MWW- Geopolitics Optional, AI Mandatory

DHL Wealth Advisory - May 29, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Well, we’re not sure if this is the end of the conflict with Iran, and we’re definitely not sure that this ends well. But equity markets are in no mood for such trifling details, not with the tidal wave of spending on AI rolling on...

Well, we’re not sure if this is the end of the conflict with Iran, and we’re definitely not sure that this ends well. But equity markets are in no mood for such trifling details, not with the tidal wave of spending on AI rolling on, with corporate earnings still blazing, and with the prospect of a handful of massive IPOs in coming months. Even the global back-up in bond yields only slowed the rapid market ascent for a few days but barely caused it to break stride—the S&P 500 is now sitting on a nine-week winning streak.

In fact, since bottoming in late March, the index has powered up more than 17%, while the Nasdaq has popped 26%. To be clear, that’s in the space of just ~40 trading days; the only two stronger such stretches in the past 20 years were bounces off extreme lows in 2009 and 2020. Even the Dow managed to rebound above 50,000, hitting a new record high for the first time since early February.

Adding some fuel to the fire were unconfirmed reports that the U.S. and Iran were close to an agreement. (We won’t trouble the raging bulls with the small matter that we have heard that before, perhaps seven or eight times, and doubts resurfaced Friday.) That slim thread was still enough to drive oil to its lowest levels of the month.

Even with some slight moderation in oil prices and bond yields, the market is more firmly leaning to the view that the US Federal Reserves next move is likely to be a rate hike, not a cut. The relentless rally in equities, signs of firming job growth, and surprisingly hawkish Minutes from the April FOMC all added to the mix. This presents Fed Chair Kevin Warsh with a rather inconvenient truth—if he is still advocating for rate cuts, as in his Senate testimony last month, he may be a lonesome dove. The case for cuts simply is not there at the moment.

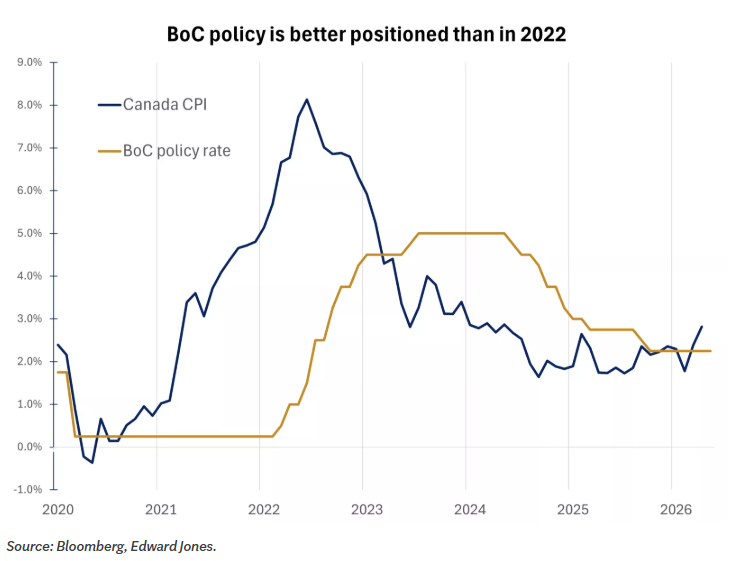

The recent acceleration in the CPI, along with the Fed minutes showing that some officials would consider rate hikes if inflation remains elevated, may bring back uncomfortable memories of 2022. That was the last time the BoC and Fed had to respond to high inflation with aggressive rate hikes, a tightening cycle that ultimately contributed to a bear market in stocks.

However, we think there are several important differences between today’s inflation backdrop and the one investors faced in 2022. Those differences suggest that the central banks' playbook is unlikely to be the same.

- Monetary policy is not easy. In 2022, the BoC and Fed policy rates were near literally at or near zero while headline CPI was moving toward 8%. Today, policy rates are largely matching inflation, giving the central banks less urgency to respond aggressively to every upside surprise.

- The labour markets are no longer overheated. In 2022, job openings were roughly twice the number of unemployed workers and wage growth was accelerating. Today, unemployment remains low, but has been rising, hiring has slowed, and wage growth is not reaccelerating in a way that would meaningfully push services inflation higher.

- Fiscal support is less stimulative. Post-pandemic stimulus boosted demand in 2022 while supply chains were still constrained. Today, fiscal support is much more limited, even as targeted measures are helping households absorb higher energy costs.

For these reasons, we think the BoC and Fed will remain vigilant but are unlikely to overreact to what may prove to be a temporary, energy-driven inflation spike that is largely outside of their control. Before the conflict, global oil supply was far exceeding demand. If conditions normalize around the Strait of Hormuz, oil prices could retrace toward prior levels, helping ease some of the recent pressure on headline inflation.

BMO’s economics team's base case is that both the Fed and BoC stay on hold this year. They no longer expect near-term cuts in the U.S., but still think the bar for rate hikes is very high.

Meanwhile, Canadian real GDP fell at 0.1% annual rate in Q1, well below consensus expectations and the flash estimate of growth of around 1.5%. All the headlines will be focused on the fact that this marks the second consecutive quarter of GDP declines, as Q4 was revised even lower to drop of -1.0% annualized (from -0.6%). To be sure, these are modest declines—the Q1 dip was barely there, and could be easily revised away—and, as StatCan pointed out, GDP actually expanded on a per capita basis in Q1. Still, the economy has contracted in three of the past four quarters, and real GDP was down 0.1% from a year ago last quarter. So, while there will be plenty of debate over whether this constitutes a recession (we would say "no, not really"), there is little debate that the economy has struggled to make any headway over the past year amid the ongoing trade conflict.

Now for some of the details: The Q1 weakness was largely driven by a surprise decline in government spending and investment. Government had previously been consistently strong, with big increases in investment the past few quarters, but fell at a 2.4% this quarter. Consumer spending was okay at +1.5%, while business investment continues to struggle, contracting 3.2%. It's no surprise that housing was weaker as well, down nearly 8%, with the tough winter weighing on an already heavy market. Net trade was also a big drag, subtracting about 3.8 ppts, while inventories neatly offset that by adding 4.3 ppts. That's a reversal from Q4.

Bottom Line: There's no sense sugar-coating this sour result, as the economy has clearly been struggling to grow since the start of the trade war, with headline growth also blunted by the rapid slowdown in population. Government spending had been supporting growth the past few quarters, putting a floor under the economy, but that support wasn't there in Q1. Importantly, consumer spending held up in the quarter and is up a steady 2.0% y/y, but is now dealing with the energy shock. Overall, this should really throw a wet blanket on rate-hike talk, as the economy is in no condition to deal with higher rates. (Even if it's only a "technical recession" or a recession in name only, the market is still priced for rate hikes? Seriously?) A trade deal and/or lower energy prices would help support growth, but we can't necessarily rely on either just yet.

Sources: BMO Economics Talking Points: All’s Well that Ends Well? BMO Economics EconoFACTS: Cdn. Real GDP (Q1, March)

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.