MWW - Oil: Stairway to Seven-handle

DHL Wealth Advisory - Jun 19, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

North American markets resumed to their winning ways on the back of what might actually be an end to the ongoing issues in the Middle East. It was a case of energy down and stocks higher with the price of Crude Oil plummeting ~$20 on the news of

North American markets resumed to their winning ways on the back of what might actually be an end to the ongoing issues in the Middle East. It was a case of energy down and stocks higher with the price of Crude Oil plummeting ~$20 on the news of a Memorandum of Understanding being sign by both Iran and the United States.

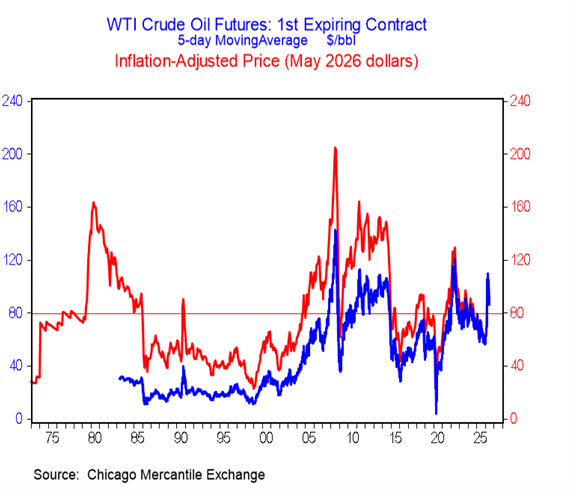

In fact, Crude Oil prices gripped the seven-handle on Tuesday for the first time since the first week of the conflict in early March. Assuming the pullback is sustained, this will cause some serious relief for central banks as it will take the wind out of headline inflation fairly promptly. For example, North American gasoline prices are already on track for a steep decline in June, which will be reflected in next month’s CPI reports.

Bigger picture, we will just point out that compared with past oil shocks, this one was relatively tame. The accompanying chart has converted the past five decades of oil prices into today’s dollar terms (red line), and the recent spike doesn’t come close to the doozies of 1979, 2008 or even 2022, in either level or duration. As well, note that the latest WTI price of around $74 is already below the long-run real price of $79. And, finally, prices are now in-with year-ago levels—WTI averaged $74/bbl in the third week of June 2025.

As we have written to in recent MWW’s, central banks around the world were trying to look past what could have been a relatively temporary spike in energy prices. If status quo remains, we could see inflationary readings resume their path lower, as had been the case the first few months of the year.

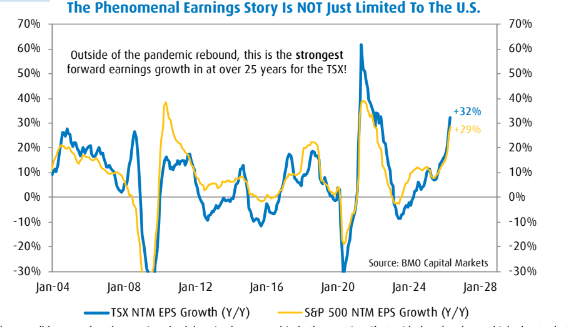

Turning to the broader equity markets, our avid readers will have seen us say this before: Earnings are the lifeblood of equity markets. Yes, market multiples also play a role in equity returns but a strong earnings profile is usually a solid anchor for stocks. Surely, there are plenty of risks out there for both the U.S. and the Canadian equity markets. Interestingly, the difference in Index composition between the S&P 500 and the TSX makes them vulnerable to different factors in 2026. That said, they have one thing in common: phenomenal earnings.

Indeed, forward earnings growth in the S&P 500 currently runs at 29% and it’s a tad higher at 32% for Canada’s S&P/TSX Index. These are not normal growth rates. In fact, we have only seen stronger numbers coming out of the global financial crisis (GFC) in the early 2010s or in the wake of the pandemic. Needless to say, earnings took a massive hit in those two events, so a rebound was to be expected. This time around, we are seeing numbers of this magnitude with earnings that had only declined slightly. This is truly a rare backdrop for earnings in both the U.S. and Canada.

Let’s talk about what’s similar between the two stock markets. Earnings growth is phenomenal in both regions. As said on the previous page, we don’t typically see earnings accelerate like this outside of crisis-recovery periods. Obviously, AI euphoria plays a role here, but the strength is much broader than that structural story. The weight of Technology in the S&P/TSX Index is only about 7%, so that’s clearly not enough to significantly move the needle. Leading economic indicators (LEIs) have been improving since the fall of 2025, so it’s normal for earnings to follow suit. The AI story certainly helps, but the backbones of an earnings acceleration are also cyclical in nature. The conflict in the Middle East not withstanding, we expect this backdrop to remain in place well into 2027.

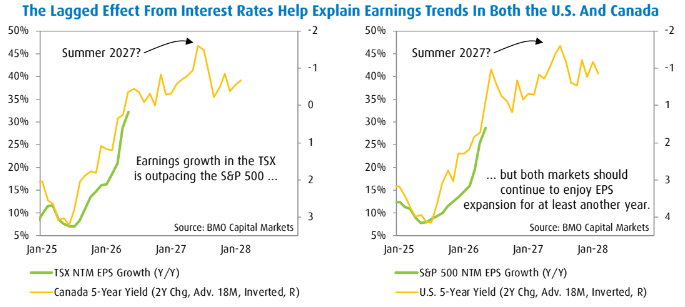

Anyone familiar with our macro framework knows that monetary policy, and interest rates by extension, are the cornerstone of our analysis. Although the tide is beginning to change, the percentage of global GDP with stimulus in the pipeline had been running at about 90% (we’re now around 75%), and the U.S. and Canada were no exception. Changes in rates impact the markets and the economy with a significant lag time. It takes about 18 months for rate trends to filter through to leading indicators like the stock market, and another six months to hit coincident numbers like GDP. So, in essence, we are still digesting rate cuts from 18-24 months ago. The lead time is much longer than most people realize, which is why we are still enjoying the benefits of monetary easing. Certainly, if energy prices remained high for long, the inflation story would catch up to us, particularly in the U.S. where GDP is about 68% consumption based. Canada fares a bit better in this respect with a little more than half of GDP stemming from the consumer.

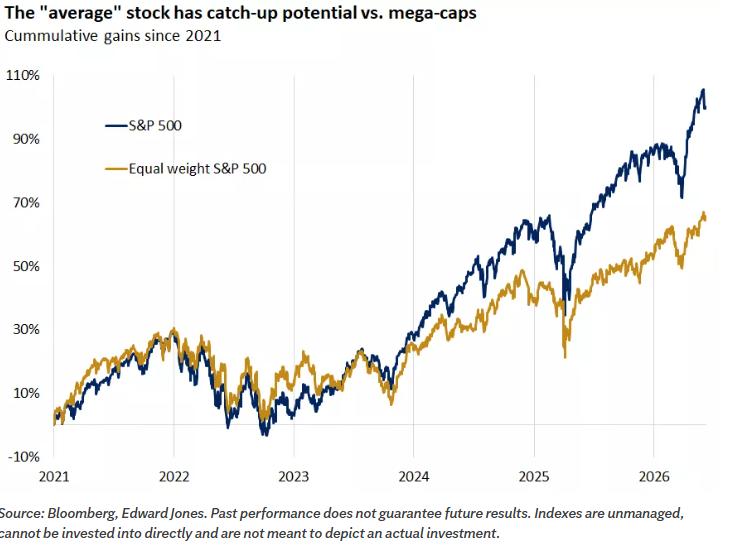

As markets often do, they tend to move in a “two steps forward, one step back” pattern. Following a strong two-month rally, it wasn’t totally surprising to have witnessed a pause the two prior weeks. And we would not be surprised to see further pauses over the summer months. Rather, we see markets transitioning:

- From narrow to broader leadership;

- From suppressed to more normal volatility; and

- From momentum-driven gains to a more mature phase of the cycle.

In the near term, this transition is likely to bring choppiness, particularly as leadership continues to evolve. However, with the economy resilient and earnings rising at a fast pace (second-quarter earnings are expected to grow 21%), we would expect any pullback to be corrective rather than indicative of a major peak or change in trend.

As it relates to IPOs, while each offering is unique, particularly at the scale of this year's listings, history suggests that early enthusiasm does not always translate into sustained outperformance. Among the 30 largest IPOs in the Russell 3000 over the past 20 years, companies have, on average, declined roughly 2.8% over the first three months following listing, while the S&P 500 gained about 3% over the same period. Over a longer horizon, these companies have underperformed the broader index by approximately 15% in their first year of trading. This reinforces the importance of selectivity and discipline. We recommend evaluating new opportunities based on fundamentals, valuation, and portfolio fit, rather than headlines and hype.

Overall, the summer “heat” may not come from a weakening market, but from shifting leadership and rising volatility. We remain constructive and would view pullbacks as opportunities to gradually add exposure and further diversify portfolios as the market evolves, based on your investment goals, risk tolerance and time horizon.

Sources: BMO Economics AM Charts: June 17, 2026; BMO Capital Markets, Portfolio Strategies Canada - Spotlight Is On The S&P 500 But Other Markets Are Equally Impressive!

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.