MWW - Less Chip, More Dip... and a Better GDP

DHL Wealth Advisory - Jul 03, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

It was a mixed week for North American benchmarks as investors sold the high-flying semi conductor stock and rotated into other areas of the market. Breadth on the week was position, which is encouraging, but indexes were trading with elevated

It was a mixed week for North American benchmarks as investors sold the high-flying semi conductor stock and rotated into other areas of the market. Breadth on the week was position, which is encouraging, but indexes were trading with elevated volatility around the semi/hardware trade which now accounts for 15-20% of major benchmarks. Take the price action in Micron Technologies, which has become the poster boy of the semi trade: shares were down ~25% in the last 5 trading sessions, but the stock is still up 250% on the year and some 800% in the last 12 months...

While the price action in the markets and the unwind of the semi trade can generally be viewed as positive, what was definitely positive was Canadian GDP... On Monday we learned that Canadian real GDP rose by a sturdy 0.5% in April, and the early read on May is for a further 0.1% gain. The strong April advance - it was actually +0.547%, so nearly up 0.6% - was the second fastest rise in the past two years, was above consensus, and even managed to top the flash estimate of +0.4%.

The reading helps wash away the bad taste of two small quarterly declines in Canada's economy around the turn of the year. It is fair to say that Q2 started on a solid footing, and there is substantial upside to estimates of 1.0% GDP growth in the quarter which ended Monday; if these numbers hold, Q2 is on track for growth of over 2%.

The rebound in April from a small dip in March was broadly based as 14 of 20 groups were up, including strong gains in a wide array of industries. Leading the way was a big 3.7% rebound in oil production, with large growth in both oilsands and conventional output. Natural resources could have been even stronger if not for maintenance in "other metal ore mining" and a resulting 28.3% fall there. Meantime, manufacturing, construction, rail transportation and pipeline activity all rebounded in sync, as the Canadian economy seemingly shook off the winter blues all at once. As a result, the goods-producing sectors rose by a robust 1.2% m/m, but with a nice assist from services, which rose 0.3% m/m. Overall, the snap-back left GDP up 1.1% from year-ago levels, quite a different picture from the reported 0.1% y/y dip in Q1 from the quarterly results a month ago.

The bounce in April is clearly a correction from the prolonged winter lull and is unlikely to persist. Still, it's good news that May likely saw at least some further gains, which will leave output up 1.3% from year-ago levels. May's gain looks to be led by services, with notable strength in finance and insurance, but a pullback in wholesale trade. A more moderate gain in May GDP will serve as a reminder that Canada is still growing slower than potential, so no one should mistake the April bounce as a sign of a robust economy. Nevertheless, it's also clear that the small two-quarter dip in output was a false alarm on the recession watch.

Bottom Line: While a nice rebound for Canada's economy in April was widely anticipated, this solid result topped almost everyone's expectations and will presumably silence the recession chatter. The broad-based nature of the snap-back is especially encouraging. Even so, the reality is that output is still up only a little more than 1% from a year ago, which is below potential and still more consistent with monetary policy biased to ease rather than to tighten.

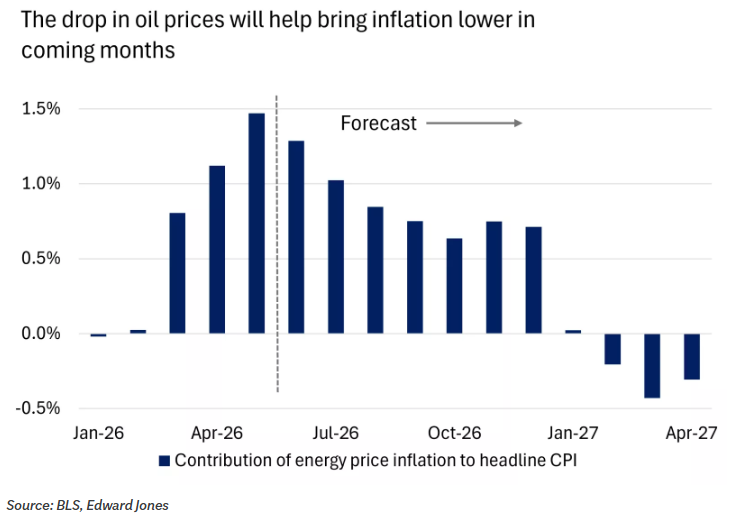

Elsewhere, oil continued to give up its gains this week and at its low on Wednesday was down +45% from its peak in April. Rising energy prices have been a key driver in surging U.S. inflation this year. In the latest May data this component alone added a full 1.5 percentage points to headline Consumer Price Index (CPI) inflation, which hit 4.2% in year-over-year terms.

The good news, in our view, is that the drop in oil should reverse a good portion of this spike in coming months. Absent any unexpected surges in other parts of the CPI basket this would mean that the peak in the 2026 inflation spike is likely now behind us, with helpful disinflation on the way.

We should see a similar dynamic in Canadian inflation over coming months. Headline inflation is running at 3.2% in year-over-year terms, but, excluding energy prices, this increase stands at a more moderate 2.1%. We expect the gap between these two measures to close, as headline inflation softens in coming months.

Cooler inflation should provide a helpful boost to households, with national average gas prices now down to $3.90 per gallon in the U.S. ($1.69 per liter in Canada) and likely to fall further in coming weeks and months.

We think this relief could be quite substantial. In the U.S. real household incomes fell at an annualized run rate of 1.5% through March to May amid strong inflation. Households absorbed this shock remarkably well, with last week's spending figures showing a further rise in consumption in May, taking the increase in spending over this three-month period to 2.1% annualized. However, households did so by saving less, with the savings rate for the household sector down to just 3%. A partial reversal of the oil spike should provide more firepower to drive spending and rebuild savings, in our view.

This potential tailwind is just the latest cause for encouragement around the U.S. economy. The labour market has gained momentum this year, first-quarter GDP growth was revised up to 2.1% (from 1.6%), and growth in the second-quarter is tracking a healthy looking 2.5%, helped by robust household and business spending. Growth has been bumpier in Canada over recent quarters, but as we discussed earlier, has started to improve.

Meanwhile, Central Banks will also likely be marking down their near-term inflation projections in the wake of lower oil prices. As these pressures moderate, markets are already anticipating fewer interest rate hikes.

As we move into the second half of the year, the fundamental backdrop remains constructive. While the recent volatility in semiconductor stocks has captured most of the headlines, the underlying story is one of broadening market participation, improving economic momentum, easing inflation pressures, and a central bank outlook that is becoming less restrictive. Markets may continue to experience rotations and periodic bouts of volatility, particularly in the most crowded areas of the AI trade, but a healthier market environment is ultimately one where leadership expands beyond a handful of stocks. For investors, the message remains unchanged: stay diversified, stay disciplined, and focus on the longer-term opportunity set rather than short-term market noise.

Sources: BMO Capital Markets Economic Research: Cdn. Real GDP — Technical Recovery?

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.