Dog Days

DHL Wealth Advisory - Aug 25, 2023

Global markets were mixed on the week with the S&P 500 and NASDAQ posting their first weekly gains of August, while the Dow Jones and S&P TSX continued their slide. After a steady rally...

Global markets were mixed on the week with the S&P 500 and NASDAQ posting their first weekly gains of August, while the Dow Jones and S&P TSX continued their slide. After a steady rally from March through July, the market's mood has shifted more recently, with stocks posting a rather weak August so far. The S&P TSX is down ~5% in August and a similar number for the S&P 500, but, as the chart below illustrates, is still having a strong year, ~15%. Enthusiasm around a resilient economy, moderating inflation and artificial intelligence is not gone, but it has been countered by global growth concerns and a leg higher in interest rates of late.

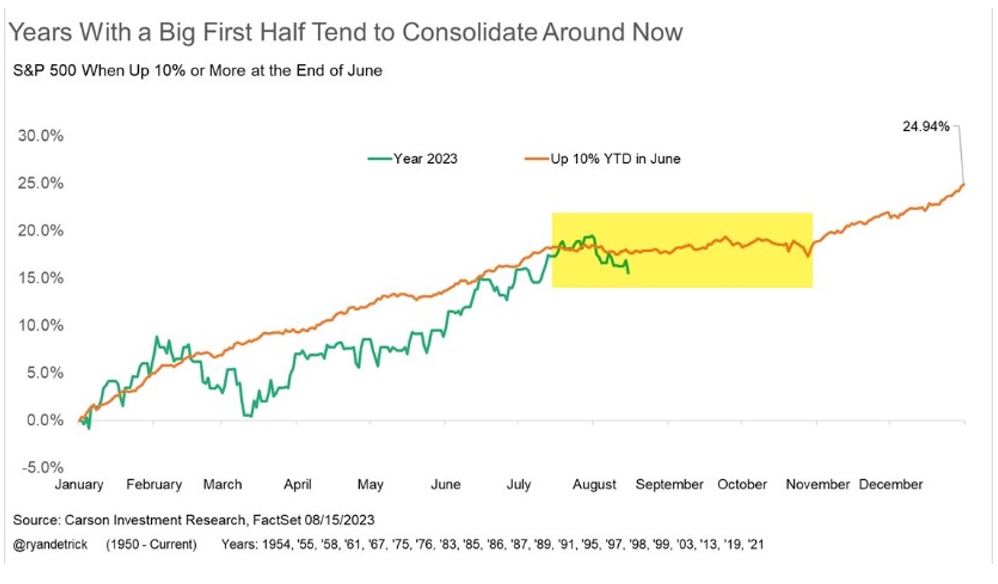

Heading into August we spoke of general seasonal weakness and for market participants to expect some consolidation after impressive year-to-date gains. In fact, there have been 21 instances when the S&P 500 was up more than 10% by the end of June. Historical trading shows that the market would trade sideways for a period of 2-3 months before picking up again around November. As the chart below illustrates, the historical average calendar return in these instances has been 24.94%.

Aside from the usual period of seasonal weakness, there has also been an uptick in interest rates. Recall that central banks are increasing interest rates in attempt to slow down global economies. The sharp rise in interest rates through 2022 was documented ad nauseam (and felt much the same) as both stock- and bond-market performance suffered last year. Coming into 2023, the general consensus amongst strategists was for the sharp and steady rise in rates to abate as the central focus shifted from high inflation to lower growth. While the aggressive hiking campaign did abate, growth hasn’t slowed nearly as much as anticipated. As such, we've seen longer-term rates climb materially in recent weeks, with the 10-year Treasury yield and Government of Canada bond yield hitting new highs for the year.

We attribute the bulk of this run-up in rates to an update in consensus expectations around U.S. Fed policy. The resiliency in economic growth is prompting markets to accept that central banks will in fact be keeping rates higher for longer.

Now, what does this for investors? First, we don't think the jump in the 10-year yield is a signal that the Fed will resume another phase of rate hikes ahead. Inflation has been moderating, a trend we expect to continue, though not perfectly linear. This point was made very clear in last week's domestic consumer price index (CPI) report, which revealed an uptick in headline inflation (to 3.3% from 2.85%), but also displayed that underlying disinflationary trends remain intact. If that trend persists it will, of course, make the Bank of Canada's job a little more difficult with rate decisions in coming months, but we don't believe it changes the broader monetary-policy story in Canada. In the U.S., the decline in inflation, to us, means the Fed doesn't need to put in a new round of policy tightening, but it also means that nobody will be entertaining rate cuts anytime soon.

This week we saw U.S. durable goods orders lose altitude, falling 5.2% in July as expected. The lofty June advance was also taken down a few ticks to 4.4% (previously 4.7%). The reversal marks the first decline in new orders since February.

Source: BMO Economics EconoFACTS: U.S. Durable Goods Orders (July)

Then there was U.S. existing home sales which fell more than expected, down 2.2% to 4.07 mln annualized in July, marking the lowest level since the start of the year. Sales of single-family homes wilted 1.9% while condos fell 4.5% .

Source: BMO Economics EconoFACTS: U.S. Existing Home Sales (July)

Meanwhile Canadian retail sales ticked up 0.1% in June, slightly better than the flat flash estimate previously published by StatCan. However, the details were softer as the increase was driven by a 2.5% jump in autos. Most of the remaining sectors were down, leaving sales ex-autos down 0.8%. The regional picture was also mixed with only four of ten provinces posting increases.

Source: BMO Economics EconoFACTS: Canadian Retail Sales (June)

The point we are making here is that the impacts of Fed rate hikes are still working their way through the economy. The end of policy-tightening cycles are traditionally a favourable development for market performance. We don't expect a sharp leg higher from here for interest rates, but we do think the help markets are receiving from the stronger-than-expected economy is partially offset by the resulting upward pressure exerted on higher bond yields.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.