MWW - April's Surprise; Earnings Rise

DHL Wealth Advisory - May 01, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Yes, It Is Still An Inflationary Recovery And A Bull Market... The events in the Middle East are still ongoing, but equity markets have clearly changed their tune in recent weeks.

Yes, It Is Still An Inflationary Recovery And A Bull Market...

The events in the Middle East are still ongoing, but equity markets have clearly changed their tune in recent weeks. It’s almost as if the initial shock or surprise from the crisis has passed and markets are now looking at the backdrop a little more broadly. What they see is a world where economic

indicators are still improving and earnings are still growing. This is really important as strong earnings have historically provided a solid anchor for equities.

Indeed, the outlook for earnings is usually what separates a stock market correction from the early stages of a bear market. Truth be told, it is sometimes hard to distinguish between the two early on. Maybe it is the beginning of Q1 earnings season that refocused investors as, so far at least, aggregate results have beaten expectations and been somewhat encouraging. The stock market can be myopic at times, but for now it is discounting a scenario that sees continuing growth in the economy.

The rebound in equities has been impressive and for Growth stocks especially (top 1% stuff in such a short period of time). Growth is typically the segment that investors turn toward when economic uncertainty is limited and risks of a recession are still low. If a recession was in the cards, Defensives would likely lead relative returns, and this would probably be in the midst of a bear market. In essence, the recovery in stocks tells us that the economic outlook is still “ok” despite the rise in oil prices.

One variable that we believe is getting overlooked is the behavior of pro-cyclical factors. Indeed, we have seen the top quintile of “high-beta” stocks generate alpha in the S&P 500 since the beginning of the crisis. This is huge as it tells us that the economic recovery trade is still very much alive when we look beneath the hood. it is not just about Iran … The overall backdrop also matters (i.e., stimulus). It’s human nature to be drawn to the negative headlines and focus on the risks at hand, especially when there is so much going on in the world. But there’s a whole other story percolating behind the scenes: the economic recovery trade is still in play. The good news for markets is that there is a lot of stimulus in the pipeline, both monetary and fiscal, providing a backstop. The US Fed has cut official rates six times since late 2024, with three of those cuts coming in the last two quarters of 2025. The Bank Canada has done considerably more: five moves in 2024 and two in 2025 for total easing form the peak of 2.25%. Given that it typically takes about 18 months for these cuts to be fully digested and flow through to leading indicators (LEIs), including the equity market, there’s a lot of runway ahead.

What makes this story so powerful is that we also have fiscal dollars positively impacting the economy at the same time as past monetary stimulus. This is not a dynamic that we’ve seen often historically so this is a bit of a rather unique tailwind. It hasn’t been getting much press in recent months, for obvious reasons, but the One Big Beautiful Bill Act (OBBBA) is also putting money in the pockets of consumers.

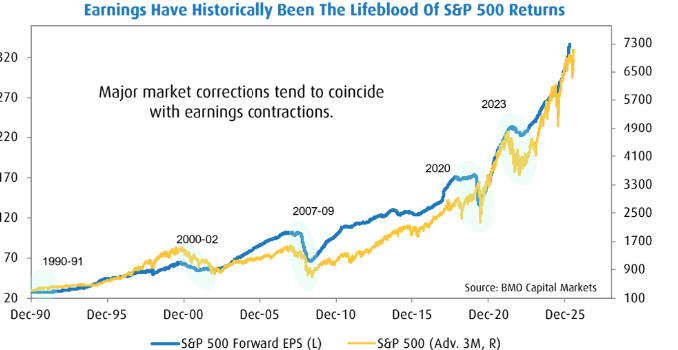

There’s understandably been some surprise at how resilient equities have been in the face of a conflict that’s producing a lot of uncertainty. Stimulus certainly helps, but another key reason is the strength in earnings. According to FactSet, S&P 500 earnings growth is running in the mid-teens and Q1 2026 was the sixth straight quarter of double-digit (year-over-year) growth seen in reported earnings. Margins are also extremely strong. So far, the blended net S&P 500 profit margin for Q1’26 is 13.4% which marks the highest margin reported for the series since FactSet began tracking the metric in 2009. The current record was set in the previous quarter. Typically, when earnings are growing strongly any significant pull back is an opportunity to buy the dip. Major corrections tend to coincide with earnings that are contracting, not barreling ahead.

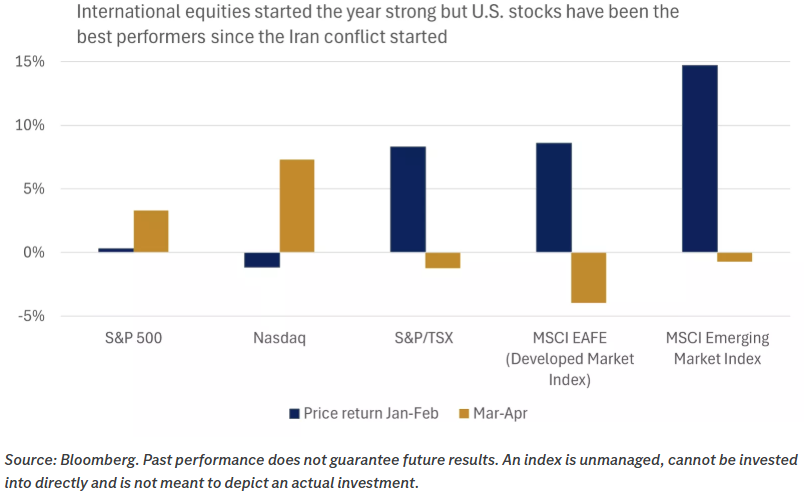

Canadian and international equities outperformed U.S. benchmarks at the start of the year, as improving earnings growth, more attractive valuations, and a weaker U.S. dollar all combined to drive a shift in market leadership. However, in the wake of the Iran shock, and the latest upgrades to U.S. tech-earnings expectations, we have seen U.S. stocks clearly outperform since the end of February.

These shifts in market leadership underline why we always preach that investors should target a diverse basket of stocks in their portfolio. In our view, diversification allows exposure to a range of investment themes, from AI investment, to improving international earnings, to more attractive valuations. Moreover, it can help cushion shocks that might emerge to the macroeconomic and market outlook by spreading and diversifying risk across a wider group of companies and geographies. Never hesitate to reach out to ensure your portfolio remains appropriately diversified for the current environment and aligned with your financial goals.

Sources: BMO Capital Markets Research: Yes, It Is Still An Inflationary Recovery And A Bull Market … For Now?!?

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.