All Quiet On The Crazy Train

DHL Wealth Advisory - Jul 25, 2025

It was yet another week of gains for North American markets, which have basically been higher every single week since the early April lows...

It was yet another week of gains for North American markets, which have basically been higher every single week since the early April lows. That said, gains and volatility have moderated in recent weeks as markets just inch higher in record territory. All the while tariffs and trade continue to remain a cloud over investors and the markets. The U.S. administration has pushed back its trade deadline to August 1 on most of its global trading partners, creating another source of uncertainty for investors. The U.S. also indicated a new, higher 35% tariff on Canada, effective August 1, although USCMA-compliant goods may be exempt from this rate.

However, this week we saw a preliminary trade deal between the U.S. and Japan, marking the first with a top 5 trading partner (okay, #5). It’s potentially important in many respects, including apparently setting a new template for the EU to follow. And, notably, the U.S. Administration was even willing to give a little bit on auto imports (trimming the tariff rate to “just” 15%).

The Japanese equity market response was curious (i.e., big rally, especially for auto stocks). One can only surmise that markets were braced for much worse. (Imagine how robust equity markets would be if tariffs were rolled back even further…just sayin’). We would also note that corporate Japan can more readily deal with a high-ish baseline tariff than others, courtesy of the big weakening in the yen in the past five years. Even with the small pullback this year, the U.S. dollar is still about 33% stronger against the yen (at 147/US$) than the average level of the past 20 years (110). That leaves a lot of potential margin for Japanese exporters, even with a hefty tariff—which also suggests that the U.S. consumer may escape the bulk of the damage, at least on imports from Japan.

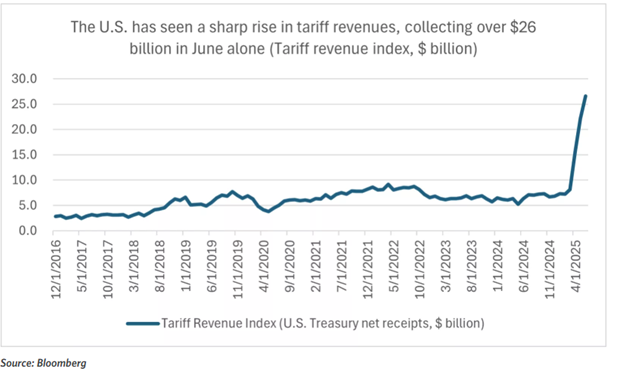

Nonetheless, average tariff rates have already moved meaningfully higher on U.S. imports, as the administration has implemented blanket 10% tariffs, with higher tariffs on China and certain sectors like steel and aluminum and autos. This has increased the average tariff in the U.S. from about 2.4% to about 20.6%, the highest since 1910, according to the Yale Budget Lab. This has also resulted in higher tariff revenues collected by the U.S. Treasury, including almost $27 billion in June.

Circling back to the home front, Canada’s PM Carney more or less echoed the sentiment by cautioning that any deal with the U.S. may well include some semi-permanent tariffs. At the same time, he warned that the August 1 deadline may not hold, and that Canada would not be rushed into a bad deal. Intergovernmental Affairs Minister LeBlanc said “a lot of work” still needs to be done. President Trump showed just how much “work” by suggesting on Friday that, for Canada, it may just be a tariff—not a negotiation. Ok then. While Canada faces the prospect of a 10 ppt hike in its tariff to 35%, that’s only on the narrow slice of non-USMCA compliant goods, so the bigger issue is the sectoral hits on autos and metals. We would note the quirk with Japan’s deal, that a vehicle produced in Yokohama with zero American content could face a lower tariff than a vehicle produced by a U.S. company a river away from the U.S. in Windsor Ontario. Not surprisingly, American auto companies are not amused by this irony, and some warned of the direct cost of tariffs in their Q2 earnings calls.

While trade will rumble away in the coming week, market attention will turn to the FOMC (and BoC) meeting on Wednesday. While there is almost no debate on what rates will do in the US -nothing - the focus on the Fed will be whether there are any dissents, and Chair Powell’s latest take on the economic/trade landscape. The market is leaning heavily to a renewal of rate trims in September (and we concur), and a solid possibility of another move later in 2025. Powell is unlikely to shake that narrative, although it’s also doubtful that he will cement that view.

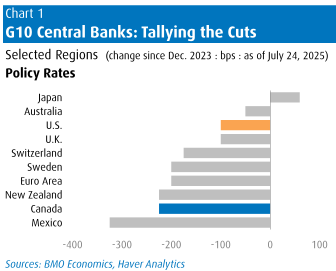

For the Bank of Canada, the odds of a rate cut next week are not zero, especially given looming permanent U.S. tariffs, but the recent core inflation CPI performance is a very high hurdle. And, in contrast to Fed pricing, the market is far from certain that any further rate trims are coming. At this point, there is a bit less than a 50% chance of even one cut priced in for the rest of 2025. Of course, some of that gap with the Fed is due to the fact that the BoC has already delivered 225 bps of cuts versus just 100 bps from the Fed (Chart 1). Still, BMO’s economics team leans to the dovish side of the market, with a somewhat pessimistic view on the prospect for U.S. tariffs, and a relatively optimistic view on underlying inflation.

Overall, U.S. and Canadian stock markets appear to have overcome the peak fear and uncertainty that emerged in early April around the threat of sharply rising tariffs. Since then, we have seen tariff increases get delayed and inflation and economic data remain resilient.

As we look ahead, we would not expect markets to continue to move in a straight line higher. Markets will also have to digest additional tariff headlines as the August 1 deadline approaches. This may mean new and even higher tariff rates, and we may see corporations and export partners less willing to absorb these higher costs. Thus, prices may rise, and consumption could cool in both the U.S. and Canada in the second half of the year.

However, in our view, investors can still feel comfortable that the worst-case scenario – high tariff rates, no positive outcomes from trade negotiations, and runaway inflation – is not likely to play out. In addition, as we look toward the end of the year and into 2026, we would expect prices and inflation to stabilize again and the US Federal Reserve and Bank of Canada to lower interest rates.

We thus believe investors can use pullbacks and volatility to position for a more stable backdrop and re-acceleration of growth in the year ahead. We favour sectors across growth and value, including consumer discretionary, financials, and health care.

Source: BMO Economics Talking Points: All Quiet on the Crazy Train

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.