Start Strong. Stay Strong. Finish Strong.

DHL Wealth Advisory - Jan 19, 2024

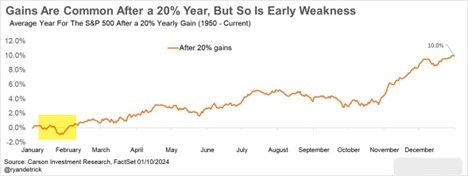

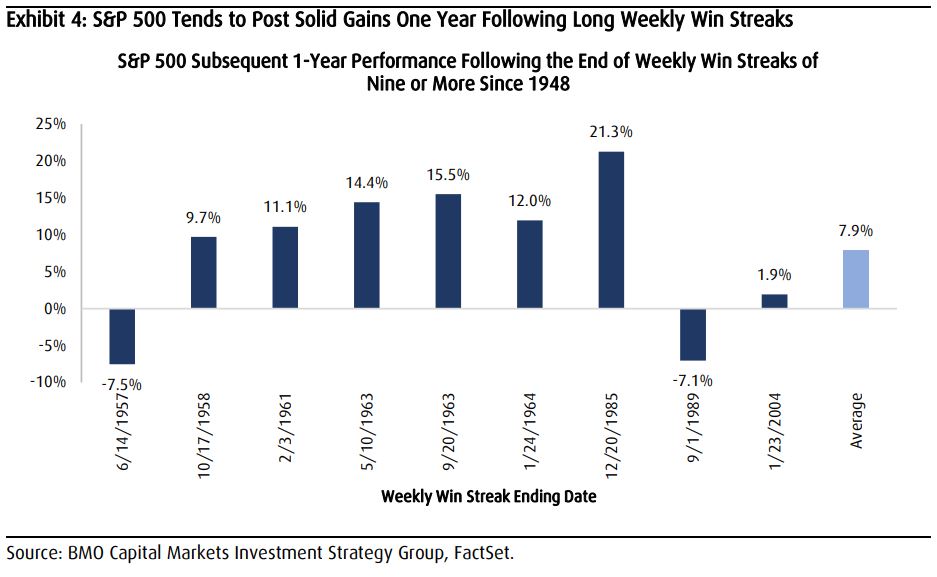

Weakness in US stocks during the first few days of January raised some concerns for investors but on Friday the S&P500 rose to an all-time high. This momentum comes on the back of the longest winning streak for US stocks in 20 years..

This week saw markets take a roller coaster ride as investors digested a slew of mixed economic data. Wednesday, we received the January 30th Fed regional report card, known as the Beige Book, which details economic conditions across 12 regions. The report confirmed a slowing economy but also an improved outlook reflecting supportive financial conditions and expected rate cuts. While data is relatively mixed between districts the overall report shows a loosening labour market and easing inflation pressures. This strengthens our expectations that the next course of action by the Fed will be rate reductions. However, the underlying resiliency of the economy and strength in the consumer will likely give policymakers all the more reason to drag their heels.

Weakness in US stocks during the first few days of January raised some concerns for investors but on Friday the S&P500 rose to an all-time high. This momentum comes on the back of the longest winning streak for US stocks in 20 years. 2023 finished the year with nine consecutive weekly gains, something that has only occurred 10 times since 1950. Given the rarity of this streak and the overall strong performance for the year it would be normal to expect some early weakness. What we find more interesting is that the S&P 500 tends exhibit relatively solid gains in the one year following the end of the prior streak. More then 80% of the times the S&P500 delivered a 20% gain it was followed by a positive year with a 10% return average.

Back over to Canada, this week saw December’s headline inflation rate in line with consensus while core inflation showed a slight surprise to the upside. The persistence in core continues to suggest that the last mile (or kilometre) of the inflation fight may prove to be the most challenging—bringing underlying inflation sustainably back below 3%. Given that wage trends are also stuck in the 4%-to-5% range, and now even housing may be showing a pulse, suggests that the Bank of Canada will doggedly maintain a cautious stance at next week's rate decision. We are comfortable with our call of a first rate cut at the June meeting, even as the market leans in earlier.

Source: BMO Economics EconoFACTS: Canadian CPI (December)

While there will likely be many fluctuations stemming from shifting monetary expectations, interest rates, and earnings outlook, we continue to believe that the fourth quarter performance trends were a good indicator of what 2024 may look like. Fourth quarter performance for the TSX was relatively in line with most global markets however, overall, the TSX underperformed the S&P by the largest margin since 2013.

Source: BMO Capital Markets: Canadian Strategy Snapshot

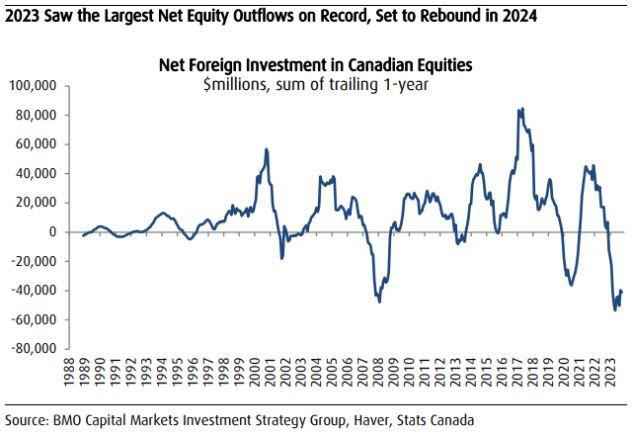

We expect Canada will see a strong catch-up trade throughout the year as equity performance broadens out and asset flows return. Indeed, while Technology still dominated performance in the fourth quarter, the market saw the beginning stages of the broadening out of US equity performance, which we expect to be a key driver of performance in 2024. In fact, Canadian equity flows started to improve in the final months of the year after reaching record lows in mid-2023. This helped propel the Financials sector to be one of the top-performing sectors in the quarter and ultimately outperform the TSX in 2023.

Source: BMO Capital Markets: Canadian Strategy Snapshot

We believe the concentration of performance in US mega -caps has been a significant factor in the lack of equity flows into Canada in 2023. In fact, 2023 saw the largest net outflows of Canadian equities on record. From our perspective, as performance broadens out and confidence returns, foreign flows will improve.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.