MWW - Like Messi in Extra Time, Fundamentals Keep Finding Ways to Win

DHL Wealth Advisory - Jul 17, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

If investors needed a reminder of what's driving markets in 2026, the opening weeks of July delivered one. While renewed tensions in the Middle East briefly pushed oil prices higher and generated headlines, equity markets largely looked through ...

If investors needed a reminder of what's driving markets in 2026, the opening weeks of July delivered one. While renewed tensions in the Middle East briefly pushed oil prices higher and generated headlines, equity markets largely looked through the noise. Instead, investors remain focused on the factors that have fueled this year's rally: strong corporate earnings, continued AI investment, resilient economic growth, and broadening market leadership.

That optimism received an early boost from the start of earnings season. With approximately 10% of S&P 500 companies having reported, over 80% have exceeded analyst expectations, continuing a trend that has characterized much of the past two years. Consensus estimates currently call for S&P 500 earnings growth of roughly 8-9% in the second quarter, supported by healthy consumer spending, expanding profit margins, and ongoing investment in AI infrastructure.

Energy markets moved back into focus after escalating tensions between the U.S. and Iran raised concerns about global oil supplies. Iran resumed attacks on commercial vessels in the Strait of Hormuz, while the U.S. reinstated restrictions on Iranian oil exports and conducted additional military strikes. Even so, the market's response has been remarkably measured.

Oil prices have risen roughly 15% from their recent lows to around $80 per barrel, but remain well below the highs reached earlier this year. More importantly, investors appear increasingly confident that the global economy can absorb higher energy costs without materially disrupting growth.

Several factors support this view:

Neither side appears eager for a prolonged conflict. Markets have learned repeatedly that geopolitical events often create short-term volatility but rarely alter long-term investment outcomes. Historically, periods of conflict-driven weakness have frequently proven to be buying opportunities rather than reasons to exit the market.

Energy supplies remain relatively well supported. OPEC has increased production targets, Iranian exports remain available through alternative channels, and global inventories are healthier than during prior energy shocks.

Economic fundamentals continue to improve. Canada's unemployment rate declined to 6.5% in June, its lowest level since January, while U.S. economic data has remained resilient. Combined with a positive earnings backdrop, the foundation for continued market growth remains intact.

Recent market behavior reinforces that message. Earlier this year, sharp moves in oil prices frequently triggered equity market weakness. More recently, that relationship has weakened significantly as investors place greater emphasis on earnings, economic growth, and AI-related investment trends.

Meanwhile, AI remains one of the market's most powerful drivers. The U.S. semiconductor index recently completed its strongest quarter on record, advancing 88%. While pockets of volatility have emerged—particularly among companies perceived to be spending aggressively—the broader investment thesis remains intact.

Importantly, there is little evidence that demand is slowing. Capital spending on AI infrastructure continues to expand, cloud providers remain committed to large-scale investments, and earnings growth across the AI ecosystem remains impressive. What we're witnessing appears less like the end of a cycle and more like the natural evolution of a maturing investment theme.

The encouraging start to earnings season also suggests market leadership may continue to broaden. Strong results are increasingly coming from a wider range of sectors, not just mega-cap technology. Industrials, financials, materials, energy, and select Canadian mid-cap companies are beginning to participate more meaningfully in the market advance.

Looking ahead, we believe the second half of the year could look different from the first—but not necessarily worse. Rather than being driven primarily by momentum and a handful of AI leaders, returns may become increasingly supported by earnings growth, attractive valuations, and sector diversification.

Bottom line: Despite geopolitical headlines, the market enters the second half of the year from a position of strength. Economic data remain constructive, AI investment continues to drive growth, and earnings season is off to a promising start. While volatility is always possible, a broader and healthier market advance may be taking shape. For investors, maintaining exposure to long-term themes such as AI while diversifying across sectors and regions may be the most effective way to participate in the next phase of the market cycle.

In our view, the combination of resilient economic growth, better-than-expected earnings, and expanding market participation provides reasons for optimism as we move through the remainder of 2026.

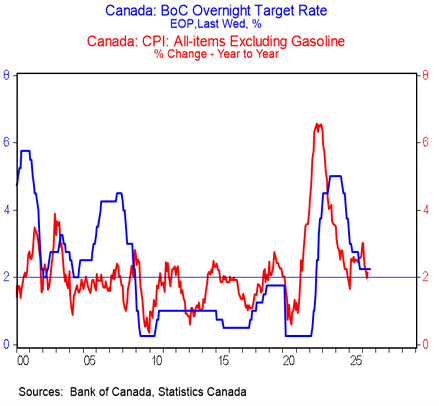

Elsewhere, to the surprise of no one, the Bank of Canada kept rates unchanged at 2.25% for the sixth consecutive meeting. The overall tone of the remarks was a bit more upbeat on the growth outlook, while still flashing plenty of concerns over the uncertainty on the inflation outlook. The BoC did nudge up its 2026 estimate for CPI from the April call by 2 ticks. But there has been no change in the outlook for core inflation. Thus, the Bank continues to see little spillover to other prices from high oil costs. The Bank specifically singled out the ex-gasoline CPI, which is now running at 2.2%—or basically right in line with the overnight rate of 2.25%. The Bank says that rate is at the low end of neutral. We would point out that since 2000, both the overnight rate and ex gasoline CPI have averaged precisely 2.2%—so the current rate looks pretty close to neutral to us!

Sources: BMO Capital Markets Economic Research - BMO Economics AM Charts: July 16, 2026

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.