On the Edge of Easing

DHL Wealth Advisory - Aug 08, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Summer may be drawing closer to its end, but economic data and corporate earnings kept investors fully engaged this week. The buy-the-dip narrative was in full effect as markets bounced following last week’s weaker than expected data...

Summer may be drawing closer to its end, but economic data and corporate earnings kept investors fully engaged this week. The buy-the-dip narrative was in full effect as markets bounced following last week’s weaker than expected data. Dovish fedspeak, increased probability of a September rate cut, and robust corporate earnings have drove investor sentiment as major indices closed this week in the green.

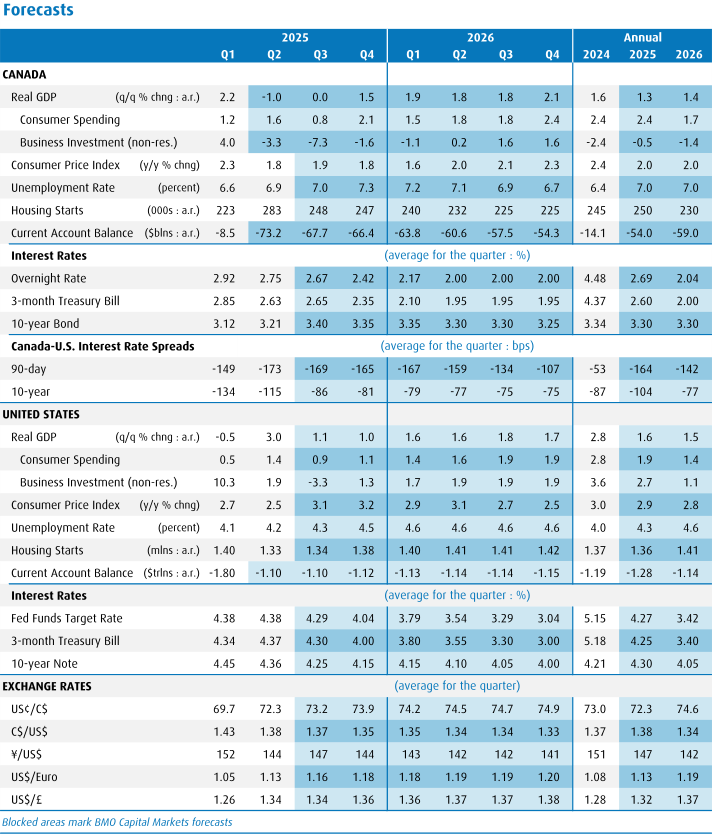

On the economic front, the U.S. labour market remains a critical barometer for rate expectations, and this week’s data showed subdued unit labour costs in the second quarter amid stable wage growth and firmer productivity, which should help insulate inflation from tariff pressures. Among non-farm businesses, labour productivity rose 2.4% annualized, fully retracing the prior quarter's decline, with both figures distorted by large swings in imports and GDP. The increase was a bit better than the market expected and lifted the yearly rate slightly to 1.3%. While this marks a slowdown from the two-year average 2.4% y/y pace, it's unclear how much is related to trade policy uncertainty and the need for some businesses to source alternative suppliers. This report largely supports the Fed's view that labour markets are not a source of inflation pressure, implying that tariffs will likely provide just a one-time lift to inflation. Assuming a soft August jobs report and no big upside surprises in the next two monthly inflation reports, the Fed will likely resume easing in September. In fact, the odds of a Fed easing in September have soared to above 90%, and there are full expectations of at least one more move in 2025. This dramatic increase was also spurred by the sudden replacement of a relatively hawkish Fed governor with a presumably dovish substitute.

The massive shift in Fed rate expectations has spilled over into the Bank of Canada outlook, despite the plain fact that the BoC has very much carved its own path in the past year. That minor detail aside, the prospect of fast and/or furious Fed cuts has revived talk of BoC trims. Those odds got a shot in the arm from a weak Canadian employment report for July (-40,800), which acted as a heavy counterweight to the shockingly strong result the prior month (+83,100). Combined, the two months made some sense, albeit the net average job gain of just over 21,000 is resilient, especially since manufacturing jobs managed to rise in both months. But, bigger picture, the trade uncertainty lingers, and this follows a nasty 31% a.r. plunge in real exports in Q2, yielding the largest quarterly trade deficit on record.

Even if the Canadian economy stumbles, the BoC will need convincing that core inflation is ebbing. Wages were neutral in the jobs data, ticking up to 3.3% y/y, but in an acceptable range and well below the 5%+ pace in mid-2024. The softness in energy prices will help, both on headline inflation, as well as the more subtle effect on food costs and even some core areas. OPEC’s decision to keep ramping production is offsetting concerns about a tightening of sanctions on Russian oil, and quietly strengthening the case for rate cuts by both the Fed and the BoC. Finally, note that as much as the BoC wants to be independent from the Fed, we now know that the next six decision dates are on the same day as the FOMC.

On the tariff front, Six trading partners, including biggies the European Union, Japan, South Korea, and the U.K. managed to reach deal frameworks with the White House before its self-imposed August 1 deadline. Apart from the UK's 10% duty, the other regions were hit with levies ranging between 15% and 20%. They also pledged hundreds of billions of dollars in direct U.S. investments and purchases of American-made goods (how their governments will compel private businesses to fulfill these pledges isn't clear). Over 60 other countries were slapped with modified reciprocal duties ranging between 15% and 41%, while other trading partners (including those that run trade deficits with the U.S.) face a minimum 10% base duty.

Of course, none of the tariffs are written in stone and all could change on a whim. Moreover, the U.S. Court of Appeals may rule the tariffs illegal, though the Administration could try to secure a favorable ruling in the Supreme Court or impose duties under a number of other trade acts. Importantly, the U.S. still needs to make deals with three major trading partners: Canada (which remains in limbo), Mexico (which was granted a 90-day extension), and China (with an August 12 deadline looming). Meanwhile, the White House has just imposed 50% duties on select copper products, with investigations underway for eight other industries, including lumber, microchips, and medicines. The big picture is that we are likely only in the middle stages of this battle, with more surprises to come. Businesses hoping for clarity before committing to hiring and investment decisions will need to wait longer.

Despite weeks of high-level trade talks, Canada was slapped with a 35% “fentanyl” duty (up from 25%), while receiving no break on sectoral tariffs. Still, the average effective tariff rate on goods exports to the U.S. rose just slightly to around 7%, as only a small share (likely less than 10%) is not compliant with the USMCA. Apart from steel and aluminum (50% duties) and motor vehicles (25%, though roughly halved by the U.S. content carve-out), over 90% of goods exports are shipped duty-free. That's why the pressure is on Canada to renegotiate the free-trade agreement when the formal review comes up in July 2026, though talks are expected to begin sooner.

Even under a manageable tariff regime, the economy likely contracted modestly in Q2 due to plunging exports of steel, aluminum, and automobiles to the U.S. and deferred business investments. Still, we now think the economy may avoid a 'technical' recession by holding flat in Q3 and growing 1.5% annualized in Q4. Consumers are showing some resiliency, with advance retail sales rebounding smartly in June and auto sales revving higher in July. Providing support are record equity values, positive income growth, and lower borrowing costs. The latter has pulled debt service costs down from record highs, while easing the pain of mortgage resets. Although joblessness is on the rise, this largely reflects earlier rapid population growth, which has since cooled. Most workers are still drawing a paycheque, even as job growth has slowed to an average of 15,000 per month this year, about half last year's rate. Further support stems from the “Buy Canada” movement and a recent upturn in international tourism amid stricter U.S. border controls.

Source:BMO Economics North American Outlook: The Trade War and the Damage Done

Sources: BMO Economics Talking Points: Life Moves Pretty Fast, BMO Economics North American Outlook: The Trade War and the Damage Done, BMO Economics EconoFACTS: U.S. Productivity (2025 Q2 Preliminary)

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.