MWW - Follow the Earnings, Not the Noise

DHL Wealth Advisory - May 08, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

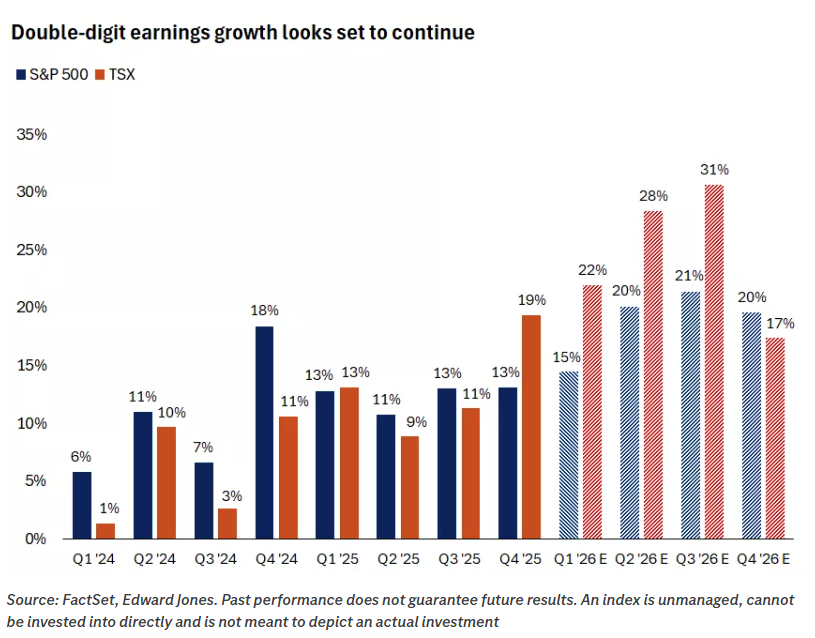

Last week marked a key inflection point in the first-quarter earnings season, with 181 companies in the S&P 500 and 41 in the TSX reporting results.

Last week marked a key inflection point in the first-quarter earnings season, with 181 companies in the S&P 500 and 41 in the TSX reporting results. Notably, five of the Magnificent 7—Alphabet, Amazon, Apple, Meta, and Microsoft—released earnings, placing a significant portion of market leadership under scrutiny at the same time. Overall, results have been encouraging, reinforcing the view that corporate profitability remains strong and continues to offset ongoing geopolitical uncertainty.

Current estimates point to TSX earnings growth exceeding 20% for the first quarter, while S&P 500 earnings are tracking toward roughly 15% growth. If realized, this would mark a sixth consecutive quarter of double-digit earnings expansion. The strength reflects a combination of solid revenue growth and profit margins that remain elevated by historical standards. Although the reporting season is still underway, several key themes have already emerged:

- Broad-based strength: Earnings growth is being driven across most sectors. In the U.S., technology, materials, financials, and industrials are leading, all delivering strong double-digit gains. Health care and energy remain the only sectors posting year-over-year declines, though both are expected to recover in upcoming quarters. Looking ahead, all 11 sectors are projected to contribute to earnings growth in 2026, with U.S. earnings expected to rise more than 18%. In Canada, growth could be even stronger, with TSX earnings forecast to increase by about 25%, supported by energy and materials.

- Limited impact from Middle East tensions: Outside of industries directly exposed to higher fuel costs—such as airlines—most companies are reporting minimal near-term demand disruption tied to geopolitical developments. While management teams continue to highlight potential risks if tensions persist, there is little evidence so far of a meaningful impact on orders or spending.

- Resilient consumer demand: U.S. consumer spending trends remain intact. Credit card providers continue to report healthy activity, with American Express noting stable growth among higher-income customers. Visa has not seen signs of weakness among lower-spending cohorts, and MasterCard pointed to solid overall demand, despite some softening in cross-border spending.

- AI remains the dominant growth driver: Ongoing investment in artificial intelligence continues to underpin earnings momentum, particularly within the technology sector. While market reactions to last week’s mega-cap tech earnings were mixed, all five companies exceeded expectations. As a result, projected technology sector earnings growth for the quarter has risen sharply to roughly 45%, up from about 26% just six months ago. Looking forward, spending on AI infrastructure shows no signs of slowing. Major cloud providers—Amazon, Alphabet, Microsoft, Meta, and Oracle—are now expected to invest approximately $700 billion collectively this year, representing an increase of around 80% year over year. While questions remain about the long-term returns on this capital, it should continue to support earnings for semiconductor firms and companies tied to data center development. Over time, productivity gains from AI are also likely to benefit sectors such as industrials.

Meanwhile, recent economic data reinforce the strength reflected in corporate earnings. In Canada, GDP is estimated to have rebounded to 1.5% in the first quarter, broadly in line with Bank of Canada expectations. The U.S. economy also appears to be on solid footing, with real GDP expanding at a 2% annualized pace. Stripping out more volatile components such as inventories, trade, and government spending, private domestic demand rose 2.5%, indicating healthy underlying activity.

Consumer spending moderated slightly but remains resilient, supported by rising incomes and tax refunds, which helped offset higher energy costs. While elevated oil prices could gradually weigh on spending, there is little evidence at this stage of a broad slowdown. Business investment continues to stand out, with spending on IT equipment and software contributing meaningfully to growth—reflecting sustained demand tied to AI.

Taken together, the data suggest that while higher energy prices may pose a headwind if sustained, there are currently few signs of meaningful stress in either the U.S. or Canadian economies.

Markets have rallied sharply in recent weeks, and the path forward may be less straightforward. Although geopolitical developments remain fluid—including a new peace proposal from Iran—there is no clear resolution to ongoing energy supply risks. At the same time, central banks remain on hold, with a slightly more cautious tone. Against this backdrop, it is not surprising to see divergence across asset classes. Equity markets have been supported by a technology-led rally in the U.S. and commodity strength in Canada, both underpinned by strong earnings. In contrast, bond markets have been more focused on inflation risks, oil prices, and policy uncertainty.

Following such a strong advance, risks now appear more balanced, and a period of consolidation would not be unexpected. That said, the strength in earnings continues to provide an important cushion. As long as corporate profits maintain their upward trajectory, there is little justification for a materially negative outlook, and investors may be better served by looking through short-term headline noise.

For now, corporate earnings remain the dominant force shaping markets. As earnings go, so too does market direction—and at present, profits continue to offer a reliable anchor.

Sources: Weekly Strategy Perspectives – A BMO Private Wealth Publication - Wrangling Risk

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Member-Canadian Investor Protection Fund. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp.