MWW - And Just as the World Stopped Caring About EV's...

DHL Wealth Advisory - Mar 06, 2026

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

- Testimonial

Global markets were lower on the week on the back of escalating tensions and war in the Middle East. The conflict between the U.S./Israel and Iran represents the biggest challenge for the global oil market since Iraq's invasion of Kuwait in 1990...

Global markets were lower on the week on the back of escalating tensions and war in the Middle East. The conflict between the U.S./Israel and Iran represents the biggest challenge for the global oil market since Iraq's invasion of Kuwait in 1990. Speculation that hostilities could break out have supported oil prices by US$5-8/bbl over the last several months. Actual hostilities mean higher oil prices; a spike through US$100/bbl is probable if important oil facilities are bombed. A prolonged closure of the Strait of Hormuz is unlikely but in the near-term tanker owners will be reluctant to transit the Strait. Global natural gas markets could also be thrown into turmoil as ~20% of global LNG supplies also transit the Strait. The near-term outlook is unknowable as it depends on Iran's actions and capabilities; however, the risk for commodity markets is strongly biased to the upside, in our opinion.

Here is what we know so far…

- The US and Israel have launched attacks against Iran with one of the implied objectives being a regime change. So far, the attacks have been aerial, with no boots on the ground just yet.

- Among the casualties so far, Iran’s supreme leader Ayatollah Khamanei as well as other leaders from the Revolutionary Guard. Iran has responded to the strikes by targeting other US allies in the region. Meanwhile, Trump has indicated that he is willing to talk to the new Iranian leadership.

- Activity through the Strait of Hormuz is basically nil at this point. Shipping insurers have cancelled current policies have raised coverage prices by over 50% in response to developments over the weekend.

- Oil majors and trading houses have also suspended ship operations in the region. Several Middle East ports have closed due to damage.

We’re going to keep our comments focused on what the conflict will mean for the economy and markets. That’s not to say that we should look past the human costs, but as market strategists, those are beyond the scope of what we can speak on here.

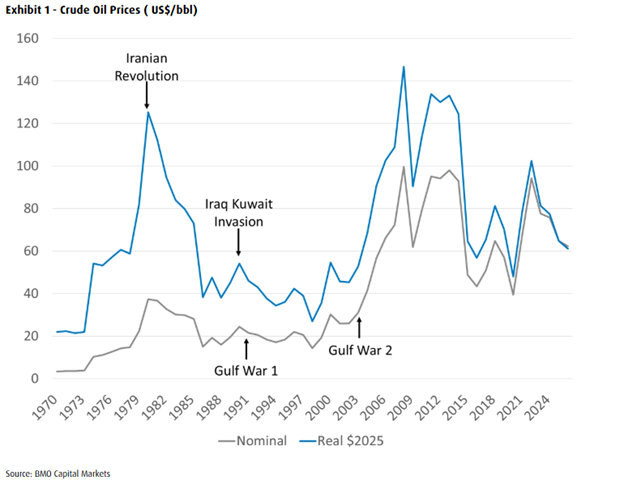

Of course this isn’t the first time we’ve navigated turmoil in that part of the world. Using History as a guide, hostilities in the Middle East have often had a significant impact on oil prices given how much crude oil is produced in the region. The Iranian revolution in 1979 led to a doubling in crude oil prices that persisted for several years. Iraq's invasion of Kuwait in 1990 led to a 50% increase in crude oil prices that lasted roughly six months. The two wars between the U.S. and Iraq (1991 and 2003) had virtually no impact on oil prices. Similarly, the brief 'wars' between Israel and Iran in 2024 and 2025 had limited impact on oil prices.

So which is this? It depends on how the conflict evolves. Iran exports ~1.5 million b/d that could be replaced by other countries such as Saudi Arabia; however, more oil from Persian Gulf countries means more oil flowing through the Strait of Hormuz. Roughly 19% of global oil supply flows through the Strait. Iran has threatened but never successfully closed the Strait. That said, if Iran successfully bombs key oil infrastructure in the Persian Gulf that could represent a significant disruption in global supplies.

This week saw crude oil prices to surge by ~US$20/bbl due to increased risk, rising tanker premiums and reduced oil shipments. If Saudi and/or UAE oil facilities are damaged, crude oil prices could easily hit US$120/bbl as there is not enough space capacity or inventories to offset such as a loss.

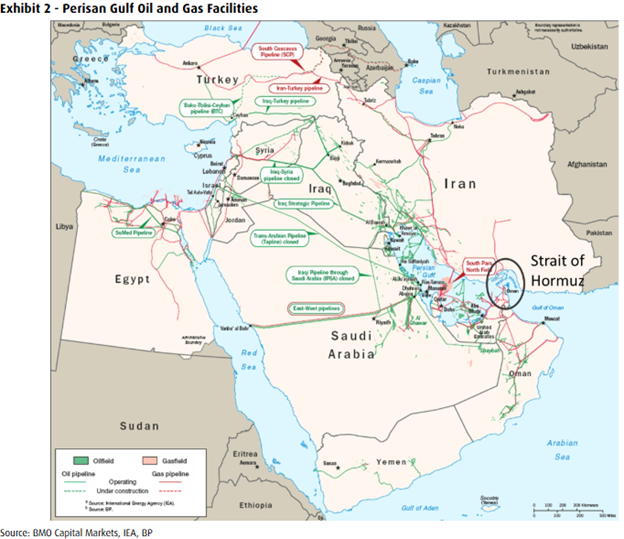

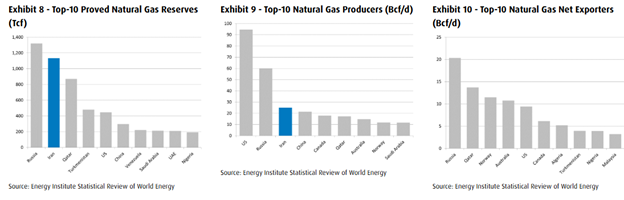

The Persian Gulf countries (Saudi Arabia, Kuwait, UAE, Qatar, Irag and Iran) produce roughly 26 million b/d or 25% of global crude and liquids supply. All the crude oil and natural gas producing, processing, liquefaction and refining facilities in this region are within striking distance of Iranian missiles.

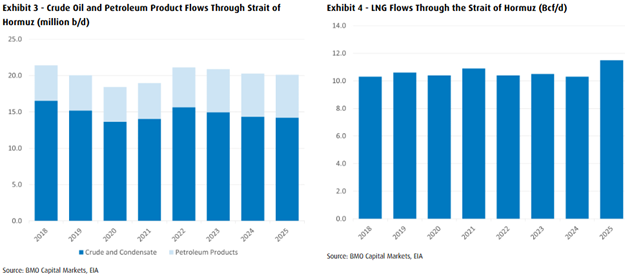

The Strait of Hormuz is one of the world's main transit points for shipments of crude oil, petroleum products and liquefied natural gas (LNG). At its narrowest point, the Strait is only 21 miles wide, making it more susceptible to block aids or attacks. Roughly 20 million b/d or 19% of global crude oil and petroleum products, and 11 Bcf/d or 20% of global LNG shipments transit the Strait. According to the U.S. Energy Information Administration (EIA), Saudi Arabia's East-West pipeline and UAE's Abu Dhabi pipelines have spare capacity of 2.5 million b/d, which clearly is not enough to offset the majority of crude oil that is hipped through the Strait.

Iran a Major Oil and Gas Player

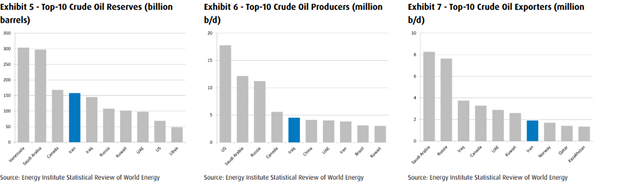

Iran holds the fourth-largest oil reserves and is the fifth-largest crude oil producer in the world; however, they are only the seventh-largest export due to high levels of internal consumption.

Iran also holds the second-largest natural gas reserves in the world and is the third largest producer. Iran does export some natural gas to Europe via pipeline but has not built up a significant export capability, likely due to ongoing sanctions.

Given the significant resource potential in Iran, a change to an investment friendly government could translate to a significant surge in investment and production, albeit over an extended time period.

Some Oil Price Scenarios

The near-term outlook for crude oil prices is unknowable as it depends on Iran's actions and capabilities, however, there are four plausible scenarios.

Capitulation: Iran could agree to fully dismantle its nuclear program. However, this could be complicated by the U.S.'s stated objective for regime change. It seems to us that 47 years of religious rule will not quickly change to secular rule. That said, de-escalation is possible. If this occurs we expect that crude oil prices could retreat to recent ranges of US$60-70/bbl.

All-Out War: Another possibility is that Iran reacts aggressively and attempts to infliction maximum damage on oil infrastructure in the Persian Gulf in order to spike oil prices and hurt the U.S. economy. Oil prices could surge well through US$100/bbl.

Civil War: The U.S. and Israel could sufficiently weaken the Iranian regime but not fully engage. Rival factions could emerge that seek control and plunge the country into civil war. This could lead to a disruption in Iranian exports but ultimately have little impact on global oil markets. If this occurs we expect that crude oil prices could retreat to recent ranges of US$60-70/bbl.

Paper Tiger: It is possible that Iran's capabilities have been overstated or severally degraded. The U.S. and Israel could quickly end the war after eliminating key leaders and accepting the surrender of the country. The U.S. would be seeking a friendly, secular regime that is open to foreign investment. While this outcome could see near-term oil prices remain elevated, it could translate to lower prices longer-term.

The bottom line is that there are a lot of unknowns right now and the situation is changing by the hour. For us, the key unknown is whether this conflict will extend beyond a month and what that means for the shipping through the Strait of Hormuz. All of the above estimates are predicated on a conflict that lasts beyond a month with shipping through the Strait remaining contained.

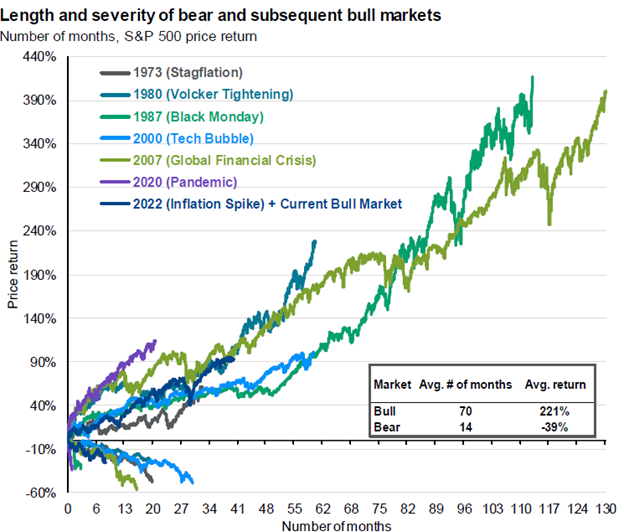

The economy was on solid footing just last week (i.e., before the war started). Hell, equity markets are still within a few percent of all-time highs, although significant internal rotation had been occurring during the handoff of current tech-focused/narrow leadership to a broader cast of participants. This week’s action has been orderly, though it feels more acute coming on the heels of the steadier, less-volatile climb experienced through much of last year.

Global economies are teed up for solid growth in the year ahead. Pro-fiscal stimulus politicians have been voted into power in key countries, and infrastructure and defense spending plans are increasing accordingly. Markets have done well at absorbing the many challenges thrown at them in the past 18 months; we expect similar behavior in the current situation. Exposure across a variety of global equity markets and sectors (while bonds play an important cushioning role) continues to demonstrate that diversification works. We’re expecting some near-term defensiveness in risk assets as the initial shock is priced in. But we’re still of the mind that investors should remain invested – especially in commodity-sensitive areas. We are not changing our macro regime call for now but do acknowledge that this weekend’s events could truncate the time we’re in it.

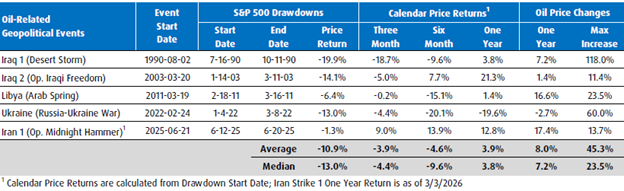

We will end it on the below table that runs through the data on the last five geopolitical events that were centered around an energy crisis. The takeaway should be that despite immediate S&P 500 drawdowns, the S&P500 was higher in all but once instance, and that one instance was related to the Covid-19 induced inflation scare, not the war in Ukraine.

Source: BMO Capital Markets Research

he opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.