MWW - Game On!

DHL Wealth Advisory - Jun 12, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Equity markets struggled over the past week, as volatility picked up following a stronger-than-expected U.S. employment report. Although geopolitical tensions in the Middle East escalated, oil prices ended the week little changed, suggesting markets

Equity markets struggled over the past week, as volatility picked up following a stronger-than-expected U.S. employment report. Although geopolitical tensions in the Middle East escalated, oil prices ended the week little changed, suggesting markets are still weighing supply risks against broader demand dynamics.

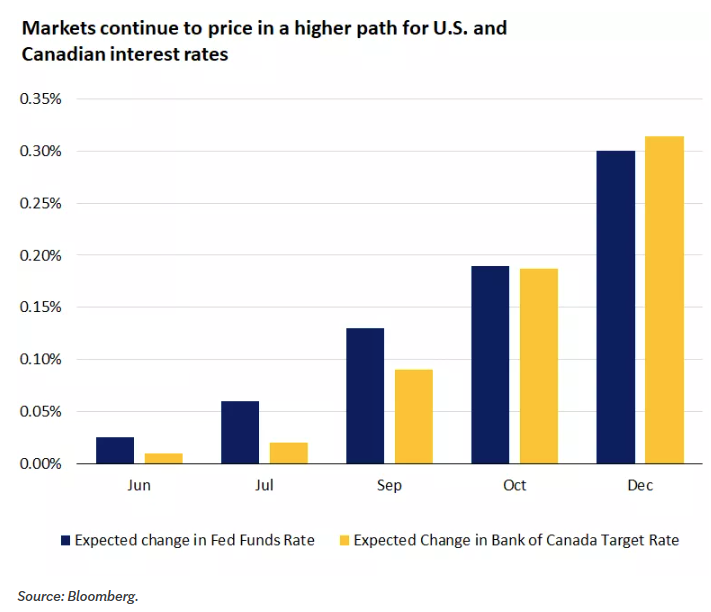

The real catalyst for the pullback was the jobs data. While stronger employment would typically be welcomed, investors instead worried that continued labour market resilience could delay or even reverse the Fed’s easing cycle. Money markets are now reflecting expectations for at least one 25bp rate increase by year-end, with further tightening priced in over the longer term.

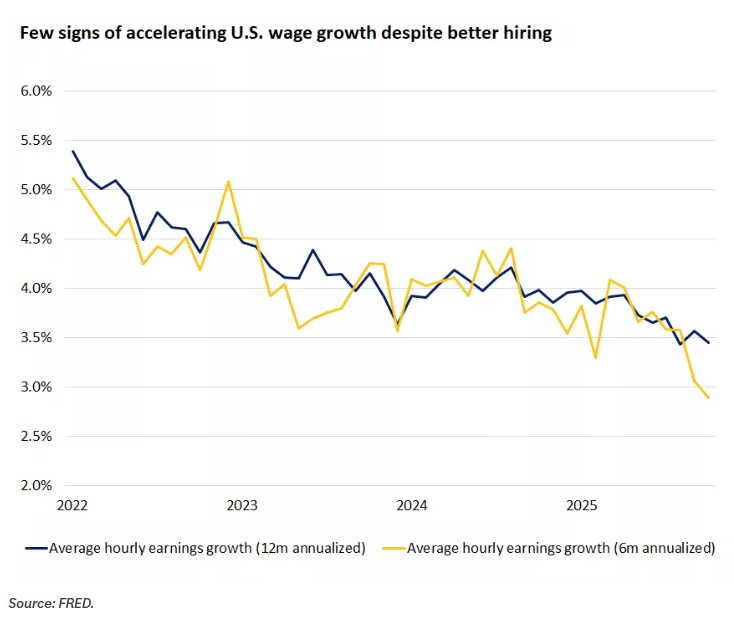

That said, this is not a classic overheating story. The unemployment rate has remained stable, and wage growth is still relatively contained. While steady payroll growth—particularly in the 150,000 to 200,000 range—could gradually tighten labour supply, especially given weaker immigration trends, any meaningful inflationary impact would likely take time to emerge.

What has changed is the Fed’s justification for easier policy. Late last year, softer labour conditions were cited as a key reason to consider rate cuts. Since then, the addition of roughly half a million jobs has challenged that narrative, while inflation risks have become more prominent.

At the same time, geopolitical developments are adding complexity. Optimism around a potential U.S.–Iran agreement are on again (but were off again) —combined with disruptions around the Strait of Hormuz—have increased the risk of energy-driven inflation. This backdrop helps explain why markets have shifted so dramatically from expecting multiple rate cuts earlier in the year to now contemplating hikes.

This sets the stage for a pivotal FOMC meeting under new Chair Kevin Warsh. While Warsh has previously emphasized the disinflationary potential of AI-driven productivity gains, near-term conditions make an immediate pivot to rate cuts unlikely. The key issue will be how he responds to growing market expectations for tighter policy.

Our view is that the Fed will aim to strike a middle ground. Policymakers are likely to acknowledge upside inflation risks—particularly from energy—but also emphasize that current policy settings are appropriate. While the possibility of further tightening may be left on the table, the hurdle for raising rates appears relatively high, especially if inflation pressures remain contained outside of energy.

In Canada, the case for additional tightening is even weaker. Inflation, excluding energy effects, remains well behaved, and economic growth has been subdued in recent quarters. As a result, the Bank of Canada is likely to remain on the sidelines for the rest of the year.

Looking beyond short-term market reactions, the underlying message from the labour market is constructive. A healthier employment backdrop supports consumer spending, economic growth, and ultimately corporate earnings. While higher interest rates can weigh on valuations, they are less problematic when they reflect stronger economic fundamentals.

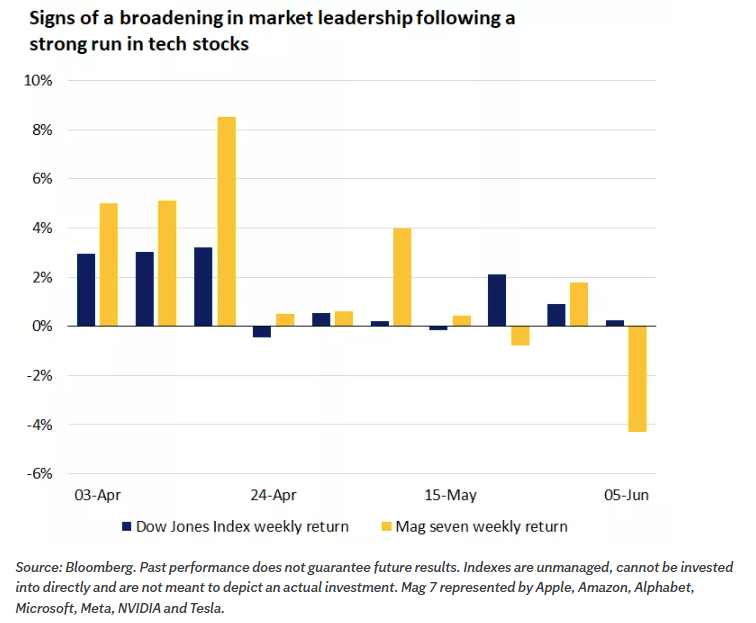

This environment could also encourage a shift in market leadership. AI-driven equities have dominated performance in recent months, but momentum showed signs of fatigue last week following weaker results from Broadcom. The Nasdaq has pulled back meaningfully since the jobs report, suggesting investors may begin rotating into other areas of the market as the cycle evolves.

Sources: BMO Economics EconoFACTS: U.S. Employment (May) - U.S. Job Growth Gaining Steam

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.