MWW - Cutting Through the Noise

DHL Wealth Advisory - Jun 05, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Three months after the eruption of hostilities in the Middle East, the most frequent question we get is, “Why are capital markets doing so well?” Year to date, the S&P/TSX and S&P 500 are up ...

Three months after the eruption of hostilities in the Middle East, the most frequent question we get is, “Why are capital markets doing so well?” Year to date, the S&P/TSX and S&P 500 are up almost 10%, European markets are up mid-single-digit percentages, and Japan and emerging markets have climbed in the 20%-plus range.

The short answer: the global economy is less reliant on energy inputs today than it was in the past (and that’s not a too-distant past). In addition, the stock market includes many companies (very large and market-moving companies in technology and communications services) whose fortunes aren’t significantly impacted by a commodity shock.

In the early days of the conflict, the priority was to understand and quantify the effect of higher energy prices and other key commodity supply disruptions on the global economy, inflation, plus monetary and fiscal policy, and evaluate their implications for equity and bond markets worldwide.

Three months on, we see the constructive view was directionally correct; however, many didn’t appreciate how much the positives outlined are cancelling out the negatives. Investors are reminded that during times of uncertainty it’s important to remain calm, focus on the facts, and stay invested.

We now see that the economy has enough momentum to absorb this shock and still be okay. Prior to the shock, the economy was unfolding along the Goldilocks theme – not too hot and not too cold. Today, Goldilocks is being held hostage in the Strait of Hormuz, but she can be freed. Middle East supply disruptions are being managed in a number of ways: through some demand destruction (like work-from home mandates/guidance in some countries); rerouting around the Strait of Hormuz (SoH); clandestine shipping; relaxed sanctions against Russia; increased production elsewhere; and the use of strategic inventories.

Providing additional salve for the capital markets: prices for key commodities in futures markets are still signalling that the conflict will be resolved – oil contracts for delivery in one, two and three years are all in the US$70 range (and have stayed there despite the on-off ceasefire/SoH reopening promises). The economy’s ability to continue absorbing the shock may have an expiration date, but that date appears to be much farther down the road than many had imagined.

In the meantime, positive drivers of stocks and certain parts of the economy have picked up the slack (capital spending on defence, infrastructure, and AI). Softening the blow are previously announced tax cuts — including tax cuts on energy specifically — and consumers who are dipping into their savings (not a long-term positive factor).

Inflation is perking up; however, recall that it was on a downward trajectory pre-conflict. In addition, some of the things causing that downward trend don’t respond quickly to a commodity shock – housing and wages, to name two.

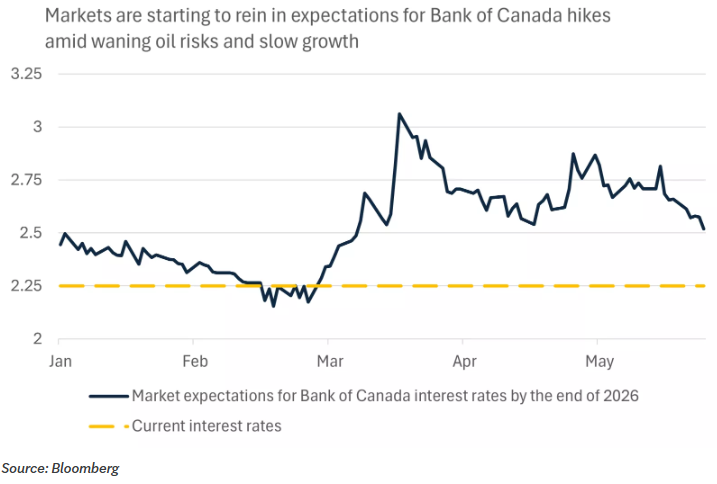

We aren’t dismissing inflation; it is a problem. Inflation running a little high (the number starts with a three instead of a two) is problematic, especially for the lower echelons of the economic strata. Cold and calculating capitalism doesn’t react to this plight until things start to break: unemployment rises or consumption falters more broadly beyond the bottom of the so-called K-shaped economy (some call it E-shaped – a top, middle and bottom). Either way, escalating inflation and higher short-term borrowing costs and mortgage rates aren’t meaningfully crimping consumption or employment. Therefore, policymakers, both fiscal and monetary, are not panicking. Rumblings from these quarters did drive some volatility in bond markets during the month. The whole issue of potential central bank actions (either raising or lowering rates) remains a top worry for some market pundits. However, many economists are not in that camp.

Although rate hikes are not constructive in our opinion, we also don’t believe hikes (even if they are motivated by central bankers’ desire to maintain credibility) will upset the apple cart; markets respond to rate cycles, not minor tinkering.

Markets don’t get too fussed about central banks changing rates in either direction unless bankers signal that these moves are the start of a sustained campaign. We aren’t hearing this, nor are markets pricing in this scenario. We are cognizant that this scenario could happen, yet we believe it is far enough down the road that we can put it in the “on watch” category for now.

Equity markets are driven by a variety of factors. While broad economic growth is one important ingredient, it isn’t the only one – equity markets are also where innovation is funded and rewarded.

What we have is a decent traditional economy in the world’s largest market (the U.S.), and in many other places economic growth is hanging in. At the same time, the innovation story (all things AI) isn’t particularly beholden to oil or the consumer (yet). AI is still in the buildout, capital-expenditure stage. In some respects, it is still in the discovery phase, too, as it continues to deliver surprises. For investors, the best surprise is spectacular earnings growth, and the spread of that earnings growth to more companies. The most recent example is increased sales and revenue at an expanded set of semiconductor companies.

It’s all about earnings, always.

Ultimately, equities have enjoyed surprisingly good results because earnings growth has been surprisingly stellar. Some criticize that aggregate earnings of a benchmark index are skewed by the massive amounts of spending happening in the AI rush. Skewed doesn’t mean weakness is masked in all other sectors. Earnings growth is simply good to better at many companies and spectacular in some AI-related area.

Across the globe, estimates are rising for earnings growth. Yes, the biggest bumps are in the AI-related businesses, but it isn’t all AI. Supportive earnings growth is broad based. Consider Canada, where all 11 S&P/TSX sectors saw sales growth; seven sectors posted positive earnings growth, while six logged double-digit growth. For the S&P 500, it was almost a clean sweep: 11 of 11 sectors delivered sales growth and 10 of 11 posted positive earnings. Consider that over half of the S&P 500 companies reported year over-year earnings growth of 10% or more. Half of these, 128 companies, grew earnings by 25% or more.

Earnings are the lifeblood of share-price growth – and the earnings are delivering. AI juiced, yes; the whole story, no. Since the 17th century when the Dutch invented stock markets, their function has been to connect those who have excess savings (investors) to those who need capital (entrepreneurs). Innovations require capital. Occasionally, new broad-based, general-purpose technologies have a wide impact on society and equity markets.

AI is considered a general-purpose technology (or GPT, not to be confused with GPT in ChatGPT which is Generative Pre-trained Transformer). The test of whether AI is a revolutionary GPT is playing out. The daisy chain goes like this: inventions need capital, stock and bond markets (hence the term capital markets) provide that capital. In the meantime, the invention gets built out and winners and losers are identified while companies race to be the first, fastest, best, most-adopted owner of the technology. By definition, if it is a true GPT, the technology is productivity enhancing and many other companies outside of the initial ecosystem will begin to adopt it. This adoption leads to productivity gains across a widening swath of the economy.

Even though there are disruptions, trade-offs and growing pains, productivity has historically and always been a powerful driver of rising standards of living, and a larger economic pie. The first slice of that pie goes to the innovators (i.e., huge single-stock gains and mammoth companies that didn’t previously exist). The second slice goes to the providers of capital more broadly as share prices rise across industries on productivity gains. Lastly, the many remaining slices go to society more broadly. Every technological advance has generated fear of change to the status quo and anxiety about what the new will look like. We know humans by nature are wary of change. Yet, we also know that technology is just a tool. Modern society would be much less enjoyable and prosperous if we still used the sickle and hoe, the buggy whip, or that corded landline phone on the kitchen wall.

|