MWW - To the Moon!

DHL Wealth Advisory - Apr 02, 2026

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

North American markets delivered some well deserved gains this week amidst of flurry of headlines that gave investors a glimmer of hope the Iran conflict would soon be over.

North American markets delivered some well deserved gains this week amidst of flurry of headlines that gave investors a glimmer of hope the Iran conflict would soon be over. Capital markets typically pay attention to geopolitical developments—elections, legislative changes, even military action—only when they have a clear and lasting impact on economic fundamentals. In this context, President Donald Trump has proven to be a uniquely transformative force, unleashing sweeping changes across U.S. trade and foreign policy within days of assuming office.

Channeling William McKinley—the tariff‑wielding, empire‑building 25th President—the administration moved quickly to reset America’s global posture. Tariffs were imposed on allies and adversaries alike. Significant cuts targeted soft‑power institutions such as USAID, broad swaths of the federal workforce, and senior diplomatic and military leadership. Multilateral institutions including the IMF, World Bank, and NATO were put on notice to increase financial contributions and refocus on core mandates. Expansionist rhetoric extended toward Canada, Greenland, Venezuela, and Cuba. The speed and scale of these moves left global leaders and corporate executives scrambling to decipher the strategy.

Investors initially responded by pushing stocks and bonds down, fearing that the breadth and depth of policy changes would instigate a recession and/or higher inflation. Markets were able to quickly right themselves thanks to a combination of factors (e.g., delay and reduction in key tariffs, reset earnings expectations that companies in aggregate easily beat). By year’s end, stocks were at/near new highs, bond yields were down and central banks were cutting rates or holding steady after they had already reduced rates to stimulative levels. A new raft of initiatives laid a solid foundation for a continued upward growth trajectory: business/consumer tax benefits from the One Big Beautiful Bill Act; aggressive regulatory and permitting rollbacks; new frameworks for important growth industries (AI, crypto); more tolerance for large Merger & Acquisition activity; and a variety of new methods of industrial investment introduced by the government to encourage domestic infrastructure and resource development.

Lesson learned: stay focused on fundamentals while the implications of pivots sort themselves out.

Fast-forward to 2026. Markets again hit fresh new highs in early February – similar to what they achieved before last year’s Liberation Day – only to be caught a bit off guard when the U.S. and Israel attacked the Iranian regime on February 28. Stock and bond markets ground lower while energy and dollar prices rose in reaction to a number of factors:

- The vociferousness of the Iranian response (especially restricting the flow of goods and 20% of the world’s energy production through the vital Strait of Hormuz)

- The duration so far (weeks, not hours/days)

- Increasing damage to key infrastructure

After a U.S. ultimatum posted on social media last Saturday imposed a 48-hour timeline, futures trading on Sunday evening pointed to a rocky open when cash trading began the next day. But another social media post less than two hours before the open of trading sparked a rapid reversal: negatives of up to 2% declines turned into 2% increases in under a minute. Oil prices fell sharply, while stocks pushed higher. All this despite the fact that Hormuz is still not technically open and Iran is denying talks are underway. Additional positive headlines on Tuesday evening created time and space for negotiation. This further cheered markets (despite the fact that thousands of U.S. troops are on their way to the area and travel through the Strait is still largely halted). Then, Thursday morning we saw markets whipsaw ~2% on the back of an aggressive Trump speech the night before and comments mid-day that Iran and Oman were working on a resolution to open the Straight of Hormuz. Bottom line here is that Capital markets continue to gyrate with every headline and social media post as the week wore on.

Lesson learned: for the moment, investors’ focus is near term (a time horizon measured in minutes/hours not months/ years) and narrow (watching for the next social media post or headline). It’s also clear that participants really want to move past the war and get back to focusing on something (almost anything) else. This mirrors the intent to move on from the tariff issue last year. Markets reverted to fundamental focus even though ultimate tariff rates and structures still remain unresolved. “Escalate to de-escalate” is a core Trump theme, but investors seem to have collective amnesia between bouts.

It will be tricky territory for the global economy over the next few weeks and months. The sooner the Strait of Hormuz can be reliably pried open and energy production restored, the better the odds that central bankers around the world look through sticky inflation and resist rate hikes. The range of potential outcomes (in industry parlance, the “tail risk” meaning the best/worst case scenarios) are wide apart and tough (if not impossible) to predict.

On the plus side, the U.S. earnings season kicks off in earnest in just a few weeks and shortly thereafter in Canada. Similar to last year’s Q1 report season (which delivered many insights into how companies were handling the early days of the tariffs shock), we would expect frank discussion re where companies are seeing increased pricing/growth pressures, where they are finding opportunity and how they are responding.

Given how fast events are unfolding (and the multi-channels information is flowing through), it makes sense to remain careful observers before making any major readjustments. We were moderately overweight a growth orientation coming into the year. We still believe that is the most likely scenario, particularly if a successful Iran off-ramp is navigated in days versus weeks. At the margin, though, careful rebalancing makes sense.

While this might be uncomfortable in the short term, there could be longer-term opportunities emerging for certain investors. The sell-off in bonds over the past month offers fixed-income investors an opportunity to lock in more attractive yields. Similarly, the drop in equity markets seen over the course of this shock has helped push valuations toward more attractive levels. The S&P500 was down 9.7% from its recent peak while the NASDAQ officially hit corrective territory at 11% from its peak last year. Similarly, rallies in some of the best performing parts of the market this year – like emerging market equities, international equities and small-cap stocks – have been partly or fully reversed. We think that investors with longer time horizons, and tolerance for short-term volatility, might find attractive opportunities in the wake of these discounts.

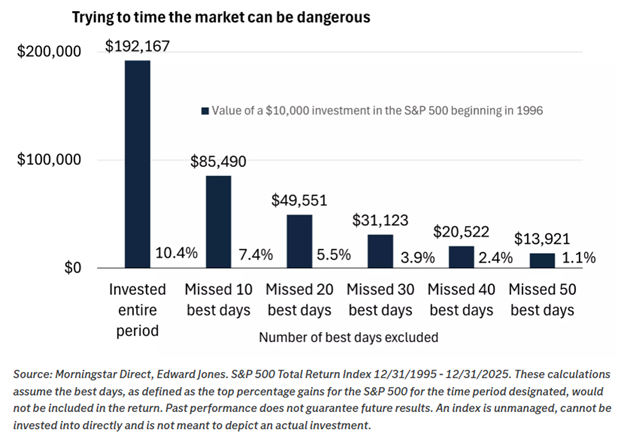

Ending this week with an excellent chart. In times of volatility, or even within strong markets, you’ll often hear us say that it’s generally unwise to try and time the market. The reason? The market’s best and worst days tend to cluster together, often within days or even hours of each other. Multiple long‑term data sets show that: 7 of the S&P 500’s 10 best days occurred within two weeks of its 10 worst days. Look at this Tuesday’s ~3% rally in the S&P500 – its best day since May 2025. Or last years Tarif scare that saw S&P 500 fall around 6% on April 4, then bounced 9.5% on April 9.

Why?

Many of the largest single‑day rallies happen during corrections, not bull markets. This happens more often than not. Wells Fargo Investment Institute mapped out the 30 best days and the 30 worst days for the S&P 500 over the past 30 years. It found that the largest percentage gains and the largest percentage losses often happened in quick succession. So going to the sidelines and waiting for an all-clear horn can be somewhat risky – missing out on these big days is very costly from a long-term growth perspective. Just take a look at the below chart.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.