Rates to Fall. In Fall?

DHL Wealth Advisory - Aug 01, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Summer temperatures are heating up, and so was the stock market until Friday’s US jobs report and new tariff announcements hit the pause button on a 4-month stock market rally...

Summer temperatures are heating up, and so was the stock market until Friday’s US jobs report and new tariff announcements hit the pause button on a 4-month stock market rally. Despite Friday’s set-back, investors had enjoyed an impressive run so far this season, with the TSX climbing steadily and not registering a single move greater than 1% in either direction for three months. Likewise, the S&P500 had not witnessed a single 1% daily move for all of July.

It was a critical week featuring big-tech earnings, a key trade deadline, Federal Reserve and Bank of Canada meetings, and the U.S. monthly jobs report, all testing the summer's calm. With respect to earnings, it did not disappoint. Mega-cap tech has once again put itself at the forefront with a string of beats and record highs out of most of the “Mag 7”.

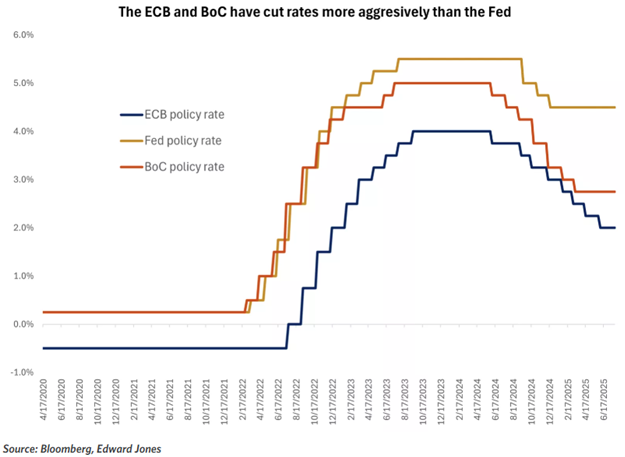

Meanwhile, as widely expected, the US Fed kept policy rates unchanged for the fifth consecutive meeting over the past seven months, with the target range for the Fed Funds rate at 4.25%-to-4.50%. What was interesting from the meeting is that we saw two dissenters for the first time since 1993. Two Governors were not on board with holding rates steady, but rather voted to drop rates 25bps. Setting the stage for potential cuts starting in the fall.

There were a few key tweaks to the statement. First, the text noted that “economic activity moderated in the first half of the year”. That’s a downshift from the June’s statement that described the economy growing at a “solid pace”. Second, the statement reiterated that uncertainty “remains elevated”, but removed language that said uncertainty had “diminished”. We’re expecting the Fed to cut a couple times this year, likely in September and December. But, as always, the moves will be guided by the data.

The Bank of Canada was also on deck Wednesday and elected to also hold rates steady for a third consecutive meeting with the overnight rate at 2.75%. However, the Bank left a crack open for further cuts, intoning that “there may be a need for a reduction in the policy rate”. But, there is a high bar for said rate relief; it would require a weaker economy to put “further downward pressure on inflation and the upward price pressures from trade disruptions are contained”. While the Bank also said it would be nimble and could respond quickly to events, that seems like a lot of dominoes need to fall before they would cut again.

On growth, the BoC notes that the economy has shown "some resilience", though trade uncertainty is weighing on activity. Labour market weakness was noted in trade-related sectors, amid a gradually rising jobless rate and slowing wage growth. A key point: "A number of economic indicators suggest excess supply in the economy has increased since January." A wider output gap means more disinflationary pressure, which normally would mean rate cuts. These certainly aren't normal times, staying the Bank's hand for now, but their worldview would suggest this ultimately leans to lower rates.

While growth slowed notably in the first half of the year, recent economic data has pushed back against the stagflation narrative in both the U.S. and Canada. U.S. initial jobless claims declined, pointing to stable labour-market conditions, and last month's jobs employment report in Canada showed the largest jobs gain in six months. Retail sales rose more than expected in June in the U.S., while in Canada May's decline is expected to be followed by a solid rebound in June. Inflation, while still a concern, is contained for now, as the expected rise in consumer and producer goods prices has been restrained by a decline in services (goods carry a 25% weight in the inflation basket vs. 75% for services).

While the seemingly never-ending trade drama will weigh more heavily into the economic data in coming months, at least we all have a bit more clarity on that file after the flurry of announcements this week. The European Union kicked off the festivities with a 15% handshake deal with the U.S. Administration, setting the tone for others—and Korea soon followed. Heavyweights China and Mexico were set to the side, with the former still negotiating to its August 12 deadline and the latter kept at its 25% rate for three months on non-USMCA goods.

Canada was not spared with a three-month reprieve; instead, it was stuck with a 35% levy on non-compliant goods (which may well represent less than 10% of all exports to the U.S.). Many others were just unceremoniously given a number, including a staggering 39% on Switzerland, 25% on India and 50% on some products from Brazil. Overall, BMO’s Economics team estimates that the combined net U.S. tariff on imported goods will land near 19%, up from little more than 2% at the start of the year.

While the inability of Canada to reach a deal with the U.S. and avert the back-up in its “fentanyl” rate to 35% is a disappointment, the Canadian dollar took it in stride. First, the probability of no deal by August 1 had been well-telegraphed, and accounted for some of the loonie’s net loss this week. Second, the reality is that the 35% rate affects only a small share of Canada’s exports, and bumps up the effective average tariff rate by less than a percentage point (to perhaps 7%).

We suspect this series of market-friendly data may be disrupted in the months ahead as higher tariffs likely impact growth. However, the recent passage of a new U.S. tax bill has brought some clarity to fiscal policy. We expect modest fiscal stimulus next year, with tax cuts, increased business investment, and deregulation supporting a pickup in activity. The upshot, in our view, is that while stagflation concerns may rise as the summer ends, the economy appears well-positioned to weather volatility as headwinds likely ease in 2026.

Record highs typically confirm strength, in our view, not signal imminent reversals. And market internals help support this notion. Equities are outperforming bonds, cyclical stocks are outperforming defensives, high-yield spreads are tight, and market-based inflation expectations appear to point to stable inflation over the longer term.

Still, any deviation from the expected path, whether in trade talks, earnings or Fed decisions, could stir volatility. Seasonality also cautions against overconfidence, as late summer and early fall tend to bring more market turbulence (just look at today). A run-of-the-mill pullback or period of consolidation is inevitable, though difficult to time. We think investors will be best served by avoiding the temptation to chase speculative investments and by doubling down on appropriate diversification across asset classes, styles and sectors.

As it often happens when risks begin to fade, complacency starts to emerge. Meme-stock mania appears to be making a comeback with some retail traders reigniting interest in heavily shorted stocks, driving big price swings that are often disconnected from fundamentals and can reverse violently. This behavior could be a sign of froth. As such we have opted to raise cash in our discretionary mandates. We still remain invested, but will park ~7-9% into cash and await tactical entry points. It’s worth reiterating, there are always some market unknowns, but greater clarity appears to be emerging with respect to trade deals and interest rates. The prevailing trend is upward, but we want to have cash ready for buying opportunities.

Sources: BMO Economics Talking Points: 35 Is the New 25, BMO Economics AM Charts: July 31, 2025

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.