So Much For the Dog Dayz.

DHL Wealth Advisory - Aug 22, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

It was setting up to be a week of divergence for North American benchmarks with Canada’s TSX hitting new all-time-highs throughout the week while our counterparts to South put together a 5-day losing streak that saw major indices retrace...

It was setting up to be a week of divergence for North American benchmarks with Canada’s TSX hitting new all-time-highs throughout the week while our counterparts to South put together a 5-day losing streak that saw major indices retrace a few percent. That was until Friday. Investors had been waiting with bated breath all week leading up to US Fed Chair Jerome Powell’s speech at the annual Economic Symposium in Jackson Hole.

And apparently it was worth the wait. Heading into the event, investors had turned somewhat cautious after last week’s concerning round of U.S. inflation results for July and some earlier guarded remarks by Fed officials. Meantime, a new front opened up on the assault on Fed board members, with Governor Cook cordially invited to resign by the Administration. Amid all these moving parts, the market is back to looking at a strong chance of a rate cut at the September 17 FOMC meeting, albeit still not a lock—there is, after all, almost a full month of data to go. In what was a meaty speech in Wyoming, arguably the key message was found in these two sentences:

“Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

Market interpretation: Interest rates are going lower, soon. The market's near-unabated rise since April promptly resumed post-Jackson, taking the index to a new record high. Meantime, the U.S. dollar pulled back in the wake of Powell’s remarks, although it has been quietly firming after a six-month bludgeoning in the first half of the year. It had risen to a three-month high against the Canadian dollar above $1.39 (or below 72 cents(US)) just prior to the speech.

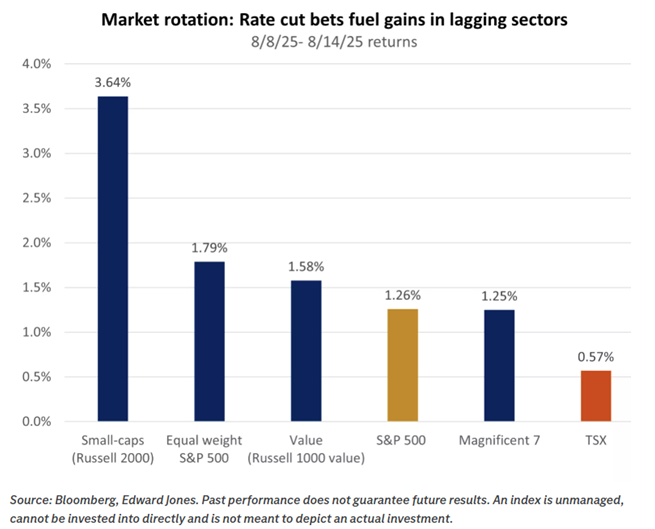

The market implications should be noticeable as easing may help broaden gains. Last week’s market action offered an early glimpse of how investors may position for a potential Fed pivot in September. U.S. small-cap stocks, which are more sensitive to interest rates due to their reliance on debt financing, rose over 3% for the week. Meanwhile, value-style investments and the equal-weighted S&P 500, which gives each company the same influence regardless of size, outperformed the traditional cap-weighted index, signaling a welcome broadening of market leadership.

While history doesn’t repeat, it often rhymes. In past cycles, the market’s response to Fed easing depends on whether rate cuts are pre-emptive ("insurance cuts") or reactive. Insurance cuts, like those in 1995, 1998, and 2019, aim to support the economy before clear signs of trouble and tend to be bullish for equities.

Recession-driven cuts (reactive), such as in 2001 and 2007–2008, often coincide with poor risk sentiment and weaker market returns. Today’s backdrop suggests the former: while labour demand appears to be cooling, jobless claims and unemployment remain historically low, and corporate profits and GDP continue to grow at a healthy pace.

We suspect that measured rate cuts this year and next could help further boost investor sentiment. Potential beneficiaries include rate-sensitive and cyclical industries, such as homebuilders, real estate, and banks. We favour the consumer discretionary and financials sectors, which could get a lift from the upcoming Fed pivot.

To sum up, the path to rate cuts may be uneven, as we have seen over the last two years, where markets have been eager for rate cuts and sometimes disappointed that the Fed has not delivered them. But we believe the direction of travel for rates is likely to remain lower. With inflation treading water and labour-market strains becoming more pronounced, the balance of risks may soon tip toward action. Chair Powell’s remarks at Jackson Hole validate the now-high expectations that, after a seven-month pause, rate cuts are likely to resume in September. In this environment, we believe diversified portfolios, which include both growth-style investments benefiting from long-term AI tailwinds and value-oriented exposures poised for a cyclical boost from easing policy, may be well-positioned for the evolving Fed narrative.

The mildly dovish words from Wyoming weren’t the only breaking news on Friday morning, as it was reported that Canada would be removing a long list of retaliatory tariffs on U.S. goods. Basically, the only items still facing Canadian tariffs will be metals and some autos (largely mirroring U.S. measures). This followed a day after the first conversation between PM Carney and President Trump in weeks and is an important step. The direct implications for the Canadian economy are that it will: a) take some pressure off specific CPI items (e.g., groceries, sporting equipment), which could help shave core inflation back below 3%, and b) further cut into expected tariff revenues. Recall that the Liberal election platform had been based on annual tariff revenues of $20 billion; we are now looking at a fraction of that amount, introducing yet more pressure on the fiscal outlook.

It is becoming growingly clear that the inflation threat from the trade war was a tad overblown, for Canada and for the U.S., albeit for different reasons. For the States, its unrivalled market power means that the Administration is not fully offside for asserting that companies will ultimately eat some of the tariffs. For Canada, the two big drivers of potential trade war inflation have vapourized—the retaliatory tariffs, which weren’t that fierce to begin with, have been further declawed; and, the Canadian dollar is 3%-to-4% stronger than when the trade war first erupted, not weaker, even with its recent sag.

The back-down on Canadian retaliation should thus fully quiet the talk of trade-war led inflation, alongside this week’s tempered CPI reading for July. The latter revealed that the three-month core inflation trend eased to 2.4%, its first trip below 3% since last fall. This opens the door to further rate cuts by the Bank of Canada. While a move in September remains a bit of a long shot—markets peg the odds at about 1 in 3—a move in October is seen as likely, and there could be more to come. BMO’s economics team continues to lean to the low side, calling for a total of three cuts by next spring, which would take rates just a touch below the low end of neutral. But given the more benign trade-related inflation risks and a softening job market, they believe that below neutral would ultimately be entirely appropriate.

Source: BMO Economics Talking Points: The Swan Song Remains the Same

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.