm around AI grew. One of our calls for this year is that the segments of the market that have been left behind will start to catch up and leadership will broaden. So far in the first six weeks of the year, it's been some of the usual suspects that have led the gains (NVIDIA, Meta, Eli Lilly and Shopify in Canada). Only three of the 11 sectors of the S&P 500 are outperforming the index (communication services, technology and health care), while U.S. small- and mid-caps have not been able to make up the lost ground. Even with the status-quo continuing early in the year, there are encouraging signs that more stocks are starting to participate in the rally. The growth-sensitive industrials sector and the rate-sensitive homebuilders are now breaking out to new highs, while financials are only modestly lagging the S&P 500, even with renewed concerns about regional and community banks. We think that a rotation from mega-cap tech into cyclical and value-style investments is still in the cards as the year progresses, especially if central banks cuts rates for the right reasons (improvement in inflation rather than a slump in growth), as we expect.

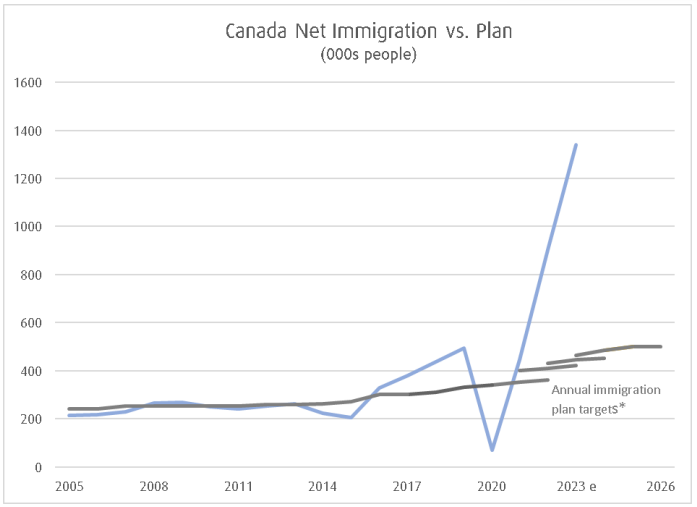

Ending this week on a BMO Economics report that we found very interesting, Canada has historically boasted a carefully-managed system of permanent resident targets, and that does remain in place today. In the 2023 Immigration Levels Plan, Canada set permanent resident targets peaking at 500k per year by 2025 and 2026. Those official immigration targets have been rising steadily from about 300k before the pandemic and around 250k in the decade prior.

Source: BMO Economics AM Notes: February 16, 2024

Now, we’ll be among the first to argue that a robust pipeline of skilled immigrants is essential to maintain future labour force and potential output growth. But, the current population ‘situation’ goes well beyond robust official targets. The roughly 1.3 million net international inflow in the past year has dwarfed these targets, entirely on the back of non-permanent resident inflows. This has proven to be inflationary, a drag on per-capita growth and a major factor stretching housing affordability. It’s also unreasonable to expect the supply side (e.g., municipal infrastructure and homebuilders) to plan for demand so many magnitudes above expectations.

Source: BMO Economics AM Notes: February 16, 2024

Source: BMO Economics AM Notes: February 16, 2024

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.