A Santa Claus Rally, Indeed!

DHL Wealth Advisory - Dec 15, 2023

Wall Street extended its rally this week after dovish Federal Reserve signals raised optimism the world’s largest economy will be able to avert a recession. North American benchmarks surged with the S&P 500 fast approaching its record...

Wall Street extended its rally this week after dovish Federal Reserve signals raised optimism the world’s largest economy will be able to avert a recession. North American benchmarks surged with the S&P 500 fast approaching its record and the Nasdaq 100 hovering near that mark. The Dow Jones, meanwhile, is now trading in record territory.

Christmas spirits were unleashed as the Fed pivoted toward reversing the steepest hikes in a generation after taming inflation without a major economic slowdown. Without officially saying that rate hikes are off the table, the FOMC has added another 25 bps to its rate cut hopper for next year in addition to not hiking again this year (so the funds rate is 50 bps lower than before), and they are now starting to discuss when to release them. This alone is a dovish signal and strongly suggests we are done with hikes. However, keeping rate hikes on the table (admittedly collecting dust) and with total and core PCE inflation just barely dipping below the 2.5% mark by the end of next year, we still judge rate cuts will commence later rather than sooner, likely mid-2024.

To paraphrase the Fed statement, Chair Powell’s press conference and the dot plot: the Fed is done raising rates; they’re not looking at a recession; the job market will remain firm through the forecast horizon; and inflation will continue to fall toward target, setting up rate cuts (75 bps) next year. To be fair, the Fed will need to see further progress on inflation before they start cutting rates, which is one reason why we think they might not ease as soon as the market now expects. But, market psychology has still been dealt a meaningful win—that is, there’s certainty now in knowing what the worst-case interest rate conditions are for this cycle

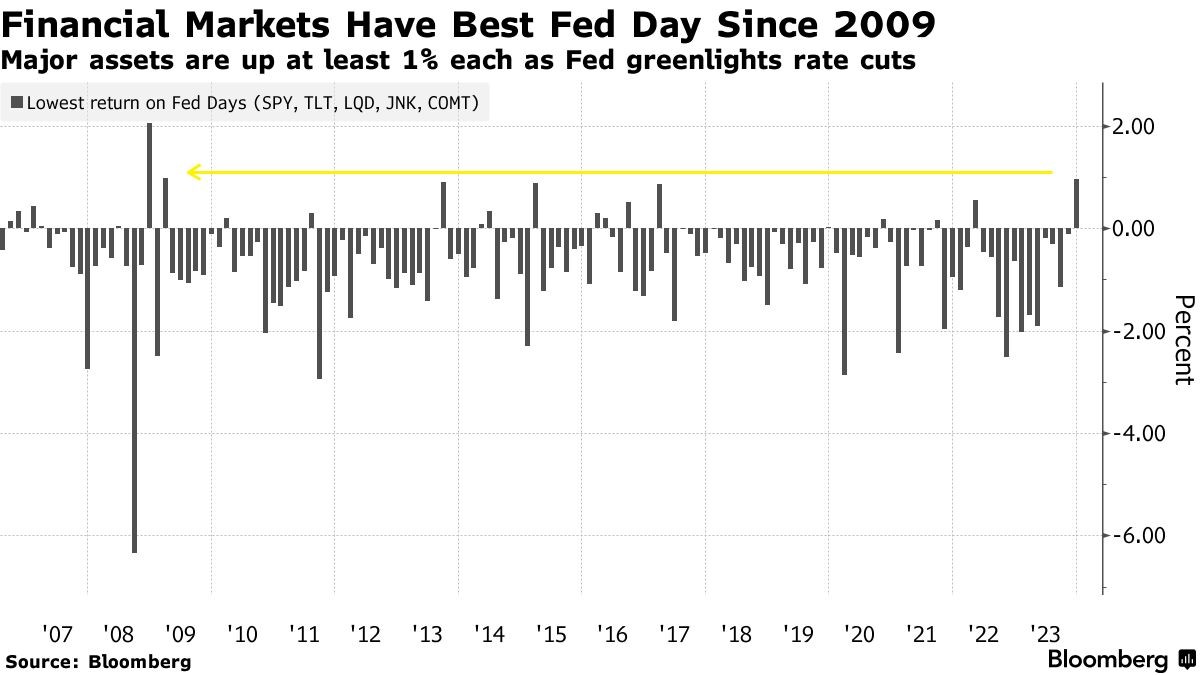

From stocks to Treasuries, credit to commodities, everything was up after the Fed projected more rate cuts in 2024. The scope and intensity can be illustrated by a measure that tracks the lowest return of the five major exchange-traded funds following these assets. With gains of at least 1%, the pan-asset advance beat all other Fed days since March 2009.

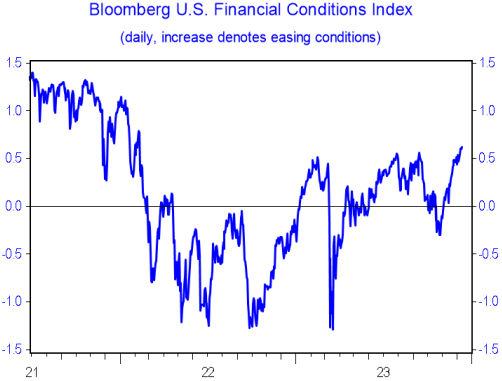

We have been writing about this Soft Landing vs Hard Landing scenario for most of 2023, so why not speak about it again once more in our last edition of the year. Soft landings are rare for a reason. Monetary policy influences the economy (and inflation) largely through changes in interest rates. Yet, the economy also responds to other factors, such as stock prices and credit spreads, that are, in turn, affected by interest rates —collectively called financial conditions. As shown in the chart below, apart from earlier this year during the regional bank scare and again in the fall when equity and bond markets briefly sold off, U.S. financial conditions have eased in 2023, after tightening in 2022 on heavy-duty rate hikes. The lagged effect of supportive financial conditions should increase the odds of a soft landing in 2024 —provided it doesn’t staunch inflation progress. Going back half a century, the economy has never slipped into recession when financial conditions were as supportive as they are today.

Source: Bloomberg

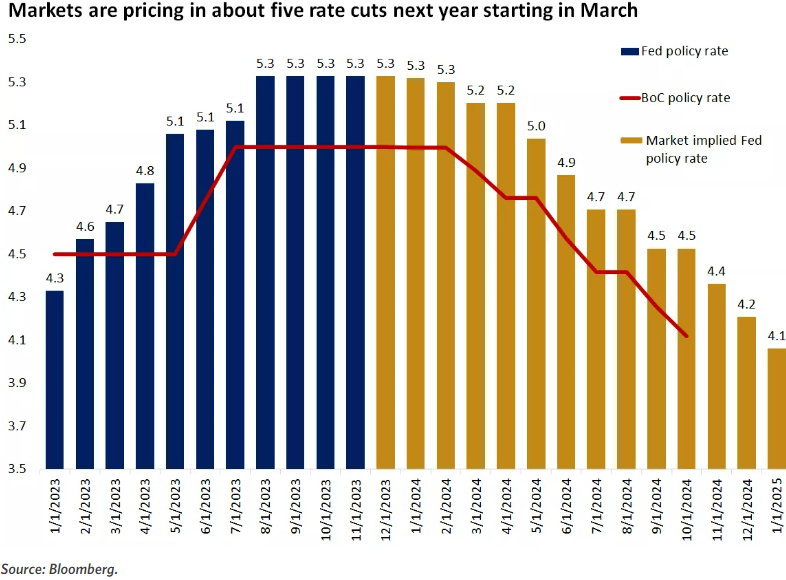

As inferred, economic data is laying the groundwork for central banks to pivot, and markets are taking notice. Fed-fund futures are now pricing in rate cuts as early as March, though July was expected just few weeks ago. While policymakers are likely interpreting the incoming data the same way, they will probably caution against pivoting to rate cuts too quickly, as that would risk unwinding some of the tightening in financial conditions that is helping apply pressure on inflation. That's exactly what the BoC did last week by stating that it is prepared to raise the policy rate further if needed.

Looking forward, a potential tug of war between market pricing and central bank messaging could drive volatility in bond and equity markets, but we expect both forces to move in the same direction as the new year progresses. If a couple of quarters of soft economic growth materializes, expectations are for the Fed to cut rates three to four times in the back half of 2024. As price pressures ease further, the real policy rate (after adjusting for inflation) will become more restrictive, which the Fed and BoC will try to offset by cutting rates more than it currently forecasts. In this scenario, we could see the U.S. 10-year Treasury yield falling slightly below 4% and the GoC yield below 3% by the end of 2024.

No doubt 2024 will bring its own twists and turns in the market narrative, but there are reasons for cautious optimism. Interest rates have likely peaked, as the Fed and BoC start paving the road for rate cuts, inflation continues to moderate, and valuations outside of the big year-to-date gainers remain reasonable.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.